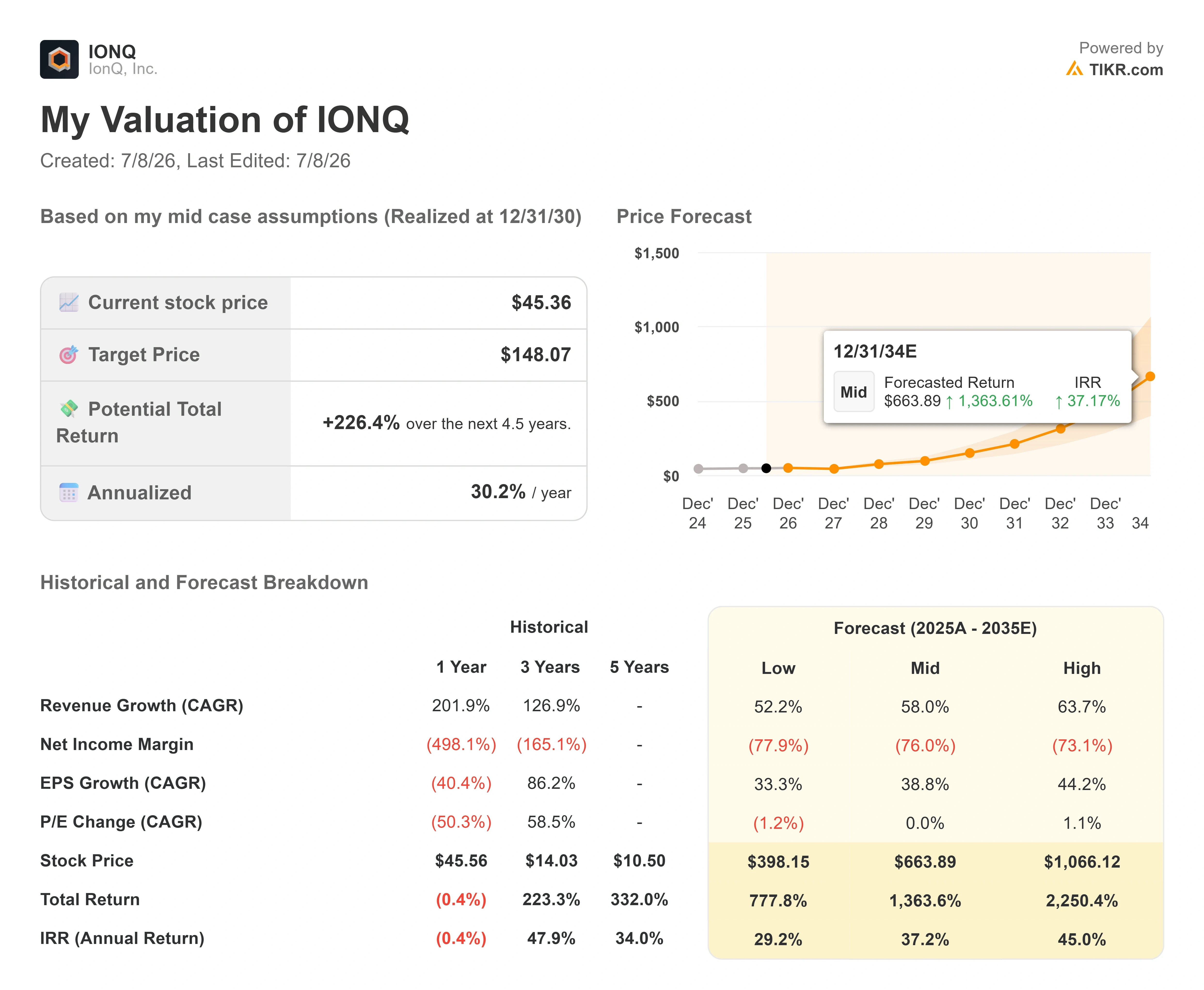

Key Stats for IonQ Stock

- Current Price: $45.36

- Target Price (Mid): ~$150

- Street Target: ~$69

- Potential Total Return: ~225%

- Annualized IRR: ~30% / year

- Earnings Reaction: -9.30% (May 6, 2026)

- Max Drawdown: -67.61% (March 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

IonQ (IONQ) has become the stock investors love right up until they decide to sell it. Shares fell 7.18% in a single session on July 7 to close at $45.36. That one-day drop capped a brutal stretch, with the stock down roughly 31% over the prior month. What makes the selling strange is what did not cause it. There was no earnings miss that day, no lost contract, no guidance cut. The quantum computing leader is still posting record revenue and still raising its outlook. Yet the market keeps hitting the sell button, and the disagreement underneath that selling has not been resolved.

The bulls and bears are arguing about two different things. Bulls are looking at the business, which is scaling faster than almost anyone modeled a year ago. Bears are looking at the price, which still values a company with heavy losses at nearly 80 times trailing revenue. The question the market cannot yet answer is which lens is correct, because the thing that would settle it, sustained profitable scale, is still years out. That gap between a strong business and an anxious tape is the entire story right now.

What Actually Triggered the Latest Drop

The July 7 selloff was a sector event, not a company event. Investor caution swept across quantum computing names as commentary focused on the group’s extreme price-to-sales multiples and the speculative nature of stocks priced years ahead of profits. Adding a fresh competitive worry, Finnish firm IQM Quantum Computers began trading on the Nasdaq on July 2 under the ticker IQMX, becoming the first European quantum company to list on a major U.S. exchange at a valuation of roughly $1.9 billion. A new listing gives quantum-focused capital another place to go, and that competition for investor dollars showed up in IonQ’s price.

The irony is that IQM’s own debut carried a warning that applies to the entire field. Its prospectus stated plainly that large-scale commercial traction of quantum computing may never occur, and its shares spent most of their first day below the offer price. That candor reframed the sector for investors who had been paying rally prices, and IonQ, as the most-watched name in the group, absorbed the mood shift.

June had already softened the stock. Shares fell roughly 26% over the month even as good news arrived, including inclusion in the Russell 1000 and Russell Midcap indices at the end of June, a change that widens the pool of institutional investors that can hold the shares. Several directors and executives also sold stock in June, though the filings show these were routine sales under pre-arranged Rule 10b5-1 plans and RSU tax-cover transactions rather than discretionary exits. Even so, insider selling into a falling price rarely calms nervous holders.

The Business the Market Is Selling

Here is the tension in sharpest form. On May 6, IonQ reported its largest quarter on record, with GAAP revenue of $64.67 million, up 755% year over year, beating the consensus estimate of $49.73 million by 30.03%. Management raised full-year 2026 guidance to a range of $260 million to $270 million, which roughly doubles 2025’s $130.02 million. The stock still fell 9.30% the next session. This is a business the market keeps selling on days it executes.

The composition of that revenue matters more than the headline. Roughly a third of the quarter’s revenue came from customers buying more than one product across IonQ’s four lines, which span computing, networking, sensing, and security. That cross-selling is direct evidence of platform stickiness, the thing that separates a hardware vendor from a durable franchise. Remaining performance obligations, meaning contracted future revenue not yet recognized, stood at $470 million as of March 31, up 554% year over year. For a company guiding to $265 million at the midpoint this year, that backlog is a real anchor under the guidance.

Management has been consistent about what is driving the roadmap. Speaking at the J.P. Morgan Technology, Media and Communications Conference on May 18, Chief Financial Officer and Chief Operating Officer Inder Singh framed the company’s edge as a cost and simplicity story, not just a physics story. “The ability to have electronic control means fewer lasers. Fewer lasers means lower cost,” he said, describing the shift from laser-based systems to chip-based control that underpins the next-generation 256-qubit machine. That matters because it ties IonQ’s scaling to the mature semiconductor supply chain rather than to exotic, hard-to-manufacture hardware, which is the crux of the bull thesis on cost of ownership.

There is also a new commercial catalyst the earlier selloff narrative ignored. On June 17, IonQ launched Clavis XG Multiplex, a quantum-key-distribution system built to run over existing fiber without infrastructure upgrades, aimed at generating recurring security revenue from metro networks. Quantum security is the part of the platform that can sell today, before fault-tolerant computing arrives, and a deployable metro product widens that near-term revenue path.

See historical and forward estimates for IonQ stock (It’s free!) >>>

Whether the Fear Is Rational

The bear case is not hard to state, because it is mostly about the price. IonQ trades at around 80 times trailing twelve-month revenue and around 54 times next-twelve-months enterprise value to revenue, multiples that leave no room for execution stumbles. Free cash flow is projected to stay negative through the end of the decade, with the TIKR consensus not showing positive FCF until 2030. The company carries a five-year beta of 3.05, so it swings far harder than the market in both directions, which is exactly why a sector wobble becomes a 31% drawdown here. When a stock is priced for a specific future, any reason to doubt that future gets amplified.

The bull case answers with the trajectory. Revenue grew 755% last quarter and is set to roughly double this year, the backlog is growing faster than recognized revenue, and the platform is expanding into networking, sensing, and security while competitors mostly sell one thing. The balance sheet removes the near-term survival question that hangs over weaker quantum names, with around $2.0 billion in net cash on the books. Where the bear sees an unjustifiable multiple, the bull sees the early revenue line of a company that could dominate a category, and a selloff driven by sentiment rather than by anything IonQ did.

The competitive frame sharpens the valuation question rather than settling it. Against listed peers, IonQ’s roughly 54x forward EV/revenue sits below Quantinuum (QNT) at around 110x, and above Quantum Computing Inc. (QUBT) at around 19x, using TIKR’s competitor data. So IonQ is neither the most nor the least expensive quantum name on that measure. The premium the market assigns it reflects scale and platform breadth rather than a discount to the group, which means the stock needs to keep out-executing to hold its multiple. That is the honest read: the valuation is defensible only if the growth stays exceptional.

See how IonQ performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $45.36

- Target Price (Mid): ~$150

- Potential Total Return: ~225%

- Annualized IRR: ~30% / year

See analysts’ growth forecasts and price targets for IonQ stock (It’s free!) >>>

The TIKR Valuation Model, using its mid-case assumptions, targets around $150 for IonQ by the end of 2030. From the current $45.36, that implies a potential total return of around 225% over the next four and a half years, or an annualized return of around 30% per year. This is the mid-case, chosen because it reflects strong but not heroic execution, which fits a company beating estimates while still years from profitability.

Two revenue drivers power the forecast. The first is the computing platform scaling from the current Tempo system into the chip-based 256-qubit machine, moving IonQ deeper into enterprise and government accounts. The second is the networking and security lines, including products like Clavis XG Multiplex, expanding into sovereign and metro customers who buy before fault-tolerant computing arrives. The margin driver is gross margin recovery as higher-margin software and multi-product revenue grows as a share of the mix. The primary risk is timeline: a slip in the qubit roadmap resets the commercial curve and the model with it.

The upside is that IonQ converts its backlog and platform breadth into durable, higher-margin revenue, and the mid-case return compounds at around 30% a year. The downside is that quantum’s commercial inflection stays perpetually a few years away, in which case an 80x revenue multiple has a long way to fall.

Conclusion

The next real test is IonQ’s Q2 2026 earnings, expected later this summer, and management already handed investors the number to watch: Q2 revenue guidance of $65 million to $68 million. A print inside or above that range, with the multi-product revenue share holding above a third and RPOs still climbing, confirms that the platform is compounding and that the selloff was sentiment, not signal. A miss, or a first sign of the backlog stalling, tells you the bears reading the multiple were right to be nervous. Everything else, the index inclusions, the analyst targets, the roadmap slides, is noise until that quarter lands. Watch the revenue and the backlog, not the headlines.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in IonQ?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up IonQ, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track IonQ alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!