Key Takeaways for Duolingo Stock as of July 2026

- With adjusted EBITDA guided to fall 9% in the third quarter before climbing 17% by mid-2027, Duolingo stock still looks underpriced against that reacceleration than the Street’s targets currently reflect.

- Twenty-three analysts split 18 holds, two buys and one sell, and the $106 mean target sits 19% below Wednesday’s $132 close.

- IKR’s mid-case model still calls for $197 by December 2030, a 49% total return worth 9% annualized over 4.5 years.

- Just 12% of monthly active users pay for Duolingo, well below Spotify’s near-50% conversion rate.

Duolingo Stock Fell 12% on a Beat as EBITDA Margins Compress Into 2026

Duolingo (DUOL) stock fell 12% after its Q1 earnings call, even as first-quarter revenue climbed 27% to $292 million and beat the $288.5 million analysts expected. The drop centered on a full-year plan that trades near-term monetization for user growth, with management guiding bookings up just 10.5% for 2026.

That growth came from the user base, not price. Daily active users rose 21% to 56.5 million while paid subscribers climbed 21% to 12.5 million, extending Duolingo’s freemium conversion.

Still, that conversion has room to run. CEO Luis von Ahn noted that roughly 12% of monthly active users currently pay, well below the near-50% rate at Spotify, one of the few freemium comparisons at Duolingo’s scale.

On the profitability side, CFO Gillian Munson addressed the quarter’s investment tradeoff directly on the call: “We achieved double-digit growth in both bookings and revenue expanded gross margin and delivered adjusted EBITDA of $83 million, which is about 29% of our revenue.”

Adjusted EBITDA grew 33% year over year at that 29% margin, even as management guided gross margin down toward 69% by year-end on rising AI compute costs. Full-year guidance holds adjusted EBITDA at $310 million, about 25% of revenue, with the trough landing in the third quarter before working through last year’s toughest comparisons from the Energy feature launch and price increase.

Beneath the margin pressure, product velocity kept climbing: Duolingo published 20,500 course units in the quarter, over 10 times its pace two years ago, pushing all nine of its most-taught languages to Duolingo Score 129, the CEFR B2 equivalent.

The Street’s reaction lagged that pace. J.P. Morgan raised its target by just $2 to $94 right after the print while keeping a neutral rating, a signal analysts want the margin trough to bottom before pricing in the 2027 reacceleration management is promising.

Wall Street Rates DUOL Stock a Hold as Targets Trail the Stock Price

Twenty-three analysts cover Duolingo stock, and 18 rate it a hold against four buy-equivalent ratings and one sell. The $106 mean target sits 19% below the current $132 price, while even the $145 high estimate trails TIKR’s own $197 mid-case figure.

J.P. Morgan’s reaction to the print, a $2 increase to $94 while holding a neutral rating, captured that caution, since the bank raised its number without changing its stance. That combination leaves Duolingo stock trading above where most of the Street currently expects it to land.

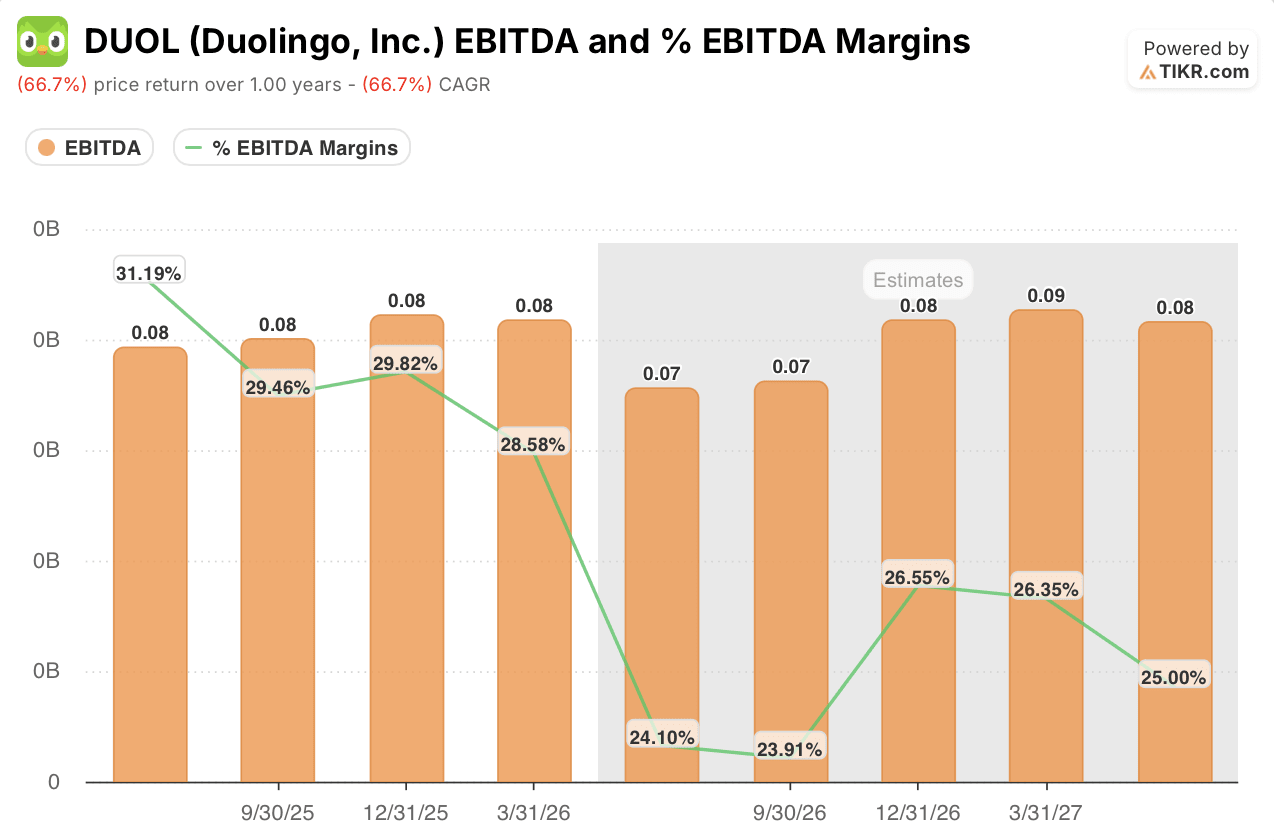

Wall Street Expects DUOL Stock’s EBITDA Growth to Trough Before a 2027 Rebound

Duolingo’s most recent quarter delivered adjusted EBITDA growth of 33% year over year, with margins at 29% of revenue. That pace reverses over the next two quarters. Consensus has EBITDA declining 10% in the second quarter and 9% in the third, with margins compressing to 24%.

Growth flattens by the fourth quarter, with EBITDA down just 1% and margins near 27%. It turns positive again in the first quarter of 2027, up 3% at a 26% margin.

The real test lands in the second quarter of 2027, when consensus has EBITDA growth accelerating to 17% at a 25% margin, the clearest signal yet that the investment year is paying off.

TIKR Values Duolingo Stock at $197 Through 2030

TIKR’s mid-case model values Duolingo stock at $197 by December 2030, implying 49% total return from the current price of $132, or 9% annualized over 4.5 years.

That return reflects a business TIKR sees compounding through both continued user growth and steadily improving profitability, not a single margin line item.

The target is reachable because two dynamics already in motion, record course-content output and daily active users past 56 million, support the same durable business TIKR’s model is pricing in. The EBITDA trough now underway is the near-term test of that case.

Should You Invest in Duolingo, Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Duolingo, Inc. stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Duolingo, Inc. alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze DUOL stock on TIKR for Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!