Key Stats for Cognizant Stock

- Current Price: $52.10

- Target Price (Mid): ~$75

- Street Target: ~$73

- Potential Total Return: ~45%

- Annualized IRR: ~8% / year

- Earnings Reaction: (3.29%) on 4/29/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Cognizant Technology Solutions (CTSH) has shed nearly 40% from its year-start price of $83.00, hitting a max drawdown of 46.98% on May 13, 2026. On May 18, the board made two moves at once: it added $2 billion to the overall share repurchase authorization, bringing the remaining authorized capacity to approximately $3.45 billion, and raised the 2026 buyback target by $1 billion, from $1 billion to $2 billion for the year. The additional $1 billion is expected to be repurchased within Q2. CEO Ravi Kumar S stated in the announcement that the company believes its “current share price significantly undervalues those prospects.”

The same day, Kumar appeared at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference, where he laid out why the selloff misreads what AI actually does to his business.

The Market Is Solving for the Wrong Problem

The fear is straightforward: if AI writes code and automates processes, why does any enterprise need 357,600 consultants? It is a legitimate question, but it is the wrong one for Cognizant specifically.

Kumar’s framing at J.P. Morgan cuts to the point. “The AI capability is absolutely moving at a rapid pace,” he told analyst Tien-Tsin Huang. “The bridge to production value has a big gap. The more the capability is, the more the production value gap is.” AI doesn’t replace his business. It creates a new category of work that didn’t exist before.

He acknowledged the deflationary pressure directly: “Software engineering is deflationary.” But software engineering is only part of Cognizant’s revenue. The larger opportunity is applying AI to the operations of companies, a domain that classical software has never reached because the work required human judgment.

His healthcare example is concrete. Cognizant’s TriZetto platform, a healthcare claims and administration software suite, processes $500 billion of healthcare spend annually. Of the roughly 20 million people employed in U.S. healthcare, Kumar estimates only 5 to 6 million perform actual care. The remaining 14 to 15 million do administrative work. “I could agentify it,” he said. “It is self-funded. You just have to front-load it, you have to transition human labor to digital labor.” A platform embedded at that scale is not being disrupted. It is positioned at the entry point of a new market.

See historical and forward estimates for Cognizant stock (It’s free!) >>>

What Kumar Said at J.P. Morgan That Investors Need to Hear

The most pointed question Kumar faced: do OpenAI’s and Anthropic’s moves into enterprise deployment threaten IT services firms like Cognizant? His answer was a direct dismissal.

“On the contrary, it reinforces the fact that there is a gap between production value and the capability of those models,” Kumar said. “I don’t think those deployment companies have been built for scale. I don’t think it is built to monetize the bridge.”

He pointed to active work already underway: a large mainframe modernization engagement running Anthropic’s Claude on AWS cloud, 5 to 6 active SAP migration engagements, and 10 to 12 vulnerability discovery projects using AI tooling.

Beyond the deal activity, Kumar laid out a pricing concept that current analyst forecasts don’t yet capture: tokenization as a moat. As clients shift toward AI-augmented outcomes, the unit of value becomes the token, the computational unit AI models consume per task. Cognizant is building a pricing harness across hundreds of engagements, accumulating enough community data to price tokenized work more precisely than any single client can. “Clients said, ‘My bills are going up. Would you be able to take this over?'” Kumar said. Whether this becomes a durable economic moat is unproven, but it is a dynamic current that Street models don’t capture.

The Financials Behind the Conviction

The selloff has masked a business that has been quietly improving. Q1 2026 revenue came in at $5.413 billion, up 5.8% year-over-year, landing in the upper half of guidance. Adjusted EPS hit $1.40, up 13.8%, beating the Street by 4.98% per TIKR Beats & Misses data. Trailing twelve-month bookings reached $29.6 billion, up 11%, with seven large deals, including one mega deal exceeding $500 million in total contract value.

April 29 also brought Project Leap, a restructuring targeting $200 to $300 million in in-year savings. The program carries $230 to $320 million in charges mostly in 2026, but it raised full-year adjusted operating margin guidance to 16.0% to 16.2%. The stock still fell 3.29% on earnings day, primarily on the softer Q2 revenue guide.

FY2025 free cash flow came in at $2.665 billion, a 12.6% FCF margin, and the balance sheet carries $425 million in net cash. Management is directing that capital into buybacks at prices it has explicitly called undervalued.

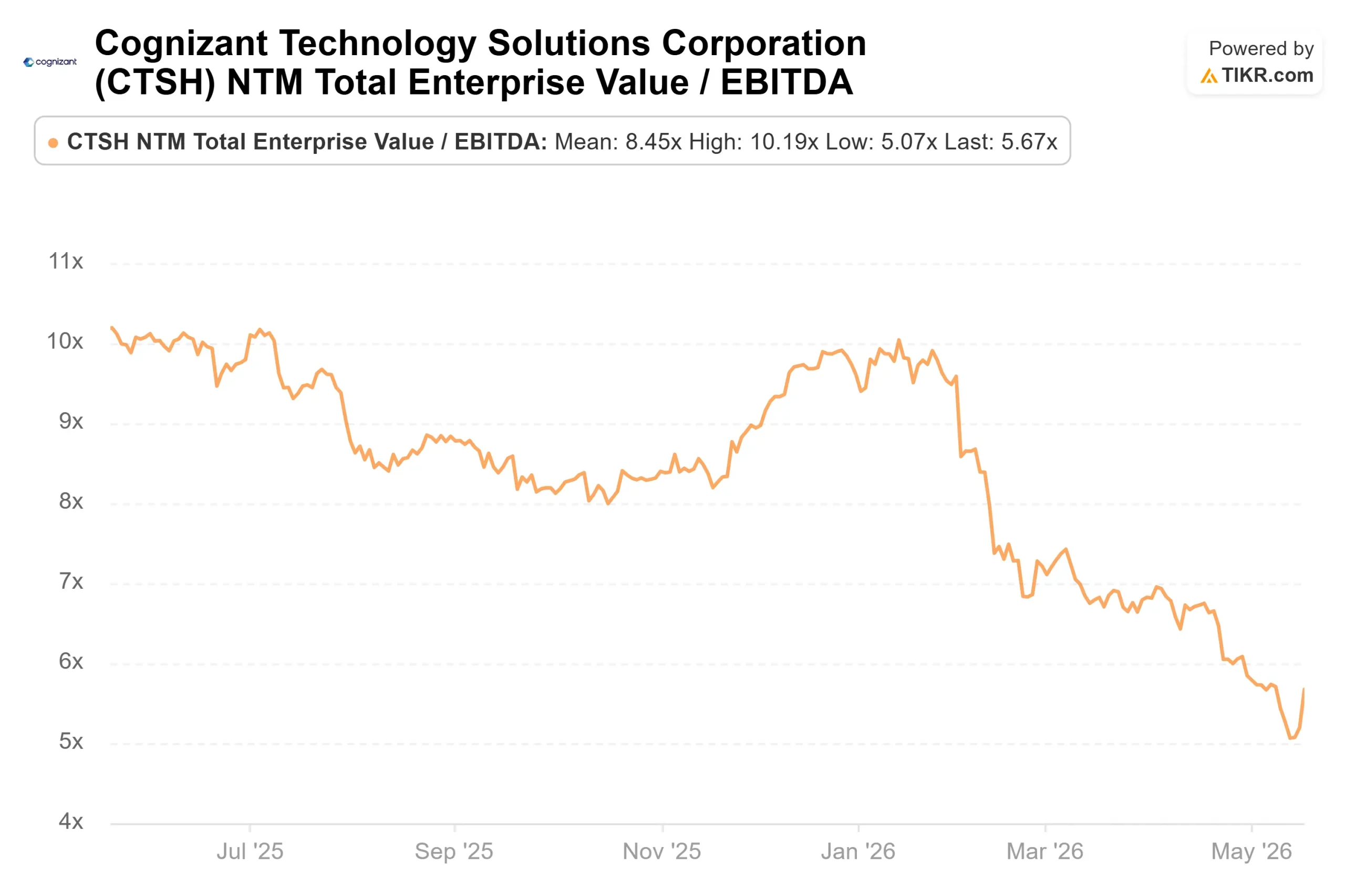

The valuation multiples reinforce the disconnect. CTSH trades at 5.67x NTM EV/EBITDA, a steep discount to Accenture at 7.49x, Infosys at 9.46x, Wipro at 8.43x, and Tata Consultancy Services at 10.16x, against a peer average of around 8.6x. Cognizant’s Financial Services segment grew 10% in constant currency in Q1 2026, and its BPO unit has posted double-digit growth for two consecutive years. A business growing its best segments faster than peers and trading at the widest peer-group discount presents a gap that is hard to explain on fundamentals alone.

See how Cognizant performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $52.10

- Target Price (Mid): ~$75

- Potential Total Return: ~45%

- Annualized IRR: ~8% / year

See analysts’ growth forecasts and price targets for Cognizant stock (It’s free!) >>>

The mid case requires no upside from the tokenization moat or agentic BPO opportunity Kumar outlined at J.P. Morgan. It is a continuation of what the business is already doing.

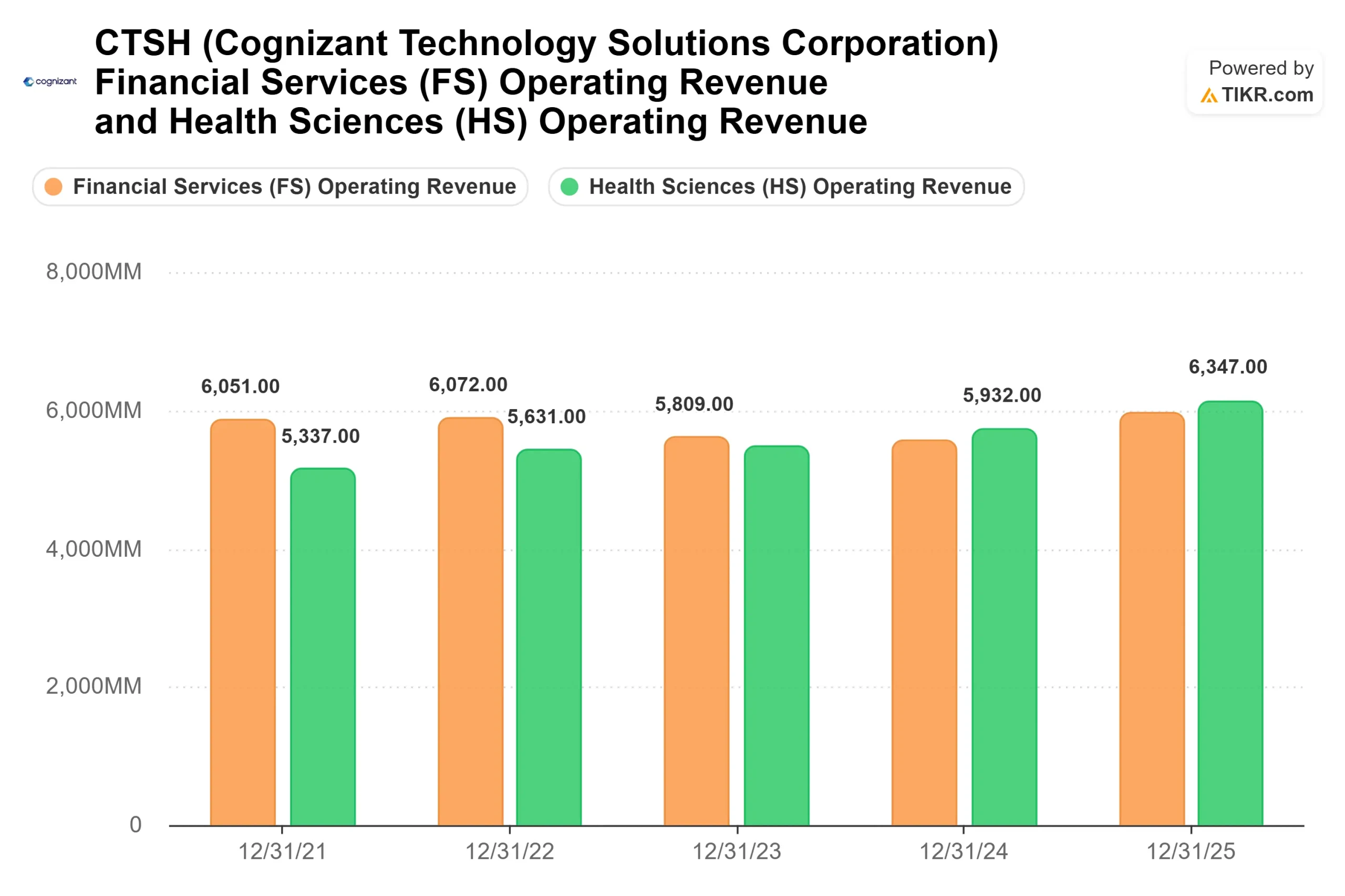

The two revenue drivers are Financial Services, which grew 10% in constant currency in Q1 2026 and contributed $6.17 billion to FY2025 revenue, and Health Sciences, underpinned by the TriZetto platform’s $500 billion processing base. Together, they made up $12.52 billion of Cognizant’s $21.1 billion in FY2025 revenue. The margin driver is Project Leap savings combined with the shift to fixed-price contracts, now at roughly 50% of revenue, up from around 40% three years ago. Fixed-price deals, where Cognizant owns delivery risk and captures the AI productivity gain directly, structurally expand profit margins as AI lowers delivery costs. The consensus net income margin forecast of around 12% reflects this conservatively.

The primary risk is constant-currency revenue growth stalling below the guided floor, particularly if the CMT segment (Communications, Media, and Technology), the weakest unit for three years, sees further discretionary spend cuts. If that happens, the inflection point Kumar described slips from 2026 into 2027. Even so, the low-case TIKR scenario points to around $73, still above the current price. A business carrying $425 million in net cash with management actively repurchasing stock at these levels does not need the bull case to find fair value above $52.

Conclusion

The number to watch is Q2 2026 constant-currency revenue growth, guided to 3.2% to 4.7%, which reports on July 29, 2026. A print at or above the midpoint confirms the large-deal bookings cycle is converting on schedule, and the selloff was a sentiment-driven overshoot. A miss below the low end turns the discretionary spending concern into a structural story and pushes Kumar’s inflection point to 2027.

Management has put $2 billion of shareholder capital behind the view that the current price is wrong. July 29 is when investors find out who is right.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Cognizant?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Cognizant, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Cognizant alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Cognizant on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!