Key Takeaways:

- Margin Expansion Focus: New CSX leadership targets 200-300 basis points of operating margin improvement in 2026

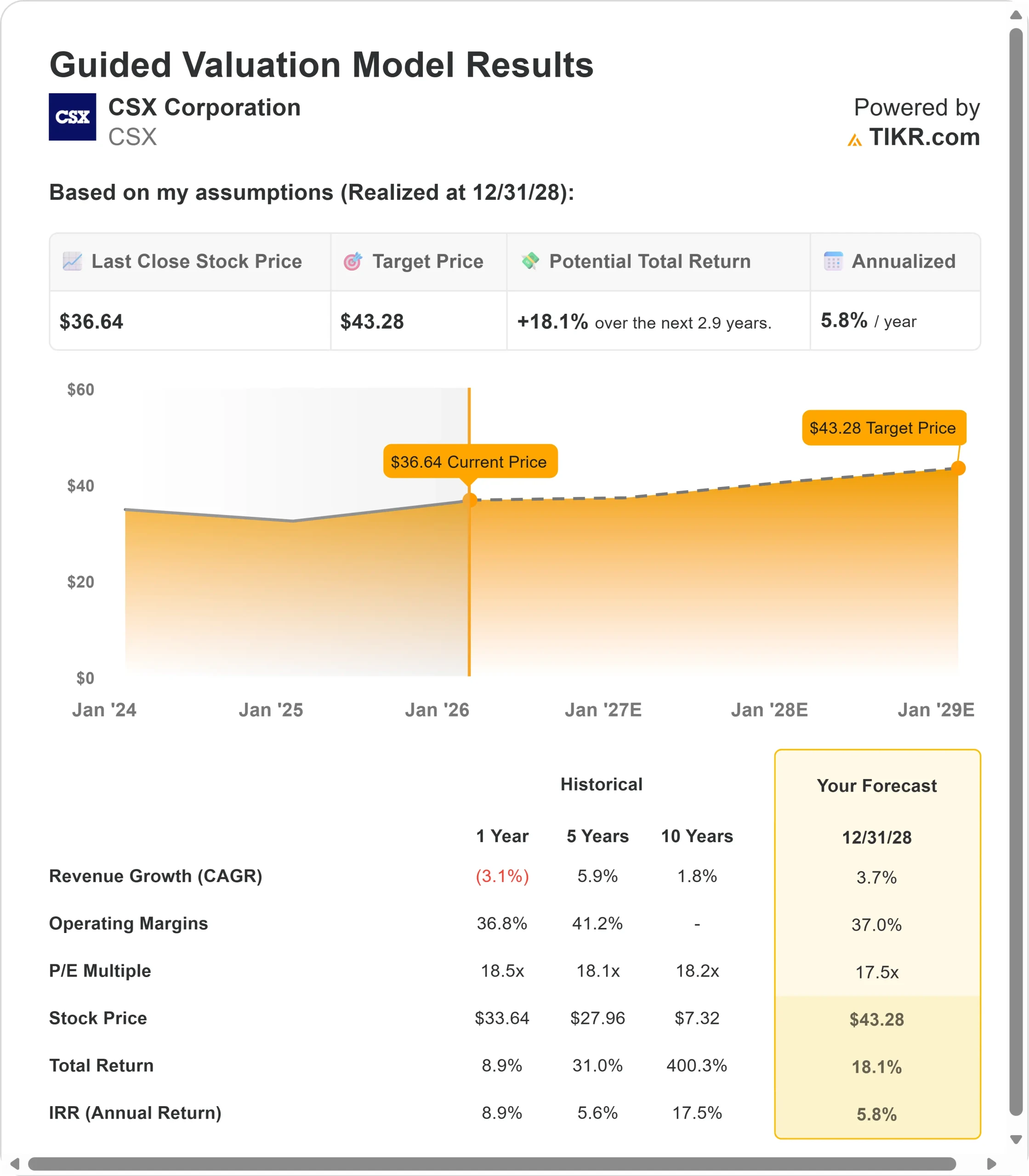

- Price Projection: Based on current execution, CSX stock could reach $43 by December 2028

- Potential Gains: This target implies a total return of 18% from the current price of $37

- Annual Return: Investors could see roughly 6% annual growth over the next 2.9 years

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

CSX Corporation (CSX) just wrapped up a challenging 2025, but new CEO Steve Angel is implementing a disciplined turnaround strategy. The railroad faced subdued demand across key markets, with reported operating income and margins declining year over year in Q4.

Despite these headwinds, CSX delivered modest volume growth and maintained strong service levels. Angel has renewed the leadership team and implemented cost structure adjustments, positioning the company to deliver stronger performance in 2026.

The results are showing early promise.

- Service metrics improved substantially from Q1 to Q4, with velocity, cars online, dwell, and trip plan compliance all trending positively.

- With over 100 cost reduction initiatives identified and a new pricing discipline in place, CSX is building momentum.

See analysts’ full growth forecasts and estimates for CSX stock (It’s free) >>>

What the Model Says for CSX Stock

We analyzed CSX through the lens of its operational turnaround under new leadership focused on margin expansion and cost discipline.

The company is methodically optimizing its workforce and technology portfolio while maintaining the service quality that customers value. Management expects to cycle out $150 million in one-time 2025 charges, including separation costs and technology impairments.

The Howard Street Tunnel project will enable double-stack service from the Southeast to the Northeast starting in Q2 2026. This creates new growth opportunities in both domestic and international intermodal markets, with customers already bidding on business for the enhanced route.

Using a forecast of 3.7% annual revenue growth and 37% operating margins, our model projects the stock will rise to $43 within 2.9 years. This assumes a 17.5x price-to-earnings multiple. That represents a compression from CSX’s current P/E of 19.9x.

As the company invests in operational improvements and navigates soft industrial markets, the multiple faces near-term pressure. However, margin expansion from productivity gains and the completion of major infrastructure projects should support a gradual recovery.

The real value lies in executing Angel’s operational playbook and delivering consistent margin improvement while maintaining service excellence.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CSX stock:

1. Revenue Growth: 3.7%

CSX’s growth story centers on winning share through superior service and capitalizing on infrastructure investments.

Intermodal Momentum: The team won new business in 2025 by delivering faster transit times and expanded connectivity. The completion of the Howard Street Tunnel opens double-stack capability between the Southeast and Northeast, creating meaningful growth opportunities starting in Q2 2026.

Service Quality Driving Wins: Strong operational metrics and consistent reliability allow CSX to compete effectively for new business. Management emphasizes making the most of every profitable opportunity rather than relying on macro improvements.

Market Mix: Growth will be strongest in lower-revenue-per-unit segments such as minerals, fertilizers, and intermodal, driven by infrastructure projects. Higher-margin areas such as chemicals and forest products face ongoing softness due to weak industrial markets.

Coal Stabilization: Two important met coal mines reopened after extended outages. Domestic utility demand continues to grow amid higher natural gas prices and power generation needs, though some plant closures are scheduled for 2026.

2. Operating margins: 37%

CSX is delivering margin expansion through disciplined cost management and operational efficiency.

Current Performance: Management expects to cycle out $150 million in one-time charges, including separation costs and technology impairments that won’t recur in 2026.

Productivity Initiatives: Management identified over 100 diverse savings opportunities across the organization. Rail headcount finished Q4 down over 3%, with further workforce optimization planned. Focus areas include overtime management, outside services spend, asset utilization, and discretionary expense controls.

Inflation Management: Labor inflation of 3-4% from union contracts and healthcare costs will be more than offset by productivity gains. Non-labor inflation should run slightly lower as procurement teams negotiate better rates.

3. Exit P/E Multiple: 17.5x

The market currently values CSX at 20x earnings. We assume the multiple compresses to 17.5x through our forecast period.

Reflects Transition Phase: CSX’s P/E has averaged 18.4x over the past year and 18.2x over 10 years. The lower multiple reflects near-term headwinds from soft industrial markets and execution risk in the turnaround.

Undervalues Long-Term Potential: As margin expansion materializes and revenue growth accelerates from intermodal investments, CSX should command a stronger multiple. The company expects 2026 free cash flow to grow at least 50% year over year, driven by higher earnings and capital discipline.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

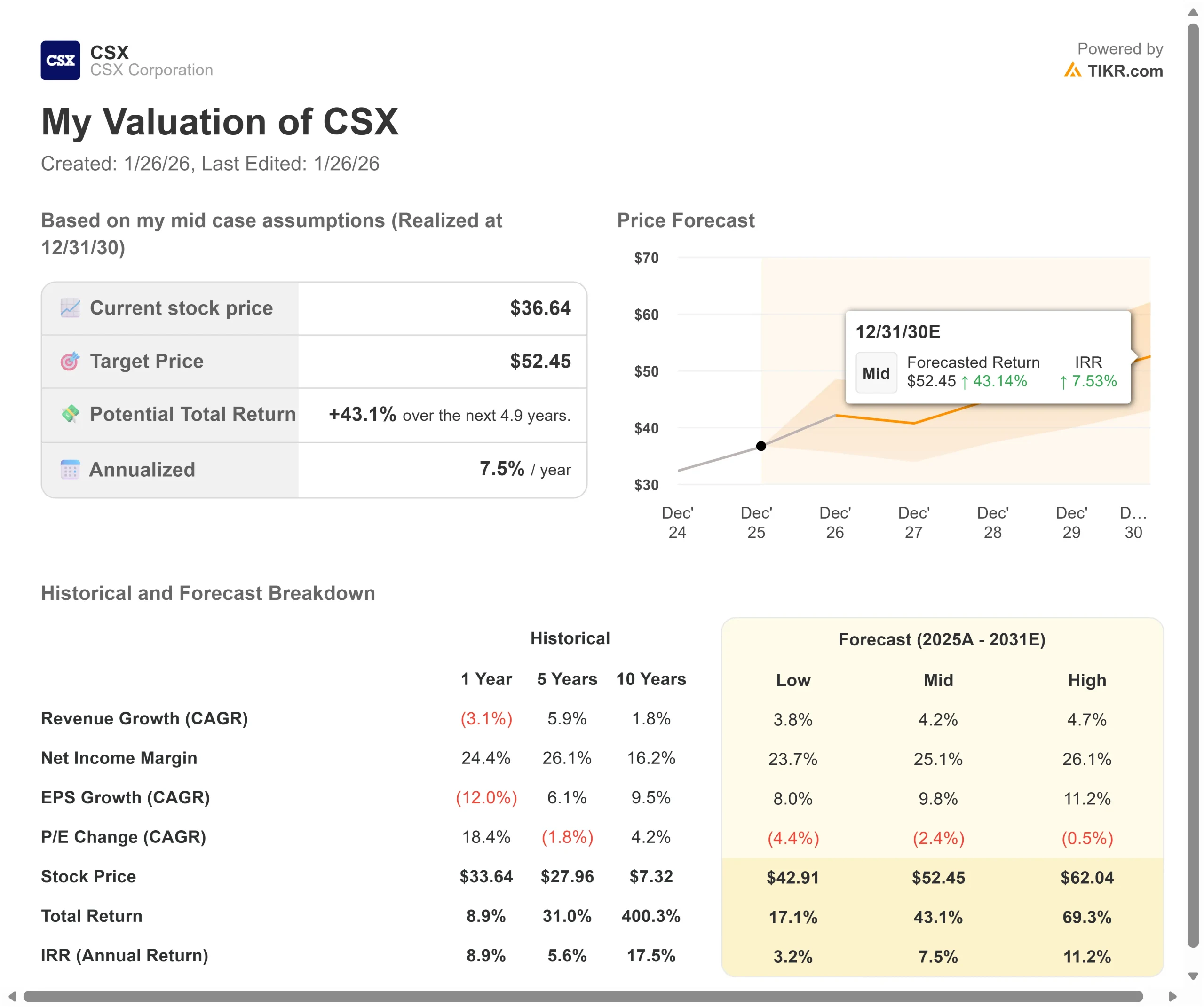

Railroad operators face cyclical demand and competitive pressure. Here’s how CSX stock might perform under different scenarios through December 2028:

- Low Case: If revenue growth slows to 3.8% and margins compress to 23.7%, the stock still offers a 3.2% annual return.

- Mid Case: With 4.2% growth and 25% margins, we expect an annual return of 7.5%.

- High Case: If intermodal ramps faster and productivity initiatives exceed targets at 26% margins while growing at 4.7%, returns could hit 11.2% annually.

See what analysts think about CSX stock right now (Free with TIKR) >>>

The range reflects execution on cost initiatives, success in capturing Howard Street Tunnel growth, and macro conditions in key end markets.

In the low case, industrial markets remain weak longer than expected, or competitive pricing pressure intensifies in intermodal.

In the high case, infrastructure investments drive faster volume growth, productivity initiatives exceed targets, and industrial markets begin to recover in 2027-2028.

How Much Upside Does CSX Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!