Key Takeaways:

- VMware Migration Opportunity: Nutanix is capturing significant market share from Broadcom’s VMware as enterprises seek alternatives.

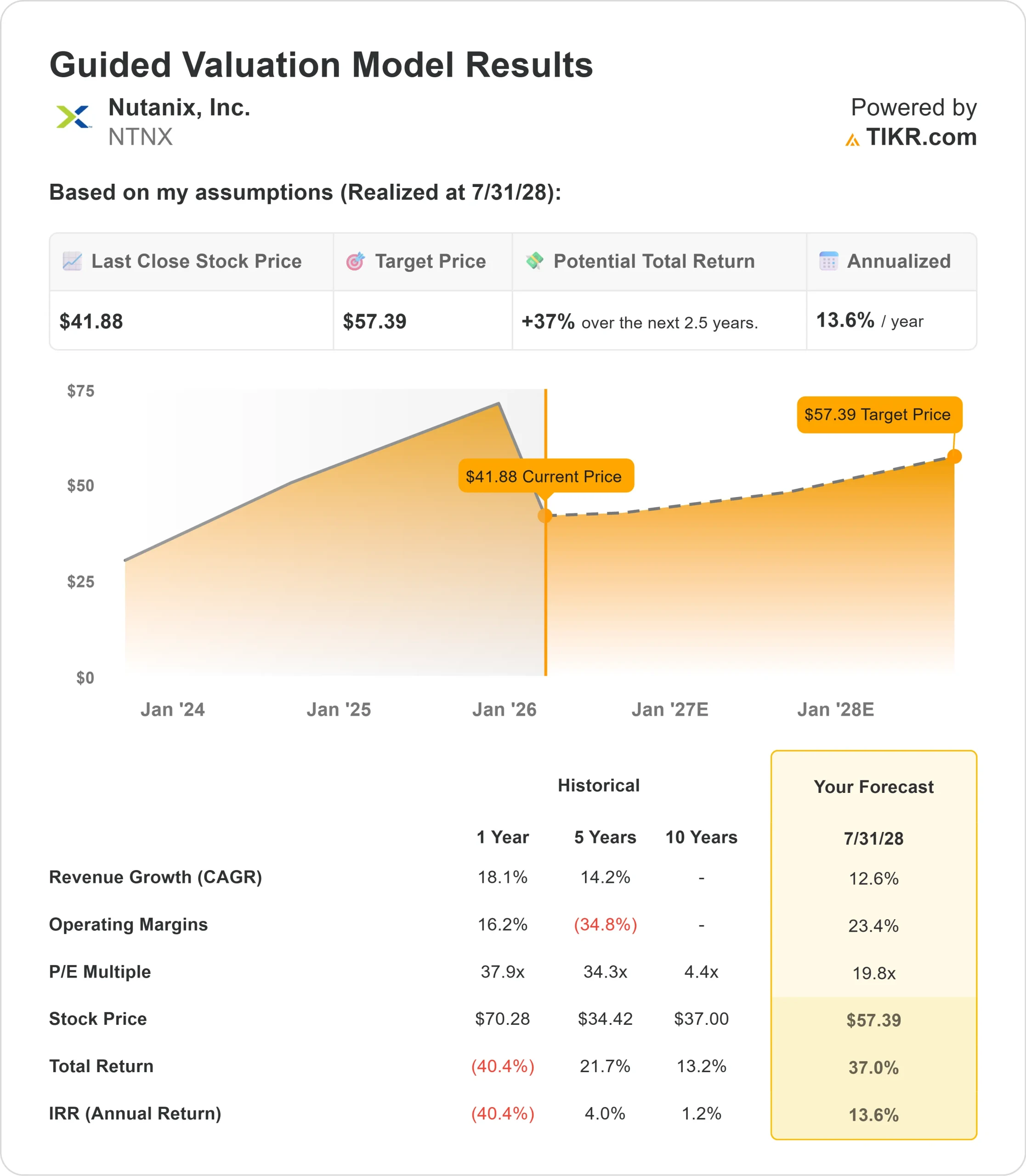

- Price Projection: Based on current fundamentals, NTNX stock could reach $57 by July 2028.

- Potential Gains: This target implies a total return of 37% from the current price of $42.

- Annual Return: Investors could see roughly 14% growth over the next 2.5 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

Nutanix (NTNX) delivered solid first-quarter fiscal 2026 results with bookings slightly ahead of expectations and 18% year-over-year ARR growth to $2.28 billion.

However, revenue guidance was reduced due to timing issues of revenue recognition related to customer flexibility needs and partner shipping dynamics.

CEO Rajiv Ramaswami emphasized that business fundamentals remain healthy, with the revenue guidance change driven solely by the timing of recognition, not by demand weakness.

- The company actually raised its free cash flow outlook while maintaining unchanged bookings expectations for the full year.

- Nutanix benefits from the massive enterprise migration away from VMware following Broadcom’s acquisition. Companies are evaluating alternatives to manage virtualization and hybrid cloud infrastructure, creating substantial opportunities for Nutanix’s platform.

- The company won notable deals in Q1, including a seven-figure deal with a Global 2000 customer in Europe’s energy sector and a North American agricultural products provider deploying the platform across its global operations.

- A European government agency selected Nutanix to run modern applications across public and private clouds using the company’s Kubernetes platform.

- Enterprise demand for hybrid multi-cloud solutions continues to expand as organizations modernize their infrastructure while maintaining flexibility.

- Nutanix’s ability to support both traditional virtualized workloads and modern containerized applications positions it well for long-term growth.

The company is also expanding hardware flexibility through partnerships with Dell and Pure Storage, allowing customers to deploy Nutanix software on external storage arrays. This reduces the barrier of requiring new hardware purchases during migrations.

See analysts’ full growth forecasts and estimates for NTNX stock (It’s free) >>>

What the Model Says for Nutanix Stock

We analyzed Nutanix’s transformation into a leading hybrid multi-cloud platform provider, capturing enterprise workloads migrating from VMware.

Using a forecast of 12.6% annual revenue growth and 23.4% operating margins, our model projects the stock will rise to $57 within 2.5 years. This assumes a 19.8x price-to-earnings multiple.

That represents compression from Nutanix’s historical P/E averages of 37.9x (one year) and 34.3x (five years).

The lower multiple acknowledges near-term revenue recognition timing challenges and the transition period as more business flows through OEM partners like Dell and Cisco.

Despite these headwinds, the company maintains strong free cash flow generation at 26% margin in Q1, with full-year guidance raised to $800-840 million. This demonstrates the underlying health of the business even as revenue timing shifts.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for NTNX stock:

1. Revenue Growth: 12.6%

Nutanix’s growth centers on capturing VMware migration opportunities and expanding within its existing customer base.

The company added 640 new logos in Q1 alone, building on 2,700 additions from the prior year.

Management expects double-digit revenue growth despite some business shifting to future periods due to customer requests for flexible license start dates aligned with migration timelines.

As more customers deploy workloads on the platform, expansion opportunities increase with additional products such as Kubernetes, unified storage, and database services.

2. Operating margins: 23.4%

Nutanix has significantly improved profitability over recent years, with operating margins expanding as the business scales.

Management maintains full-year margin guidance of 21-22% despite lower revenue, demonstrating operating discipline.

The company balances growth investments with efficiency improvements, benefiting from its subscription model, in which support revenue carries high margins.

As the revenue mix shifts toward renewals, margin expansion opportunities persist.

3. Exit P/E Multiple: 19.8x

The market currently values Nutanix at 22.2x earnings. We assume the P/E will compress moderately to 19.8x over our forecast period.

Near-term uncertainty around revenue recognition timing and the growing proportion of business through OEM partners are creating multiple pressures.

However, as Nutanix demonstrates consistent bookings growth and the migration opportunity unfolds over multiple years, the company should command a premium valuation for its strategic position in enterprise infrastructure.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Enterprise IT spending and migration timelines can vary significantly. Here’s how Nutanix stock might perform under different scenarios through July 2030:

- Low Case: If revenue growth slows to 10% and net income margins compress to 19.5%, investors still see a 38% total return (7.5% annually).

- Mid Case: With 11.1% growth and 20.9% margins, we expect a total return of 76% (13.4% annually).

- High Case: If VMware migrations accelerate and drive 12.2% revenue growth while Nutanix maintains 22.1% margins, total returns could reach 118% (19% annually).

See what analysts think about NTNX stock right now (Free with TIKR) >>>

The range reflects execution on enterprise migrations, maintaining customer momentum, and successfully navigating the revenue timing dynamics as the business model evolves.

How Much Upside Does Nutanix Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!