Key Takeaways:

- The “Power” Play: CEO Toby Rice is positioning EQT as the “fuel tank” for the AI revolution, highlighting that natural gas is the only viable solution for the massive, reliable baseload power needs of data centers.

- Vertical Integration: The reintegration of Equitrans Midstream allows EQT to control its own destiny, lowering its breakeven cost structure and protecting margins during price volatility.

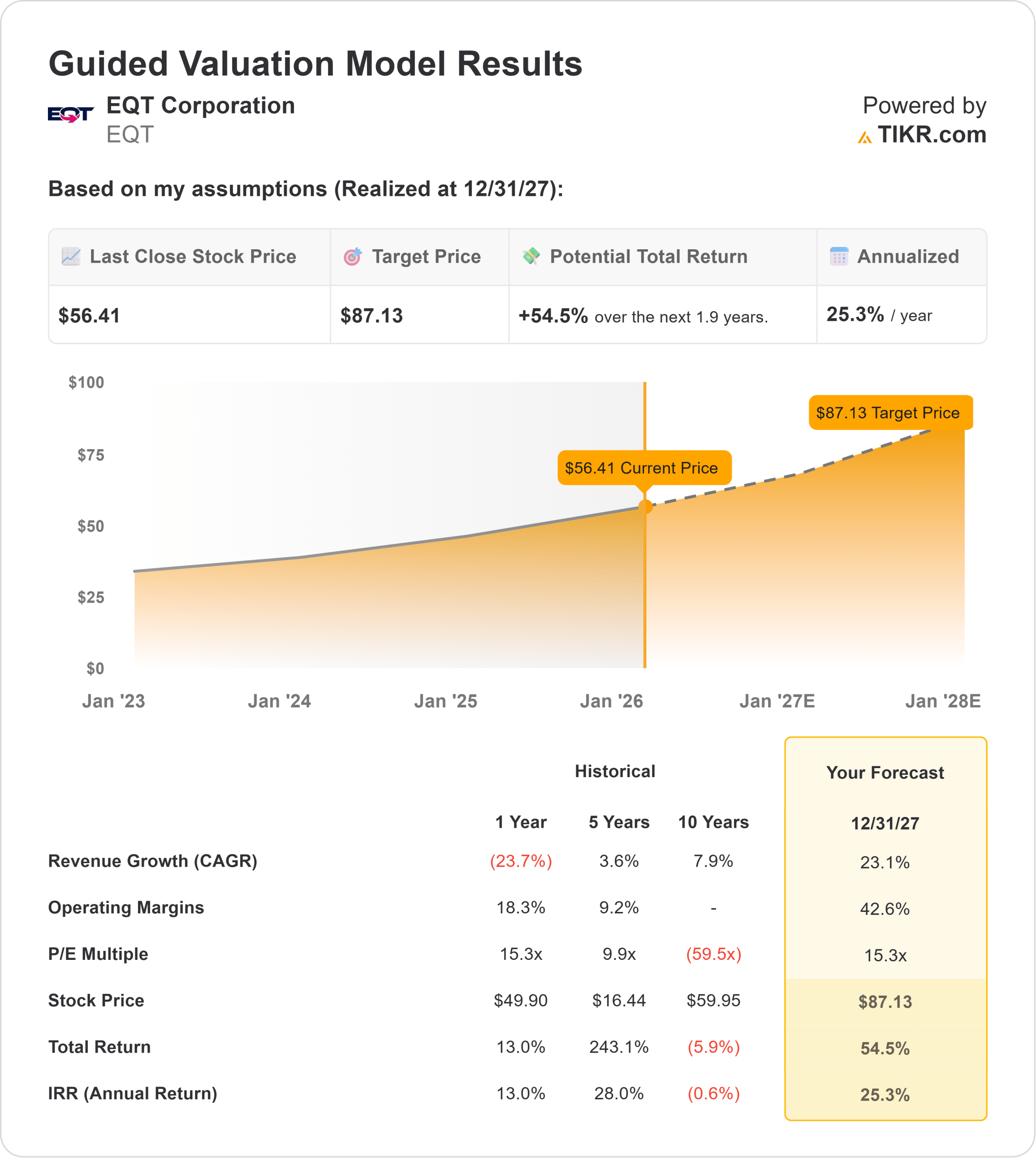

- Price Projection: The valuation model points to a target of $87 by 2027, suggesting significant upside from current levels.

- Compelling Returns: With an implied 25.3% annualized return, the model signals a “Strong Buy,” driven by a structural re-rating of natural gas as critical infrastructure.

EQT Corporation (EQT) is the largest natural gas producer in the U.S., and it is pivoting to serve a new, insatiable customer: Big Tech.

Management has been vocal about the “power demand” story, noting that the grid cannot support the coming wave of AI data centers without natural gas.

In the latest quarter, the company emphasized that inquiries for power supply are at unprecedented levels.

To prepare, EQT has transformed its business model.

By acquiring Equitrans Midstream, EQT has integrated the pipelines with the wells, creating a fortress balance sheet that can withstand cyclical lows.

In Q3, the company demonstrated this discipline by strategically curtailing production to avoid selling into a glut, a move CEO Toby Rice called a “total team effort”.

Financially, the setup is coiled.

While current revenue growth is negative due to cyclical gas prices, the company maintains robust profitability potential.

The valuation model assumes margins can expand significantly as the company executes its integration strategy.

With the stock trading at $56, investors are paying a cyclical low price for a company that could soon be valued as a critical utility for the AI sector.

What the Model Says for EQT Stock

This analysis evaluates EQT’s potential through 2027, factoring in a return to historical growth rates and a valuation re-rating.

The model signals a “Strong Buy.”

Using mid-case assumptions that price in a recovery in gas markets, the model points to a target price of $87.13 (rounded to $87) by December 2027.

This implies a massive 25.3% annualized return from today’s levels.

The model suggests that the market is currently pricing EQT strictly on today’s depressed gas strip.

If the “AI Power” thesis materializes, the combination of margin expansion and volume growth creates a “multi-bagger” scenario.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for EQT stock:

1. Revenue Growth: 23.1%

The model assumes a sharp rebound.

The forecast uses a 23.1% CAGR through 2027, reflecting a recovery from the current cyclical lows (LTM growth of -23.7%) and the onset of new demand drivers.

As data centers come online and LNG export capacity expands, EQT is positioned to capture this volume growth.

2. Operating Margins: 42.6%

Efficiency is the primary driver of value.

The model assumes Operating Margins will expand to 42.6% by 2027.

This expansion is supported by the vertical integration with Equitrans, which permanently lowers the cost structure, allowing EQT to capture more margin per molecule of gas sold.

3. Exit P/E Multiple: 15.3x

The valuation assumes the market will eventually pay a premium for reliability.

The model assumes an exit multiple of 15.3x, which aligns with the company’s historical trading range during upcycles and reflects its status as a premier integrated operator.

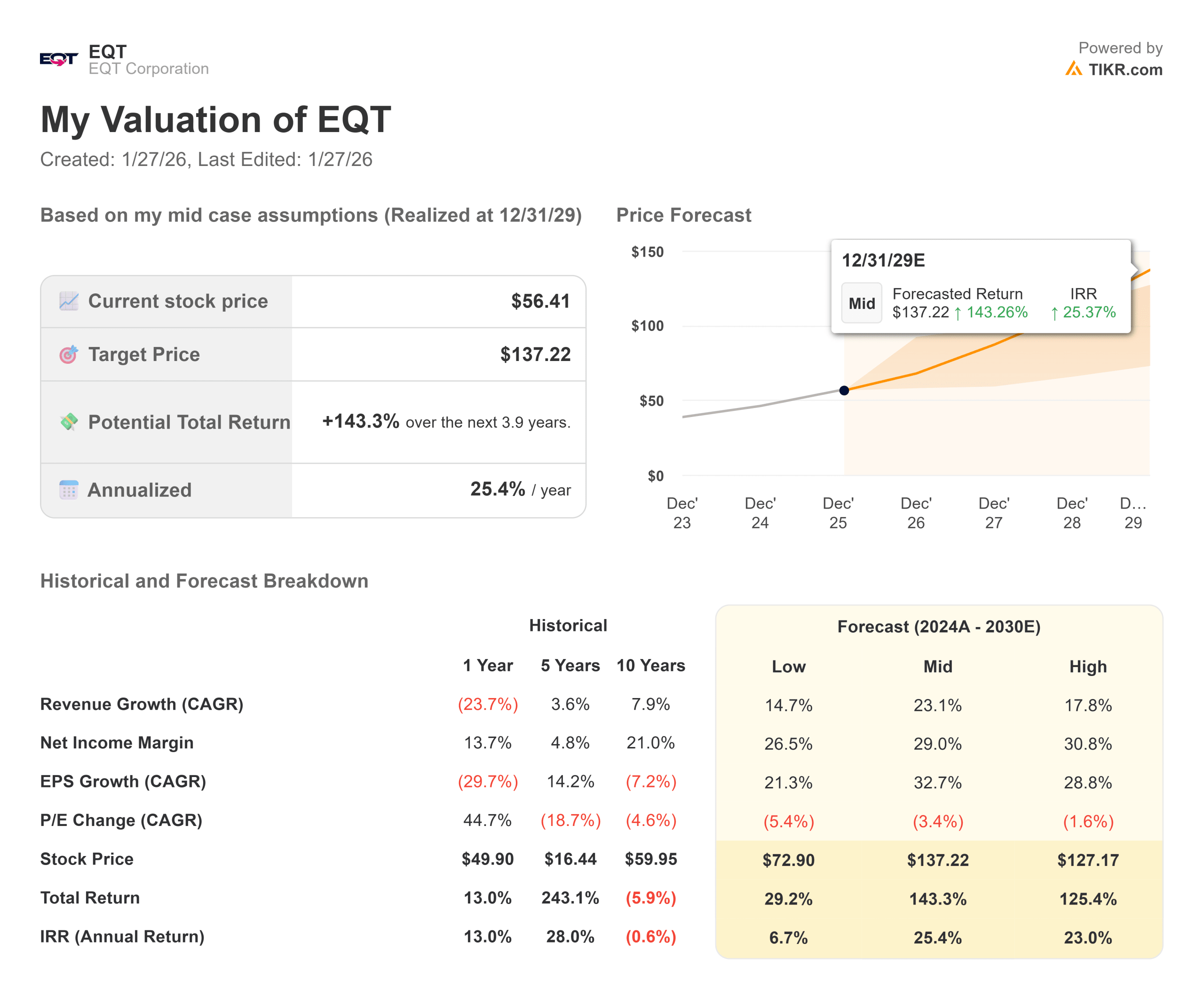

What Happens If Things Go Better or Worse?

The skew is heavily to the upside, provided the “Power” thesis holds (these are estimates, not guaranteed returns):

- Bear Case: If gas prices stay lower for longer and data center demand is met by renewables, the stock could stagnate.

- Mid Case: With a recovery to historical norms, the target is $87, delivering a 25.3% annual return.

- Bull Case: If a natural gas shortage emerges, pricing power could drive margins and multiples even higher, pushing returns well beyond 30%.

See what analysts forecast for the next 5 years for EQT stock (Free with TIKR) >>>

How Much Upside Does EQT Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!