Key Takeaways:

- AI-Driven Growth: Cybersecurity demand surges as businesses deploy AI agents, expanding attack surfaces.

- Price Projection: Based on current execution, CRWD stock could reach $599 by January 2028.

- Potential Gains: This target implies a total return of 44% from the current price of $416.

- Annual Return: Investors could see roughly 20% growth over the next 2 years.

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free)>>>

CrowdStrike Holdings (CRWD) delivered an exceptional third quarter with record net new ARR of $265 million, up 73% year-over-year and beating expectations by over 10%. The company now sits at $4.92 billion in ending ARR, accelerating to 23% growth.

CEO George Kurtz highlighted relentless execution across the platform. The company posted an all-time record operating income of $265 million (21% of revenue) for the second consecutive quarter. Free cash flow hit a record $296 million, representing 24% of revenue.

- The business is firing on all cylinders. Endpoint ARR accelerated as AI adoption pushes new applications to employee devices.

- Falcon Next-Gen SIEM delivered record net new ARR as customers migrate from legacy solutions. Cloud security and identity businesses both posted strong sequential growth.

- More than $1.35 billion in ending ARR now comes from Falcon Flex subscriptions, growing over 200% year-over-year.

- This flexible licensing model is becoming the standard, making it easier for customers to consolidate their security stack on CrowdStrike’s single platform.

- The growth story centers on AI transformation. Organizations are deploying agentic workforces where humans and AI agents collaborate.

- Each agent creates a potential for an attack surface and requires protection. CrowdStrike provides both the armor to secure these agents and the intelligence layer to monitor threats.

Despite strong momentum and category leadership in cybersecurity, CrowdStrike trades at $416, offering meaningful upside for investors who recognize the company’s position as the operating system of enterprise security.

See analysts’ full growth forecasts and estimates for CRWD stock (It’s free) >>>

What the Model Says for CrowdStrike Stock

We analyzed CrowdStrike’s transformation into the cybersecurity platform of choice for the AI era. The company benefits from multiple structural tailwinds that are just beginning to unfold.

AI is democratizing both creation and destruction. State-sponsored adversaries now use large language models to create sophisticated cyber intrusion agents.

Anyone can “vibe hack” using AI and become a threat actor overnight. This reality is driving jarring lightbulb moments for businesses witnessing AI-powered attacks firsthand.

Companies realize that tab-switching between multiple security tools creates gaps where adversaries thrive.

CrowdStrike’s single-platform architecture delivers data, controls, and actions in one place. It’s the broadest and only true single-platform solution in cybersecurity.

The company’s AWS partnership validates this position. AWS selected Falcon Next-Gen SIEM as the default SIEM for millions of customers, offering it directly in the Security Hub console.

This product-led growth strategy opens CrowdStrike to significant new customer acquisition opportunities.

Based on a forecast of 21.8% annual revenue growth and 24.3% operating margins, our model projects the stock price will rise to $599 over 2 years. This assumes an 86.3x price-to-earnings multiple.

That represents compression from CrowdStrike’s historical P/E averages of 113.6x (one year) and 180x (three years). The lower multiple reflects the stock’s premium valuation and the natural normalization that comes with scale.

The real value lies in capturing secular growth in cybersecurity as AI adoption accelerates across industries and geographies, while expanding wallet share through platform consolidation.

Our Valuation Assumptions

Estimate a company’s fair value instantly (Free with TIKR) >>>

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for CRWD stock:

1. Revenue Growth: 21.8%

CrowdStrike’s growth centers on AI-driven security transformation.

- The company delivered 22% revenue growth in Q3 with broad-based acceleration across endpoints, cloud, SIEM, and identity.

- Management sees strong momentum continuing. Q3 net new ARR grew 73% year-over-year.

- The company expects second-half net new ARR growth of at least 50%, well above prior guidance of 40%.

- Looking ahead, CrowdStrike expects fiscal 2027 net new ARR growth of at least 20%.

AI adoption is supercharging endpoint demand. Employees deploy AI applications such as Claude Desktop and ChatGPT directly on their machines.

New AI browsers like Comet and Atlas deliver productivity gains but also introduce new vulnerabilities. The endpoint has become the epicenter of human-AI interaction.

2. Operating margins: 24.3%

CrowdStrike has expanded operating margins significantly while maintaining high growth. Q3 operating margin reached 21%, the second consecutive quarter of record operating income.

Subscription gross margins hit 81%, reflecting the platform’s efficiency advantages.

As the company scales and customers consolidate more modules onto Falcon, margin expansion continues through operational leverage.

The Falcon Flex model drives both growth and profitability.

Customers consume more of the platform faster, leading to higher retention and module adoption. Currently, 49% of subscription customers use six or more modules, up from prior periods.

3. Exit P/E Multiple: 86.3x

The market values CrowdStrike at 91.6x earnings currently. We assume the P/E will compress modestly to 86.3x over our forecast period as the company matures and the valuation normalizes.

Near-term, multiple compression risk exists given the premium valuation. However, CrowdStrike’s category leadership, platform advantages, and AI tailwinds support a premium to most software companies.

The AWS partnership, expanding MSSP market, and product-led growth through SIEM all provide upside catalysts.

As CrowdStrike demonstrates consistent execution across its global customer base, the market should continue valuing the stock at a premium.

Build your own Valuation Model to value any stock (It’s free!) >>>

What Happens If Things Go Better or Worse?

Cybersecurity faces evolving threats and technology shifts. Here’s how CrowdStrike stock might perform under different scenarios through January 2030:

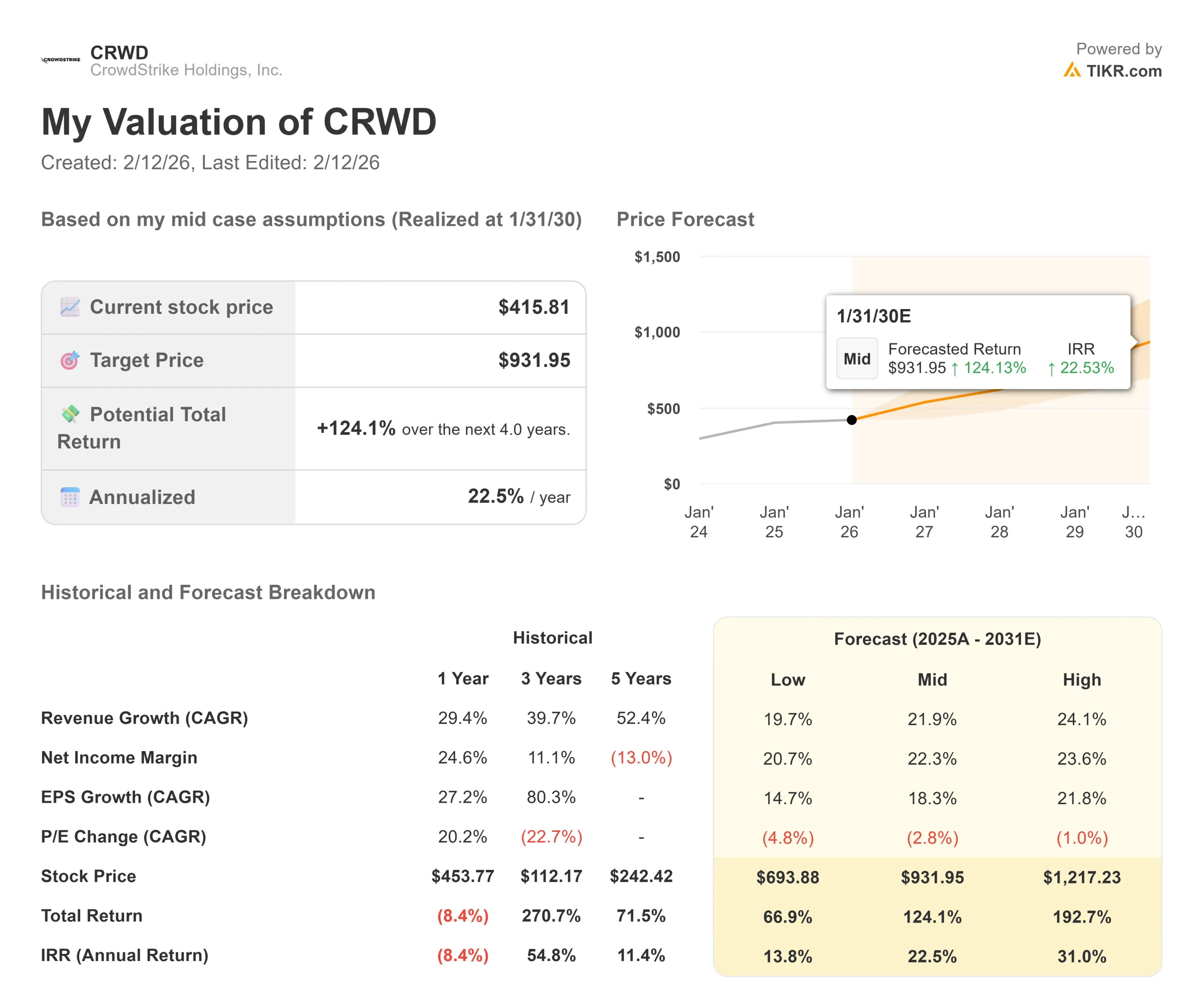

- Low Case: If revenue growth slows to 19.7% and net income margins compress to 20.7%, investors still see a 66.9% total return (13.8% annually).

- Mid Case: With 21.9% growth and 22.3% margins, we expect a total return of 124.1% (22.5% annually).

- High Case: If AI acceleration drives 24.1% revenue growth while CrowdStrike maintains 23.6% margins, returns could hit 192.7% total (31.0% annually).

See what analysts think about CRWD stock right now (Free with TIKR) >>>

The range reflects execution on AI-driven demand, successful platform consolidation, and the company’s ability to expand internationally while maintaining premium pricing power.

How Much Upside Does CrowdStrike Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!