Key Stats for Costco Stock

- This Week Performance: +1%

- 52-Week Range: $844 to $1,067

- Current Price: $944.8

What Happened?

Costco stock (COST) sits at $994.76, hovering just below the $1,000 psychological threshold after the Supreme Court’s February 20 IEEPA ruling cleared a path for the warehouse giant to recover a share of $175 billion in disputed tariff duties it helped sue to reclaim.

Wall Street moved swiftly in response to the strengthening fundamental backdrop, with JP Morgan raising its price target on Costco to $1,050 from $1,000 and Bernstein lifting its target to $1,155 from $1,146 on February 9, underscoring growing analyst conviction in the stock’s upside.

The engine driving that conviction is Costco’s January sales report, which showed total net sales surging 9.3% to $21.33 billion, powered by digitally-enabled sales jumping 34.4% and U.S. comparable sales climbing 5.8% even as gas deflation dragged reported comps by roughly 100 basis points.

Beyond the headline numbers, the market is quietly re-rating Costco from a defensive consumer staple into a digitally-driven, high-income growth platform, as households earning over $100,000 increasingly fuel its e-commerce expansion and push traffic up 2.2% domestically in January.

Andrew Yoon, Director of Finance and Investor Relations, stated on the January sales call that “total company comparable sales for the month, excluding all gas sales and the impact of foreign exchange, was 7.3%,” underscoring how underlying demand momentum remains considerably stronger than headline figures suggest.

Adding further institutional weight, Bernstein’s raised target of $1,155 represents roughly 16.1% upside from the February 25 close of $994.76, signaling that at least one major research desk sees Costco’s current price as a meaningful discount to fair value.

Looking further out, Costco’s simultaneous wins on tariff litigation, digital commerce acceleration, and affluent customer acquisition position it to widen its competitive moat against rivals like Amazon and Walmart over the next 3 to 5 years, as its 924-warehouse global footprint becomes an increasingly rare and defensible asset.

Wall Street’s Take on COST Stock

The Supreme Court’s February 20 IEEPA ruling directly strengthens Costco’s forward earnings picture, as potential recovery from the $175 billion tariff refund pool removes a meaningful cost overhang that had been compressing margins across its import-heavy merchandise categories.

Underneath that legal tailwind, Costco’s fundamentals show a business in steady acceleration, with revenue forecast to grow 8.1% to $297.6 billion in fiscal 2026 and normalized EPS climbing 11.8% to $20.36, extending a multi-year streak of double-digit earnings compounding.

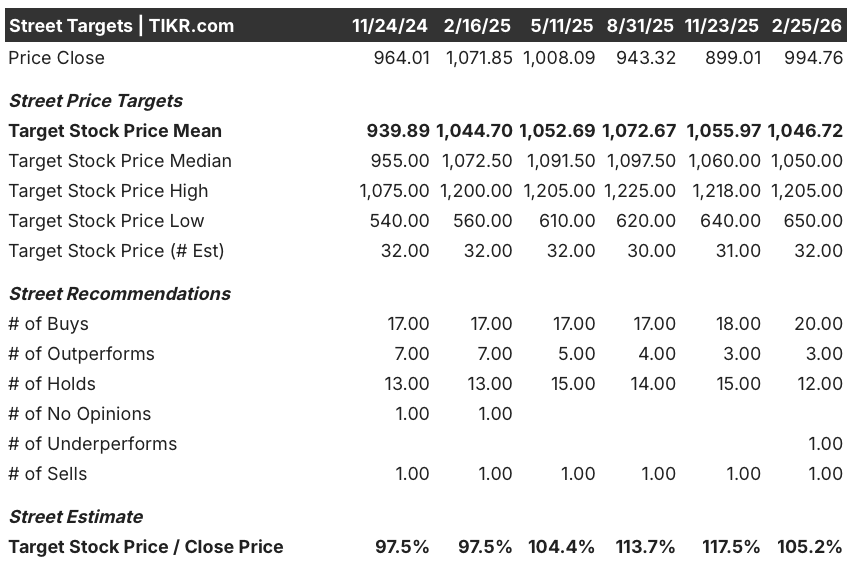

However, Wall Street stands firmly bullish on COST, with 20 buys, 3 outperforms, and 12 holds against just 1 sell as of February 25, producing a mean price target of $1,046.7 that implies 5.2% upside from the current $994.76 close, with analysts holding conviction through a recent pullback from the 52-week high of $1,067.1.

The spread between the analyst low of $650.0 and the high of $1,205.0 is wide enough to demand attention, with the bull case hinging on sustained digital sales acceleration and affluent customer retention, while the bear case reflects multiple compression risk at a stock trading near a 45x price-to-earnings ratio.

What Does the Valuation Model Say?

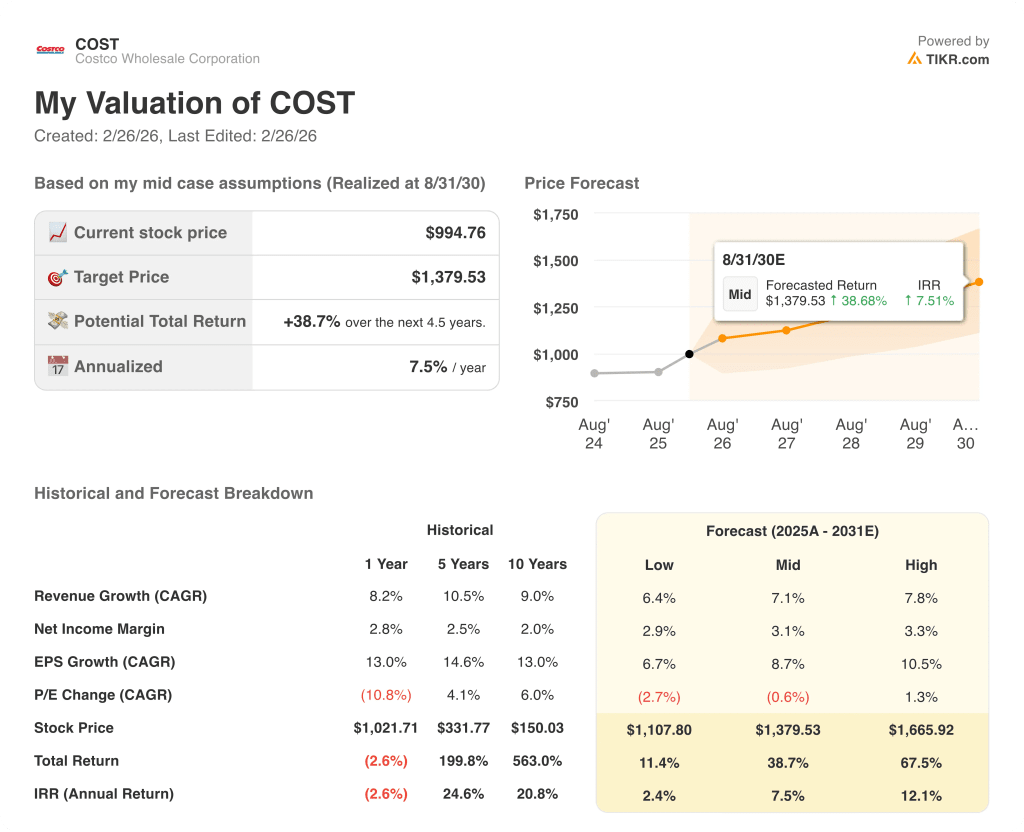

Given Costco’s 8.2% one-year revenue CAGR, 13% EPS growth, and improving net income margins trending toward 3.1% in the mid case, TIKR’s valuation model prices COST at a mid-case target of $1,379.5, implying a 38.7% total return over 4.5 years at a 7.5% annualized IRR.

The most consequential risk visible in the estimates is P/E multiple compression, where the model’s mid case already prices in a -0.6% P/E CAGR, meaning Costco must sustain earnings momentum just to prevent valuation erosion as the market reassesses growth-stock premiums in a higher-rate environment.

Altogether, COST looks modestly undervalued relative to its fundamental trajectory, with the tariff ruling, digital sales acceleration, and affluent customer expansion forming a credible growth runway, though investors should watch whether fiscal 2026 EPS delivery of $20.36 materializes on schedule as the key confirmation signal.

Should You Invest in Costco Wholesale Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up COST stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Costco Wholesale Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze COST stock on TIKR for Free →