Key Stats for Amazon Stock

- Current Price: $245.98

- Target Price (Mid): ~$625

- Street Target: ~$313

- Potential Total Return: ~155%

- Annualized IRR: ~23% / year

- Earnings Reaction: +0.77% (April 29, 2026)

- Max Drawdown: 21.74% (February 13, 2026)

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Amazon (AMZN) just did something it has rarely needed to do: it borrowed heavily to pay for growth. On July 7, 2026, the company launched a bond sale of at least $25 billion to fund its artificial intelligence buildout, and the market’s response carried a note of caution that was absent from earlier deals this year. Bulls see a company pressing its advantage in the biggest technology shift in a generation. Bears see the most cash-rich company in tech reaching for debt because its own cash flow can no longer cover the bill.

That tension is the whole story right now. Amazon’s cloud business is accelerating, yet its free cash flow is heading into negative territory in 2026. The question the market cannot yet answer is simple: is this spending a monetization machine that will look cheap in hindsight, or a hole that keeps getting deeper?

Why the Bond Sale Matters

The deal itself was large and structured across eight tranches, with maturities running from three to 40 years, led by Barclays, Goldman Sachs, JPMorgan, and Morgan Stanley. Amazon earmarked the proceeds for general corporate purposes, which a spokesperson said can stretch to cover future capital spending or paying down existing debt, but the timing leaves little doubt about the driver. It follows roughly $54 billion Amazon already raised in bonds earlier this year, plus a $10 billion raise in Canada in June. The company told underwriters it does not plan to issue more debt in 2026.

The more revealing detail was demand. According to Bloomberg, which first reported the deal’s size, orders peaked near $62 billion before the banks trimmed the spread, paring the book to about $41 billion, or roughly 1.6 times the deal size. That is still oversubscribed, but it is a cooler reception than the March offering that drew so much interest it was heavily oversubscribed at $37 billion. When even Amazon’s debt starts to see thinner enthusiasm, it signals that investors are beginning to price the AI buildout more carefully.

The reason Amazon needs the cash is no secret. Management has guided to roughly $200 billion in capital expenditure for 2026, up sharply from the $131 billion it spent in 2025. Most of that goes to data centers, chips, and cloud infrastructure. And here is the part that separates Amazon from its peers. As Needham analyst Laura Martin has argued, every other major hyperscaler is funding its 2026 buildout largely from free cash flow, while Amazon is leaning on debt to close the gap.

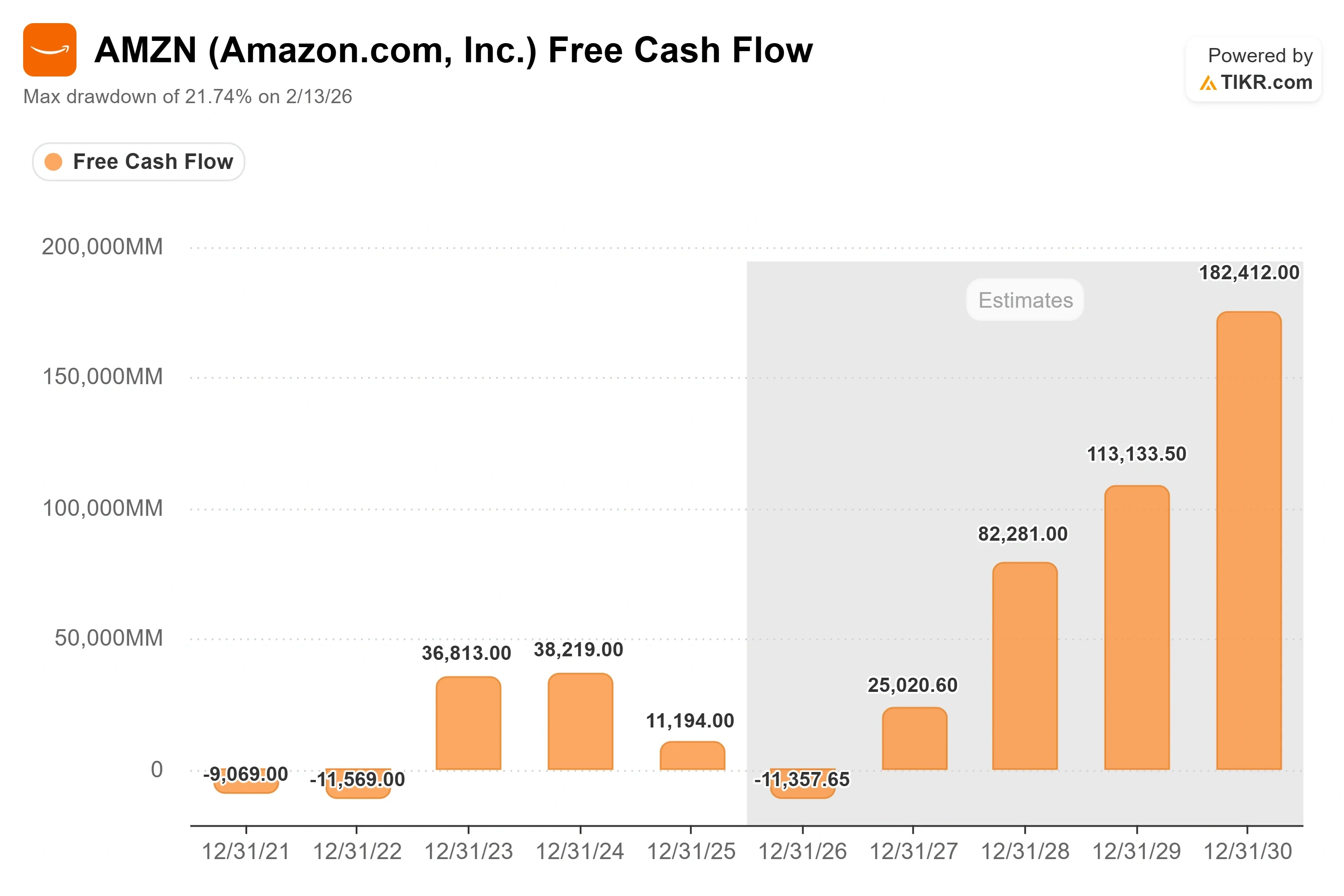

What the Cash Flow Actually Shows

The strain is visible in the model. Amazon generated $139.5 billion in operating cash flow in 2025, but free cash flow fell from $38.2 billion in 2024 to $11.2 billion in 2025 as capex surged. TIKR estimates free cash flow turns negative in 2026 as the spending peaks. That is the number bears keep circling, because a company cannot fund a $200 billion investment program from a negative cash flow line. The debt is the bridge.

CEO Andy Jassy has framed this deliberately as a timing feature, not a flaw. On the Q1 2026 earnings call, he explained the mechanics directly:

“AWS has to lay out cash for land, power, buildings, chips, servers and networking gear in advance of when we can monetize it, typically 6 to 24 months before we start billing customers depending on the component.”

That matters because it reframes the negative free cash flow as the front end of a cycle rather than a permanent condition. Jassy added that these assets carry long useful lives, more than 30 years for data centers and five to six years for chips, and that the returns become “cumulatively quite attractive a couple of years after being in service.” The bull case rests entirely on whether that timeline holds.

See historical and forward estimates for Amazon stock (It’s free!) >>>

The Growth That Justifies the Spending

The reason investors give Amazon the benefit of the doubt is the demand behind the buildout. In Q1 2026, AWS revenue reached $37.6 billion, up 28% year-over-year, the fastest growth in 15 quarters, at a segment operating margin near 38%. Jassy told analysts the AWS backlog stood at $364 billion at quarter-end, and that figure excluded the recently announced Anthropic deal worth over $100 billion.

The custom silicon story is the sharper edge. Amazon’s chip business is now growing triple digits year-over-year, and Jassy said Trainium revenue commitments exceed $225 billion. Trainium is Amazon’s in-house AI training chip, and its economics are the point: Jassy said it delivers about 30% better price performance than comparable GPUs, and that at scale it will “save us tens of billions of dollars of CapEx each year and provide several hundred basis points of operating margin advantage versus relying on others’ chips for inference.” If that holds, the capex bill is partly self-funding through the savings it generates.

The whole company grew revenue 17% to $181.5 billion in Q1, with operating income of $23.9 billion and a 13.1% operating margin, the highest in Amazon’s history. Advertising added $17.2 billion, up 22%. The stock barely moved on the print, closing up 0.77%, because the market had already rallied into the quarter and had moved on to the harder question about cash.

Where the Valuation Sits

At $245.98, Amazon trades at around 12x NTM EV/EBITDA, a measure of value against expected operating profit. That sits below the roughly 13x to 14x range the stock held across 2025, meaning the market is paying less for each dollar of forward earnings power than it did a year ago, even as growth accelerated. The stock is off about 12% from its $278.56 all-time high set in May 2026, though it has recovered off its 52-week low near $196.

On July 1, Goldman Sachs urged investors to buy several U.S. hyperscalers, including Amazon, ahead of earnings, arguing their valuations had dropped even as earnings kept growing. That is the compression bulls point to. The risk runs the other way: if AI demand monetizes slower than management assumes, the capex weighs on free cash flow for longer, and the multiple never re-rates. Ongoing regulatory scrutiny of large technology firms, which Morningstar flags as a rising concern as Amazon expands internationally, adds an overhang that the buildout thesis has to absorb.

See how Amazon performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $245.98

- Target Price (Mid): ~$625

- Potential Total Return: ~155%

- Annualized IRR: ~23% / year

See analysts’ growth forecasts and price targets for Amazon stock (It’s free!) >>>

The mid case fits this stock because it sits between a Street that already expects upside and assumptions that do not require heroics. It puts AMZN around $625 by year-end 2030, an implied total return near 155% and an annualized IRR (the yearly return from today’s price to the target) of about 23%.

Two revenue drivers carry the model. The first is AWS, growing on a $150 billion-plus annualized run rate with a $364 billion backlog behind it. The second is advertising, scaling past $17 billion a quarter at margins that lift the whole company. The margin driver is mixed: as higher-margin cloud and ads grow faster than low-margin retail, the model assumes net income margin expands toward roughly 16% from the current level near 9%.

The primary risk is the cash flow trough. The upside is that Amazon’s spending converts to billable capacity faster than the market expects, and the multiple re-rates as free cash flow recovers. The downside is that monetization lags, the capex keeps outrunning revenue, and the stock stays stuck paying for a buildout it cannot yet show returns on.

Conclusion

The next hard evidence comes on July 30, 2026, when Amazon reports Q2 earnings. Watch two lines. First, AWS growth: holding at or above the 28% it posted in Q1 would confirm demand is still accelerating into the buildout, while a slip below 25% would hand the bears their opening. Second, the free cash flow trajectory. Management has set no floor, so the first sign that trailing free cash flow has stopped shrinking is the clearest proof that the spending is turning into returns. Until one of those two things breaks in Amazon’s favor, the $25 billion in fresh debt is a wager on Jassy’s monetization timeline against the market’s patience. July 30 is when that wager starts getting settled.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Amazon?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Amazon, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Amazon alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!