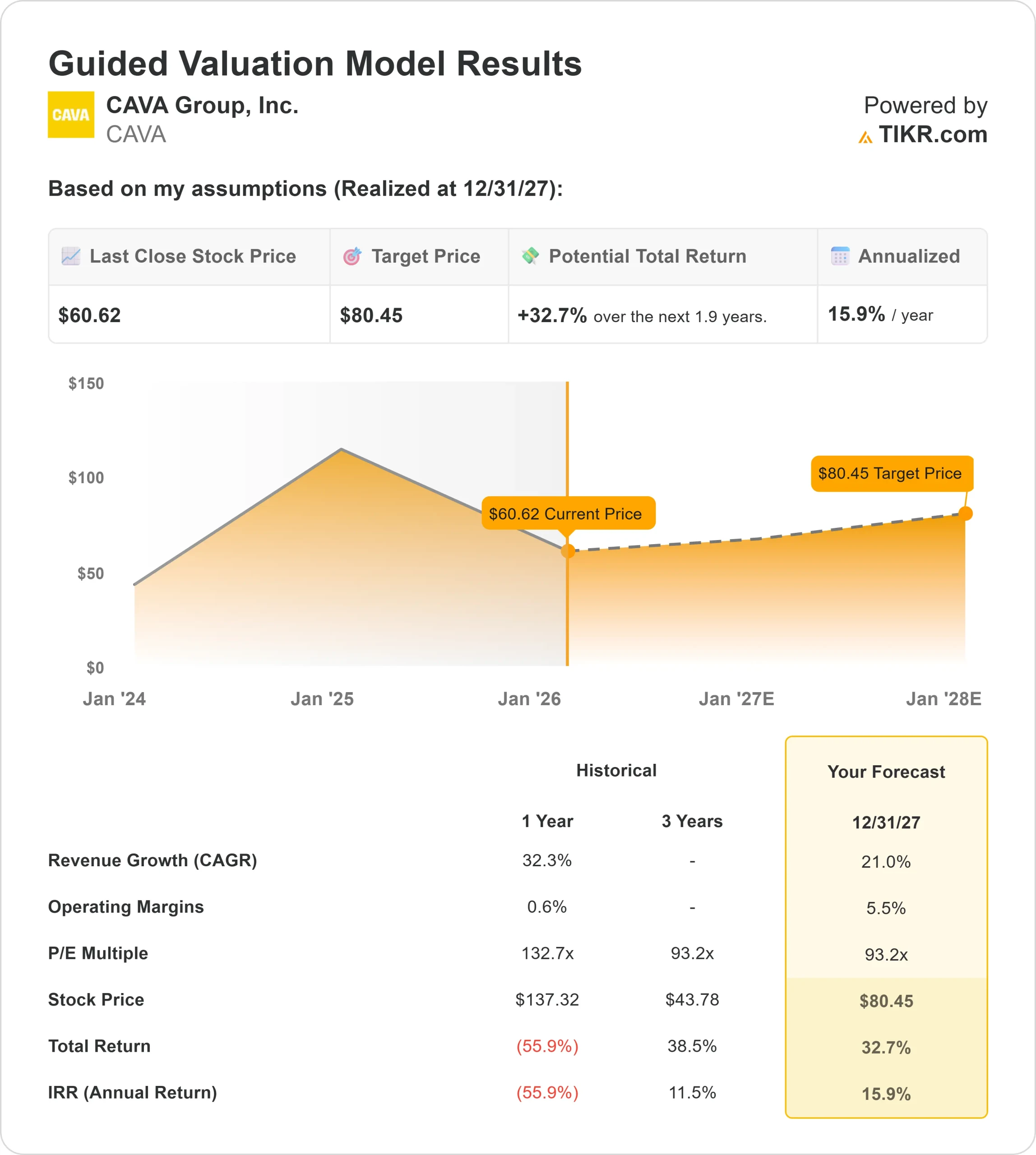

Key Stats for CAVA Group Stock

- Past-Week Performance: -4%

- 52-Week Range: $43 to $144

- Valuation Model Target Price: $80

- Implied Upside: 32.7% over 1.9 years

Value your favorite stocks like CAVA Group with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

CAVA Group, Inc. stock fell about 4% over the past week, finishing near the lower end of its recent trading range. The decline unfolded steadily through the week, pointing to sustained selling pressure rather than a single negative headline.

The drop was driven by sizable institutional selling, which increased share supply at current price levels.

Wealth Enhancement Advisory Services LLC cut its stake by 47.7%, selling 28,378 shares, while Federated Hermes reduced its position by 40.7%, selling 294,880 shares and trimming ownership to about 0.37% of the company.

Insider selling added to the pressure. On January 27, multiple executives and insiders sold shares near $62, including CFO Tricia Tolivar and CEO Brett Schulman, who also sold 21,650 shares earlier in the month. While each sale represented a small percentage of ownership, the cluster of transactions at similar price levels reinforced near-term valuation sensitivity.

On the business side, CAVA continues expanding its footprint, operating 300+ restaurants nationwide while opening dozens of new locations each year.

Management remains focused on improving unit-level efficiency, with digital ordering representing a meaningful portion of sales and loyalty engagement supporting repeat traffic. These initiatives keep margins and scalability in focus as the company heads into upcoming earnings updates.

See analysts’ growth forecasts and price targets for CAVA Group (It’s free) >>>

Is CAVA Group Undervalued?

Under valuation model assumptions, the stock is modeled using:

- Revenue Growth (CAGR): 21.0%

- Operating Margins: 5.5%

- Exit P/E Multiple: 93.2x

Based on these inputs, the model estimates a target price of $80, implying 32.7% total upside from recent levels over the next 1.9 years.

Over the next year, results are likely shaped by how quickly new restaurant openings mature into profitable units as the company continues expanding its footprint.

Same-store sales momentum carries added importance, since incremental traffic can flow meaningfully into earnings once fixed labor and occupancy costs are absorbed.

Food and labor cost discipline remain central, as even modest improvements can lift operating margins from still-early levels.

Digital ordering mix and throughput efficiency also support higher revenue density without requiring proportional increases in staffing or real estate.

At current levels, CAVA appears undervalued, with near-term performance driven by execution on unit economics and margin scalability rather than headline revenue growth alone.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Value Any Stock in Under 60 Seconds (It’s Free)

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>