Key Stats for Corning Stock

- Current Price: $255.69

- Target Price (Mid): ~$425

- Street Target: ~$206

- Potential Total Return: ~66%

- Annualized IRR: ~12% / year

- Earnings Reaction: -0.75% (April 28, 2026, Q1 report)

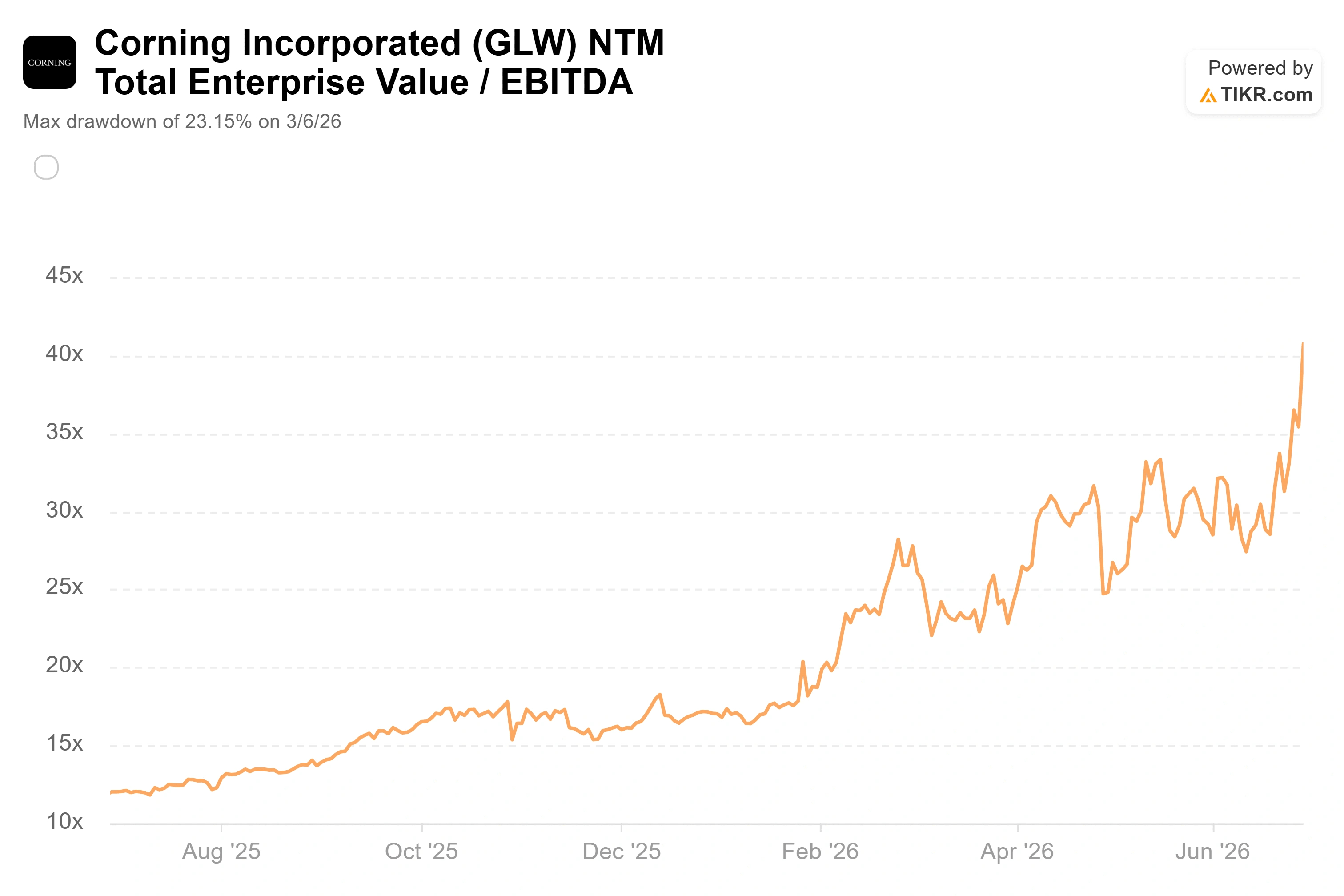

- Max Drawdown: 23.15% (March 6, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Corning (GLW) just closed at a record high on a day when almost nothing changed at the company itself. Shares finished at $255.69 on June 29, up 15.67%, after a set of mechanical, calendar-driven events pushed fund money into the stock at once. There was no earnings release and no new contract that day. The buying was largely structural.

That is the strange tension sitting under this stock right now. The business underneath has genuinely changed, and yet the latest leg of a 192% year-to-date run was triggered by index and calendar mechanics, not by fresh fundamental news. Bulls see a materials company that finally became an AI infrastructure company. Bears see a 175-year-old glassmaker trading at 123 times trailing earnings, partly because passive funds were told to own more of it. The question the market cannot yet answer is which version is setting the price.

Why Corning stock 2026 jumped on index mechanics, not earnings

The biggest catalyst was the FTSE Russell reconstitution. Every June, FTSE Russell recalculates which stocks belong in its US indexes and whether each one counts as growth or value. According to LSEG, the 2026 style changes took effect at the market open on June 29, the exact day GLW spiked. Corning shifted toward the growth side of the Russell style indexes, and roughly $12 trillion is benchmarked to the Russell family, so a reweighting of that size pulls in real buying as growth funds rebalance.

Index moves are usually telegraphed weeks ahead and largely priced in before the effective date, which is why a 16% single-day pop points to more than one driver. Two calendar effects piled on. Investors positioned ahead of Corning’s $0.28 per share dividend, payable September 29 to holders of record on August 31, and quarter-end “window dressing,” where funds add strong performers before reporting, added fuel on the last business day of Q2. Month to date, the stock had already climbed roughly 41% into the event. None of this changes the long-term thesis, but together it explains why the move was this violent and this fast.

The reason the reclassification mattered so much is what put Corning in the growth bucket in the first place. The company has spent two years rewiring itself around the data center. Optical Communications, its fiber and cable business, grew 36% last quarter, and three of the largest technology spenders in the world have now signed long-term supply deals: Meta committed up to $6 billion in January, NVIDIA followed in May with capital attached, and Amazon signed a multiyear fiber agreement in June. That is the story the index finally caught up to.

See historical and forward estimates for Corning stock (It’s free!) >>>

What management is actually promising

The deals matter less for their size than for their structure, and that is where management has been most direct. At the J.P. Morgan technology conference on May 19, CFO Edward Schlesinger described the NVIDIA arrangement in plain terms: “NVIDIA is actually providing a multibillion dollar prepayment to support that capital deployment and they’re making an equity investment.” That sentence is the whole bull case in miniature. The customer funds the factory and commits to fill it, which removes the classic risk that Corning builds expensive capacity and then waits for demand that may not arrive.

The plan attached to those deals is large. Management has extended its “Springboard” growth framework, raising the sales run-rate target to $40 billion by the end of 2030, with a high-confidence floor between $35 billion and $40 billion. Schlesinger framed the engine behind it as the enterprise business growing “1.5x the rate of GPU growth” for the next few years. For a company that did about $16.4 billion in revenue in 2025, that is more than a doubling, underwritten in part by customer prepayments.

Here is why that one quote should matter to investors: prepayments and minimum volume commitments are the difference between a backlog and a forecast. If the cash is arriving before the capacity is built, the growth is closer to contracted than hoped for. That is precisely the feature a stock at this valuation needs in order to defend itself.

The valuation is the entire argument

And the valuation is steep by any honest measure. At $255.69, Corning trades at roughly 123 times trailing twelve months earnings and about 76 times forward earnings, levels the market normally reserves for software, not for a capital-intensive manufacturer. The Street has not kept pace with the price. The mean analyst target sits at around $206, which is below where the stock closed, and the current breakdown is 11 Buys, 1 Outperform, 4 Holds, 1 Underperform, and 1 Sell. A consensus target trailing the market price tells you the rally has outrun the analysts who cover it.

The peer comparison sharpens the point. On an NTM EV/EBITDA basis, Corning trades at about 40.7 times, against roughly 35.0 times for Coherent and 21.5 times for IPG Photonics, with the peer group median near 21.6 times. So Corning carries close to double the multiple of its median optical peer. The premium is partly justified. Corning has the signed hyperscaler agreements and the integrated US manufacturing base that the others lack, and it is the named supplier to NVIDIA, Meta, and Amazon. But “partly justified” is not the same as “fully priced in,” and at 40 times forward EBITDA, the stock is pricing the high-confidence plan as if it has already happened.

The bears have two near-term flags worth respecting. Q2 core sales were guided to about $4.6 billion, just under the roughly $4.67 billion consensus, and insiders sold meaningful stock into the June strength, including more than $30 million in disclosed sales near the highs. Neither breaks the thesis. Both are reasons to question whether a 16% melt-up driven mostly by index and calendar flows was the market discovering value or simply the market being pushed to buy.

The cash question is the one that actually decides this. Free cash flow was $1.72 billion in 2025, and capital spending is climbing to fund the optical ramp. A stock priced this richly needs profit to convert to cash, not the reverse. Schlesinger’s answer was timing: he argued incremental net income should “convert to cash at almost 100%,” which would lift overall conversion as the new revenue lands. If that holds, today’s heavy capex is an investment phase. If it slips, a triple-digit multiple has very little to lean on.

See how Corning performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $255.69

- Target Price (Mid): ~$425

- Potential Total Return: ~66%

- Annualized IRR: ~12% / year

See analysts’ growth forecasts and price targets for Corning stock (It’s free!) >>>

Using the TIKR mid-case scenario, which realizes on December 31, 2030, the model points to a target of around $425, or roughly 66% total upside over about 4.5 years, an IRR of around 12% per year. The mid-case is used here rather than the high case because the bull story is already partly in the price, and the more interesting question is whether the stock can still work without everything going right.

Two revenue drivers carry the model. The first is enterprise optical demand tied to data center buildouts, which management expects to grow at roughly 1.5x the rate of GPU growth. The second is the broader optical and emerging portfolio, including carrier fiber, solar, and the early photonics opportunity management sizes at a $10 billion market by 2030. The margin driver is operating leverage: Corning has moved operating margin from 16% to about 20% and expects to hold at or above that level while it scales, with the model assuming a net income margin climbing toward 18% in the mid case.

The primary risk is conversion. If capital spending on the optical ramp keeps free cash flow lagging net income, the valuation loses its support.

The upside: contracted hyperscaler demand and customer prepayments let Corning compound revenue at a mid-teens rate, near the 15.6% the model assumes and below management’s own roughly 19% total-company projection, while improving cash conversion and justifying the premium.

The downside: the AI capex cycle cools or the photonics inflection slips past 2027, and a stock at 76 times forward earnings re-rates hard toward its peers.

Conclusion

The next real test is Q2 earnings in late July. Watch one number above all: Optical Communications growth. It grew 36% last quarter. A print holding in the low-to-mid 30s, paired with free cash flow starting to close the gap with net income, would confirm the hyperscaler contracts are converting and give the path toward around $425, a foundation that does not depend on index flows. A clear deceleration, or another quarter where cash conversion lags, would suggest the June surge was a mechanical event dressed up as a fundamental one. At 123 times earnings, Corning does not get the benefit of the doubt for long, and the late-July report is when the market stops trading the index reshuffle and starts trading the business again.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Corning?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Corning, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Corning alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Corning on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!