Key Stats for Caterpillar Stock

- Current Price: $863.95

- Target Price (Mid): ~$1,120

- Potential Total Return: ~30%

- Annualized IRR: ~6% per year

- Earnings Reaction (4/30/26): (0.05%)

- Street Target (Mean): $913.29

- Max Drawdown: 13.88% on 3/30/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Caterpillar Inc. (CAT) has risen more than 150% from its 52-week low of $336.24 as the market reprices the company from a cyclical equipment maker into a power infrastructure play. Today, at a Bank of America virtual investor meeting, Power & Energy Group President Jason Kaiser spent an hour explaining what is actually driving that story. His answers go well beyond what any earnings transcript has covered.

The most recent catalyst was Q1 2026 earnings on April 30, when CAT reported revenue of $17.415 billion, up 22% year-over-year, and adjusted EPS of $5.54, a 19.3% beat versus the consensus estimate of $4.64. Power & Energy drove the quarter with $7.03 billion in segment revenue. On the earnings call, CEO Joe Creed reported that total enterprise backlog reached a record $63 billion, up 79% year-over-year, with all three primary segments contributing. Management also raised its long-term revenue compound annual growth rate target to 6% to 9% through 2030.

The core question BofA analyst Michael Feniger put to Kaiser is whether this momentum is structural or a pull-forward. Here is what Kaiser’s answers actually revealed.

See historical and forward estimates for Caterpillar stock (It’s free!) >>>

What “Bring Your Own Power” Actually Means

The original data center power story was simple: hyperscalers needed diesel standby generators as a backup when the grid went down. That business was growing, but it was a reliable product, not a primary energy source.

Over the past 18 months, something structurally different has emerged. Data center developers are no longer waiting for utility grid connections. They are building campuses before grid access is secured and powering them with CAT engines and Solar Turbines gas turbines from day one. Kaiser described the full spectrum: some customers need a short bridge of months until a utility connection arrives, some need a multi-year solution, and some have decided to run on-site generation permanently because the reliability and economics beat the grid.

“We see quite a few customers that are setting up for the long term,” Kaiser said. “They see the efficiency, the performance, the systems we’re able to deliver as being real positive as compared to the utility, and they’re going to keep it there for the long term.”

A backup genset sits largely idle, running only when the grid fails. A prime power genset runs continuously for decades. The difference in parts consumption, service frequency, and aftermarket revenue is what makes this shift so consequential.

The Number That Changes the Services Story

Kaiser disclosed a figure that has not appeared in any earnings call. When comparing a diesel standby generator to a gas generator running as primary power, the lifetime services opportunity for the gas unit is 40 times larger.

“If you compare a standby diesel genset and you look at the lifetime services opportunity and compare that to a gas genset that’s running primary power 24/7, there’s 40x more services opportunity over the lifetime for that gas genset,” Kaiser said.

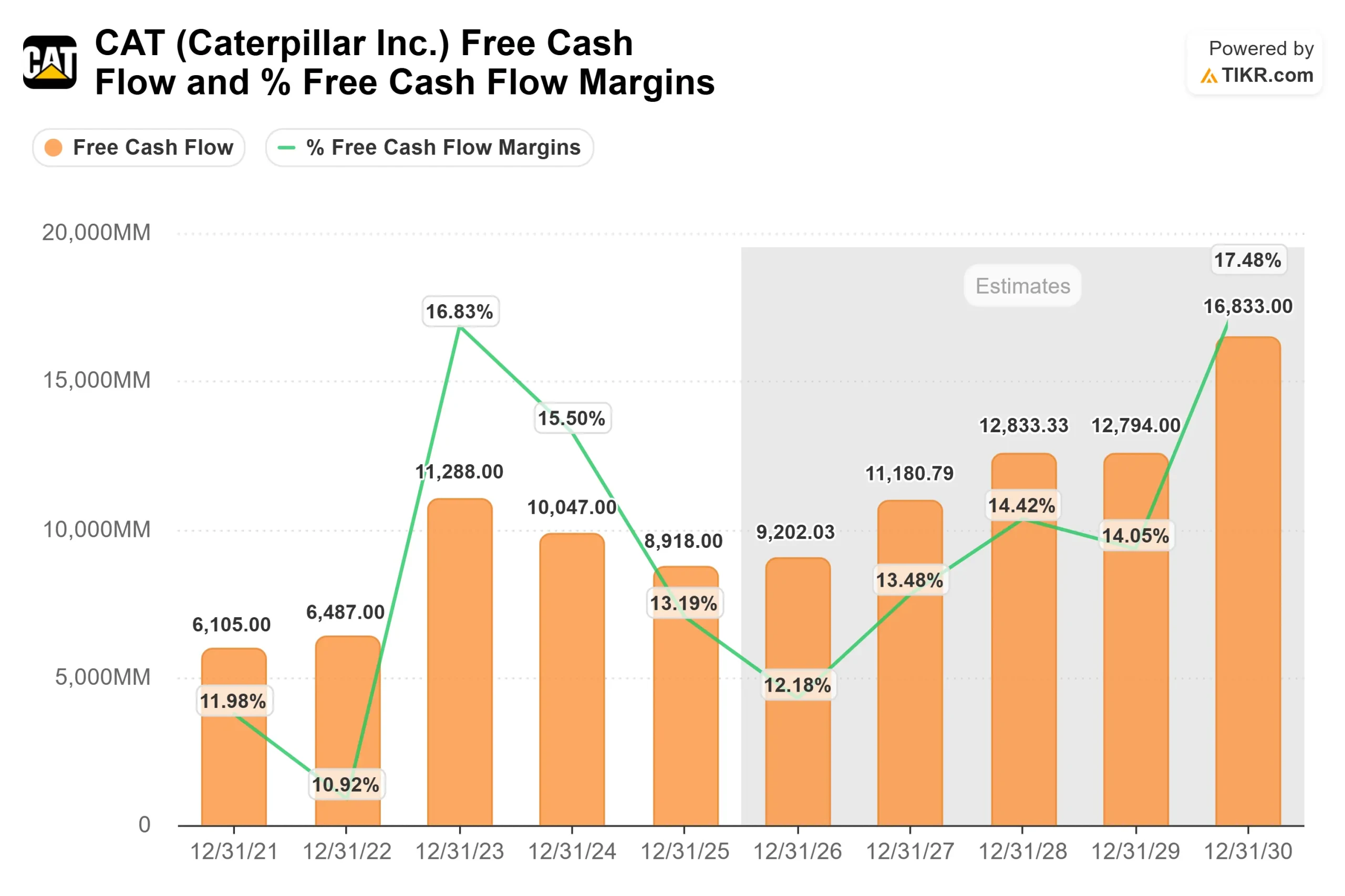

The logic is mechanical. A standby diesel generator might run a few hundred hours per year. A prime power gas generator runs continuously, requiring scheduled maintenance, periodic top-end overhauls, and full rebuilds over a product life spanning multiple decades. Each of those events generates parts revenue, labor revenue, and revenue from long-term service agreements sold alongside the original equipment. TIKR consensus estimates project CAT’s free cash flow growing from $8.9 billion in FY2025 to around $16.8 billion by 2030, and the shift from standby to prime power is a key driver of that trajectory.

This also explains how Power & Energy margin expansion can coexist with tariff headwinds. Services carry better margins than new equipment, and the installed base is only beginning its shift toward prime power.

How CAT Is Managing Overcapacity Risk

Caterpillar is expanding large reciprocating engine capacity to nearly three times its 2024 levels, with turbines going to 2.5x. The obvious risk is overcapacity if the data center buildout slows. Kaiser gave three specific answers.

First, major customer agreements include cancellation penalties and sometimes upfront prepayments before CAT commits additional capital. The six publicly announced contracts covering at least one gigawatt each, including the ProPower deal for 2.1 gigawatts over five years disclosed at Q1 2026 earnings, are only part of the picture. “We have several other smaller ones that we haven’t announced as well,” Kaiser said.

Second, the same large engine platform powering a data center also powers gas compression in midstream pipelines and mining trucks in Resource Industries. If data center demand softens, CAT can redirect capacity to those end markets.

Third, Caterpillar ran an internal stress test on its own AI and technology roadmap, modeled its own future data consumption, and concluded the demand signal was large enough to justify the capacity investment. “Whether that would support the kinds of investments that others are seeing and backstop the investments we’re making, and we see it,” Kaiser said.

Oil & Gas: The Underappreciated Growth Driver

Power generation gets the headlines, but Kaiser noted that the oil and gas vertical inside Power & Energy is at record revenue levels even as traditional upstream indicators like rig counts remain soft. The driver is gas compression, not drilling.

As more electricity is generated with natural gas and LNG export volumes rise, the pipeline infrastructure moving gas from wellheads to power plants and export terminals requires continuous compression from CAT engines and Solar Turbines gas turbines. Kaiser said oil and gas sales to users grew 16% in Q1 2026, driven primarily by gas compression. He expects that to continue as LNG infrastructure investment grows. The Middle East conflict introduces some near-term uncertainty, Kaiser acknowledged directly, but the longer-term signal from that region points toward more energy security investment, not less.

The Vertiv Partnership

In November 2025, Caterpillar and Vertiv announced a strategic collaboration combining CAT and Solar Turbines’ power generation with Vertiv’s cooling and power distribution hardware into pre-designed reference architectures for AI data centers.

Kaiser was direct about the strategic logic: speed to power is the primary purchase criterion he consistently hears from customers. Pre-integrating CAT’s generation with Vertiv’s cooling systems cuts the engineering handoffs that currently slow deployment. The result is an integrated systems offering that is harder for customers to disaggregate and harder for competitors to displace with a lower-priced alternative.

See how Caterpillar performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $863.95

- Target Price (Mid): ~$1,120

- Potential Total Return: ~30%

- Annualized IRR: ~6% per year

See analysts’ growth forecasts and price targets for Caterpillar stock (It’s free!) >>>

The TIKR mid-case assumes around 6.5% revenue CAGR and a net income margin of approximately 18%, arriving at around $1,120 by 12/31/30, a ~30% total return, and roughly 6% annualized from today’s price.

The two revenue drivers are Power & Energy backlog conversion from data center prime power demand, and gas compression growth tied to LNG infrastructure. The margin driver is operating leverage as capacity scales and the services mix improves. The primary risk is valuation multiple compression. CAT trades at 25.99x NTM EV/EBITDA, well above the broad machinery peer median of approximately 8.86x per TIKR’s Competitors data. Among the most comparable names, Cummins (CMI) trades at 14.22x and Atlas Copco at 17.45x. Any evidence that prime power adoption is slowing would compress CAT’s multiple faster than earnings could offset.

The high case puts CAT at around $1,820, assuming the 40x aftermarket multiplier begins compounding through the P&L as the prime power installed base matures. The low case lands at around $1,150, still around 33% total return over the period, reflecting how much revenue visibility CAT has accumulated from its backlog.

Conclusion

The number to watch is not Power & Energy revenue growth, which is well understood. It is the segment’s operating margin. In Q1 2026, the segment delivered approximately 20.6% operating margin, down 170 basis points year-over-year as tariffs and manufacturing ramp costs hit simultaneously, per Kaiser’s comments at the conference. If segment margin returns above 22% by Q3 2026, it confirms that those headwinds are transitory and the services thesis is on track. If margins stay at 20% or below through Q3, the premium multiple starts to look fragile. Q2 2026 results, expected August 5, 2026, will be the first real test.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Caterpillar?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Caterpillar, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Caterpillar alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Caterpillar on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!