Key Stats for SanDisk Stock

- Current Price: $1,617.70

- Target Price (Mid): ~$2,970

- Street Target: ~$1,980

- Potential Total Return: ~84%

- Annualized IRR: ~16.5% / year

- Earnings Reaction: +8.25% (April 30, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

SanDisk (SNDK) has put analysts and the market on opposite sides of the same trade. On July 6, Goldman Sachs raised its price target by 83%. Two sessions later, the stock broke below $1,500 for the first time. That gap is the story right now. One side is buying the dip in slow motion through research notes, and the other is selling it in real time on the tape.

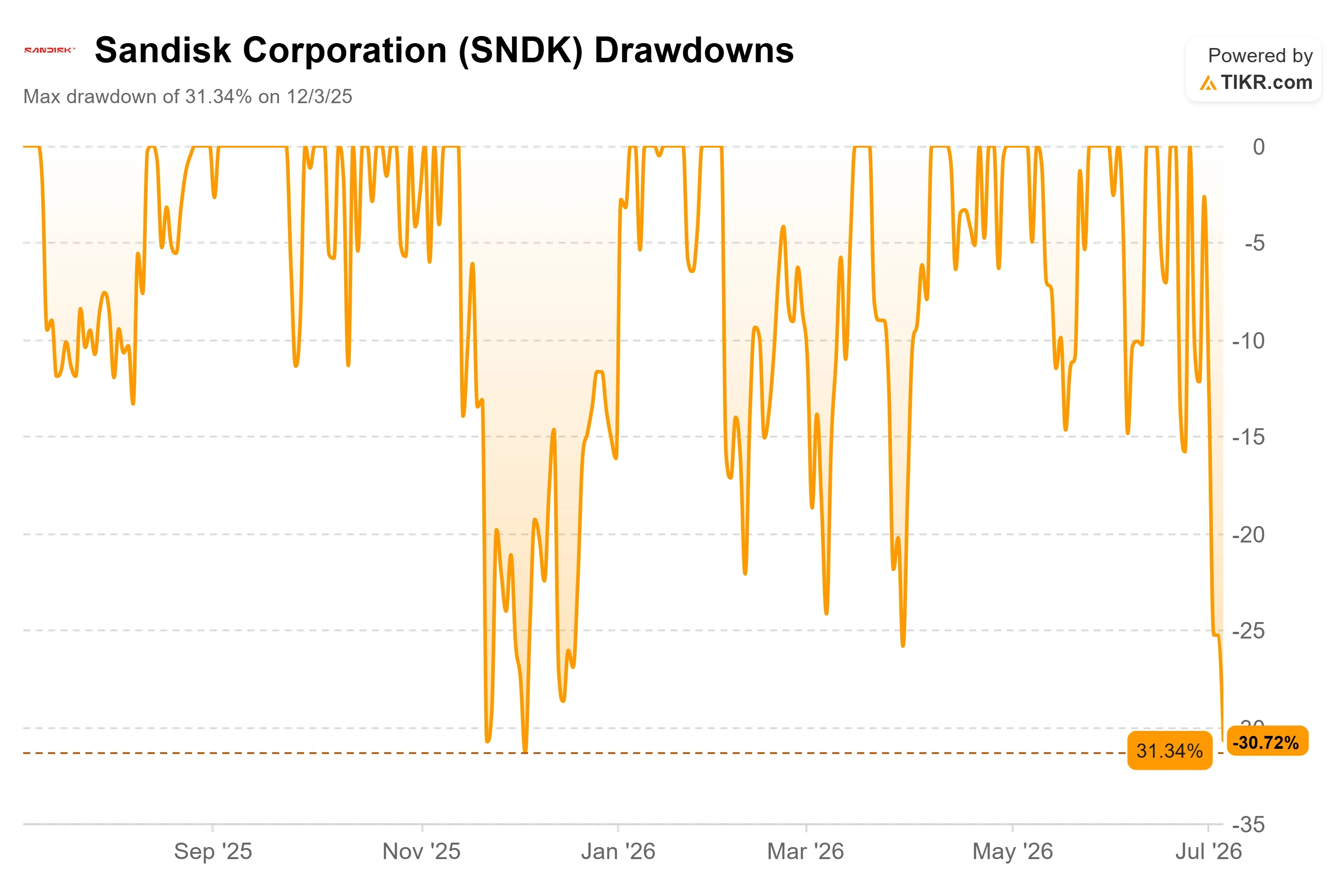

The numbers frame the standoff. SanDisk closed at $1,617.70 on July 7, down roughly 31% from its June 22 all-time high of $2,354.39, and it touched an intraday low near $1,485 the next session before recovering, according to intraday market data. Yet the average Street target sits at $1,975.95, above the current price. When a stock trades 30% below its high while the consensus target sits above spot, someone is early and someone is wrong.

The question the market cannot yet answer is simple. Is NAND flash, the memory technology that stores data in phones, drives, and AI servers, still the same boom-and-bust commodity that has always carried a low multiple? Or has the AI build-out changed the cycle enough to justify the targets analysts keep raising?

The Upgrade That Landed Into a Selloff

The freshest catalyst is the one investors ignored. On July 6, Goldman Sachs analyst James Schneider raised his SanDisk target to $2,200 from $1,200 and reiterated a Buy, projecting a “very strong quarter” ahead of fiscal fourth-quarter results in August. His adjusted EPS estimate for calendar 2026 runs nearly 30% above Street consensus, driven by tight NAND supply and improving enterprise solid-state drive mix at hyperscale customers.

Goldman was not alone. In late June, Bernstein lifted its target to $3,000 from $1,700, and Bank of America moved to $2,500 around the start of July. The direction of the revisions is unambiguous. So is the direction of the stock. SNDK rose only about 3% to 5% the day Goldman published, then kept sliding as the broader memory group sold off. The upgrade barely dented a stock in a full-blown correction.

That disconnect is the entire debate. Analysts are pricing durable, structurally higher earnings. The market is pricing a cyclical peak.

See historical and forward estimates for SanDisk stock (It’s free!) >>>

Why the Stock Is Falling When the Business Is Not

The selloff did not start inside SanDisk. It started 7,000 miles away. Samsung Electronics posted record preliminary Q2 operating profit near 89 trillion won, a roughly 19-fold jump year over year, and memory stocks sold off anyway. That reaction told investors the good news was already in the price. Concerns then centered on capacity: announced supply additions from Samsung and SK Hynix could soften NAND pricing just as the AI capital spending cycle is expected to peak.

For SanDisk, the fear is specific. A large share of its output still sells on the open market. Reporting on the company’s fiscal 2027 supply indicates that its multi-year agreements cover more than a third of its bit supply, which leaves the majority exposed to spot pricing. If NAND prices roll over, those uncommitted volumes take the hit, and the company’s LTM gross margin of 56.0% comes under pressure. That is the bear case in one sentence, and it is not a strawman.

SanDisk also pushed out a fresh operational proof point that the tape shrugged off. In early July, SanDisk and manufacturing partner Kioxia began volume production of tenth-generation 3D NAND at their Fab2 facility in Kitakami, Japan, using a CMOS-bonded-to-array design that lifts density and efficiency. It is exactly the kind of milestone that supports the long-term story. It moved the stock not at all.

What Management Actually Said About the Cycle

This is where the conference transcript matters more than any research note. At the Mizuho Technology Conference on June 9, 2026, CEO David V. Goeckeler took the cyclicality question head-on and refused to pretend the skepticism was unfair. Asked how he convinces investors that this time is different, he pointed to the industry’s history directly: “There’s so much scar tissue, and there’s so much history.” His answer was a method rather than a promise: “You just keep putting points on the board.” That tone matters, because it signals management knows the burden of proof sits with them.

The substance behind the confidence sits with the CFO. Luis Visoso described the company’s New Business Model agreements, meaning multi-year supply contracts structured with a pricing floor and ceiling so neither side gets whipsawed by the cycle. His most important line addresses the exact fear driving the selloff. Even at the low end of the pricing band, Visoso said, “we like the margins,” adding that they “will be consistent with the margins that we guided for the fourth quarter.” Goeckeler drew the boundary on what the deals are for. “We’re not trading duration for price,” he said, adding that “the value proposition is continuity of supply.” That is the direct rebuttal to the spot-exposure worry. It does not erase the risk on uncommitted bits, but it puts a high floor under a meaningful and growing share of them.

There is also a second growth engine still loading. Goeckeler confirmed that fiscal Q4 2026 is the first quarter SanDisk recognizes revenue from Stargate, its high-capacity enterprise SSD line built for AI storage workloads. One engine, the performance NAND used in AI inference caching, is fully ramped. The other is just switching on.

Where the Valuation Sits After the Drop

Here is what complicates the “priced for a peak” narrative. After the correction, SanDisk trades at 9.12x NTM P/E and 6.58x NTM EV/EBITDA, per TIKR. On forward earnings, that is not an expensive stock. Its former parent, Western Digital, and diversified peer, Samsung, anchor the range on either side. Within TIKR’s Technology Hardware peer set, Samsung trades at 2.10x NTM EV/EBITDA and 5.13x NTM P/E, reflecting its conglomerate mix, which leaves SanDisk at a premium to Samsung but nowhere near a bubble multiple in absolute terms. The debate is not whether the multiple is stretched. It is whether the earnings that multiple sits on are durable.

The balance sheet strengthens the bull side. SanDisk now holds a net cash position, with LTM net debt of negative $3.53 billion, and management paired its results with a $6 billion share buyback authorization. A company priced for imminent collapse does not usually carry net cash and buy back stock. The risk in this name lives in the durability of the earnings, not the valuation placed on them. If NAND pricing holds into 2027 as management and Goldman expect, the analysts are early. If capacity additions crack pricing first, the tape is early.

See how SanDisk performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $1,617.70

- Target Price (Mid): ~$2,970

- Potential Total Return: ~84%

- Annualized IRR: ~16.5% / year

See analysts’ growth forecasts and price targets for SanDisk stock (It’s free!) >>>

TIKR’s mid-case model targets around $2,970, implying a total return of roughly 84% and an annualized return of around 16.5% per year over the forecast horizon. The mid case sits comfortably above the current Street mean of about $1,980, which tells you the model agrees with the direction of the analyst upgrades rather than the tape.

Two revenue drivers carry the forecast. The first is data center enterprise SSD demand, where AI inference workloads are pulling in high-capacity storage, and the Stargate line is just beginning to contribute. The second is the multi-year New Business Model contracts, which convert volatile spot volume into committed bits at floor-protected pricing. The margin driver is that same mix shift toward data center, which is structurally higher-margin than commodity consumer flash, supporting a mid-case net income margin near 58%. The primary risk is unchanged from the bear case: with the majority of bits still exposed to spot pricing, a NAND downcycle would pressure margins fast.

The upside is that AI storage demand and contract coverage keep pricing firm through 2027, and the earnings the current multiple sits on prove durable. The downside is that Samsung and SK Hynix capacity floods the market, spot NAND pricing rolls over, and the stock re-rates as investors decide it is still the old cyclical SanDisk.

Conclusion

The referee arrives in August, when SanDisk reports fiscal Q4 2026. The number that settles the analyst-versus-market fight is not headline revenue. It is a committed supply. Management said it expects to sign more New Business Model agreements, and Goldman’s own catalyst list flags contract scope as the swing factor. Watch the share of fiscal 2027 bits under multi-year deals. If it pushes meaningfully above the current level of roughly a third, the “cycle is different” case gains real evidence, and the target hikes look prescient. If it stalls near a third while NAND spot pricing softens, the market’s caution was the right read. Margin durability is the tell: holding LTM gross margin near the current 56.0% while new industry capacity comes online would be the strongest rebuttal the bears could get.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in SanDisk?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up SanDisk, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track SanDisk alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze SanDisk on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!