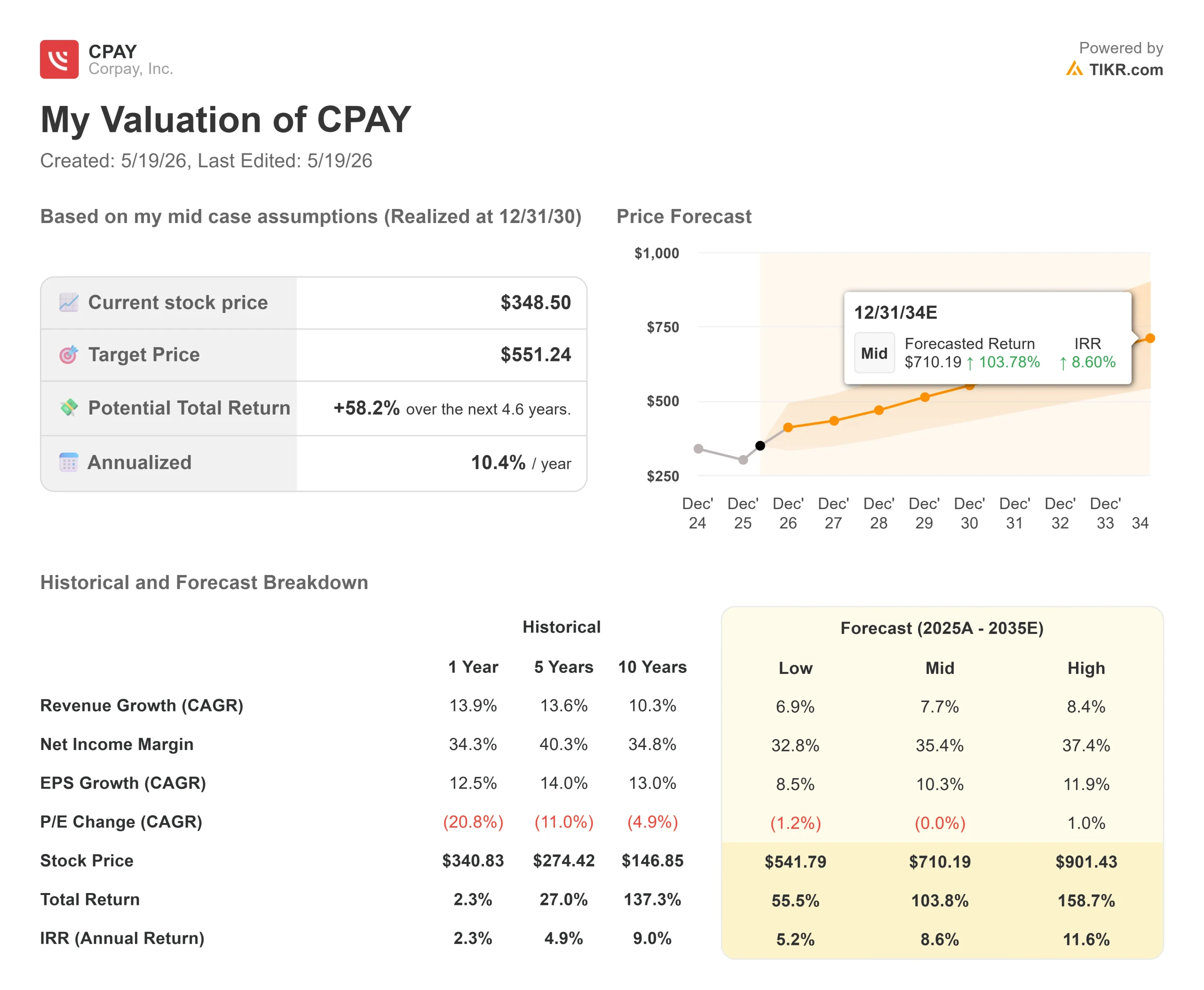

Key Stats for Corpay Stock

- Current Price: $349.54

- Target Price (Mid): ~$550

- Street Consensus Target: ~$390

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

- Earnings Reaction: +12.51% (May 7, 2026)

- Max Drawdown: 27.27% on 10/30/25

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Corpay, Inc. (CPAY) has had one of the most eventful two weeks in its recent history, yet the stock sits nearly 4% below its 52-week high of $361.99. That gap is the story.

In ten days, the company reported a blowout quarter, added blockchain settlement through JPMorgan and BVNK, hosted a cross-border investor teach-in, and sent CFO Peter Walker onto the stage at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference. The stock surged 12.51% on earnings day. Then it stalled as the stablecoin overhang reasserted itself.

The tension is clear. Bulls see a company compounding at double digits with adjusted EBITDA margins that JPMorgan analyst Tien-Tsin Huang described as the third-highest in his payments coverage universe, behind only Visa and Mastercard. Bears see a cross-border business they believe is exposed to stablecoin disruption. Walker spent May 18 at JPMorgan making the case that the bears are misreading the business.

A Quarter That Left Little Room to Argue

Per Corpay’s investor relations materials, Q1 2026 revenue came in at $1,260.99 million, up 25% year-over-year and ahead of the $1,212.28 million consensus. Adjusted EPS hit $5.80 against an estimate of $5.47. The 12.51% single-day move on May 7 was the market’s verdict.

What stood out was the consistency behind the beat. Organic revenue grew 11% for the fourth consecutive quarter. Revenue retention held at 93.5%. New sales bookings rose 24% year-over-year. Corporate Payments, the segment Corpay is pivoting its entire business toward, reached 40% of total company revenue in the quarter for the first time, according to Corpay’s Q1 2026 earnings release. Management raised full-year 2026 guidance to a revenue midpoint of $5.29 billion and adjusted EPS midpoint of $26.70.

Walker was direct at JPMorgan. “We actually came out of the gate stronger than we expected,” he said. “Two-thirds really came from business fundamentals,” with the remainder reflecting a weaker U.S. dollar and higher fuel prices.

See historical and forward estimates for Corpay stock (It’s free!) >>>

What the CFO Said About Stablecoins

The stablecoin question has been the single biggest overhang on CPAY. The fear: if stablecoins commoditize cross-border money movement, Corpay’s fastest-growing segment loses its edge.

Walker’s answer at JPMorgan was the clearest the company has given publicly. First: over 85% of Corpay’s cross-border revenue runs through G20 currencies, markets that are already highly liquid and nearly instant. There is no margin to disrupt in the rail because the rail already moves efficiently. The value Corpay delivers sits in the services wrapped around the transaction.

Second: running what Corpay believes is the largest cross-border operation outside the banking system requires capabilities no stablecoin replaces. A customer acquisition engine, liquidity across 145 currencies, the ability to net over 60% of trades internally, and a licensing framework built over 20 years. “The idea of somebody catching up to us at the rate we’re growing, I think that’s going to be difficult,” Walker said.

Third, and most counterintuitively: Corpay partnered with JPMorgan’s Kinexys blockchain and BVNK’s stablecoin infrastructure in early May 2026, adding 24/7 settlement as a product feature. Rather than defending against disruption, management is absorbing it as a distribution advantage. Walker’s view is that tokenized bank currency (Kinexys) will win over public stablecoins for corporate clients because it avoids the on-chain/off-chain friction that limits adoption in treasury workflows.

If stablecoins are additive to Corpay’s platform rather than corrosive to its margins, the discount the market has applied to the cross-border business looks mispriced.

The Cross-Border Growth Engine

Walker described the cross-border mechanics more granularly than most CFO presentations allow. The segment competes against Tier 2 through Tier 4 regional banks, not other fintechs. Management estimates the addressable market at approximately $160 billion in that bank segment, and Corpay holds less than 1% of it today.

The product logic is tight. A middle-market company expanding internationally needs to pay overseas vendors, manage FX risk, and open foreign bank accounts. Tier 2 to 4 banks take four to six months to open a foreign account. Corpay does it in roughly a week. That speed pulls clients in, and once inside, wallet share grows because international payments and FX risk management go together. The 97% retention rate in cross-border reflects how sticky that combination becomes.

The Alpha Group acquisition, which closed in late 2025, expanded licensing into the U.K. and continental Europe. Walker confirmed at the conference that 15% of Alpha’s client volume has already migrated to Corpay’s global platform, with the rest expected by mid-summer 2026. Alpha synergies are back-half weighted for 2026, with a larger contribution expected in 2027.

One channel deserves specific attention. Corpay’s Mastercard partnership allows it to white-label cross-border capabilities directly into Tier 2 through 4 banks, creating a distribution layer where Corpay sells to the very banks it competes against.

Capital Allocation: Cash Generation and What Management Plans to Do With It

TIKR consensus estimates show Corpay generating around $1.55 billion in free cash flow in 2026, rising to around $1.96 billion in 2027. Walker told JPMorgan that management is targeting approximately $2 billion in free cash flow for 2026, which he framed as giving the company significant optionality. Over the past eight years, Corpay has deployed $15.5 billion in capital, split roughly 50-50 between buybacks and M&A.

Walker confirmed Corpay just refinanced all of its outstanding debt, upsizing its credit facility by over $1 billion, extending maturities by five years, and reducing the interest rate by 10 basis points. He described the terms as a direct reflection of the company’s free cash flow profile and growth trajectory in the credit markets.

The buyback conviction signals what management actually thinks the stock is worth. Trading at roughly 13 times the $26.70 midpoint of management’s 2026 adjusted EPS guidance, Walker’s comment that CPAY is “truly undervalued given the results that we produce” was a direct answer to a question about stablecoin risk. It was not a prepared line.

On M&A, the Corporate Payments pipeline is active, and Walker confirmed additional Vehicle Payments divestitures are being evaluated for assets that are profitable but too TAM-constrained to grow at Corpay’s current scale.

See how Corpay performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $349.54

- Target Price (Mid): ~$550

- Potential Total Return: ~58%

- Annualized IRR: ~10% / year

See analysts’ growth forecasts and price targets for Corpay stock (It’s free!) >>>

The TIKR mid-case model targets approximately $550 by 12/31/30, a total return of around 58% from $349.54, annualizing at roughly 10% per year. The model assumes a mid-case revenue CAGR of around 8%, consistent with TIKR consensus estimates showing revenue growing from $4.53 billion in 2025 to around $7.62 billion by 2030. The two primary drivers are the rotation into Corporate Payments, where segment margins are structurally higher, and the scaling of cross-border as Alpha integration completes.

The margin driver is EBITDA expansion. LTM EBITDA margin sits at around 53% per TIKR data, temporarily compressed by Alpha running at pre-synergy cost levels. Walker guided explicitly toward margin recovery in 2027.

The Street is less patient. TIKR’s Street Targets screen shows a mean analyst price target of $389.79 across 14 estimates (5 Buys, 4 Outperforms, 3 Holds), implying around 12% upside on a 12-month basis. The primary risk Walker named is stablecoin disruption accelerating beyond G20 currency corridors, where it poses no current threat. At 13 times 2026 adjusted EPS, sentiment re-rating slower than earnings growth is the more immediate risk.

Conclusion

The next meaningful test is Q2 2026 earnings, where management has guided for revenue of approximately $1.295 billion and adjusted EPS of $6.55, representing 28% year-over-year earnings growth. Watch Corporate Payments’ organic growth specifically. If it holds double digits in Q2, the stablecoin discount has no new data to stand on. If it misses, the bear case gets its first real evidence.

Walker said at JPMorgan that Alpha synergies will show up meaningfully in the back half of 2026. Q2 is the data point that either confirms or defers that. The difference between those two outcomes is the difference between CPAY re-rating toward the Street’s ~$390 consensus target or drifting back toward $310.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Corpay?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Corpay, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Corpay alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!