Key Stats for Western Digital Stock

- Current Price: $439.44

- Target Price (Mid): ~$800

- Street Target: ~$508

- Potential Total Return: ~74%

- Annualized IRR: ~14% / year

- Most Recent Earnings Reaction: (0.69%) on 4/30/26

- Max Drawdown: 20.59% on 3/30/26

Now Live: Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Western Digital Corporation (WDC) has spent the past year making a compelling case that the hard disk drive (HDD) business is not a dying industry, it is becoming indispensable to AI infrastructure. Shares climbed from a 52-week low of $49.00 to a high of $525.15, driven by an AI-fueled storage buildout that has consistently outrun Wall Street’s expectations. The stock has since pulled back to $439.44, and investors are asking whether the thesis is still intact.

On May 18, 2026, at the J.P. Morgan 54th Annual Global Technology, Media and Communications Conference, CFO Kris Sennesael delivered a demand upgrade that has not yet been fully absorbed by the market.

The Demand Outlook Keeps Getting Bigger

In February 2025, Western Digital told investors it expected global exabyte demand to grow at a mid-teens compound annual growth rate (CAGR) over the next three to five years. At the time, the company said AI could push that into the low 20s. At the JPMorgan conference, Sennesael upgraded the outlook again: Western Digital now expects exabyte growth above 25% CAGR over the next three to five years.

“Every time we talk to them, they come back with stronger and longer,” Sennesael said of the company’s hyperscaler customers, adding that the largest cloud operators are “willing to almost commit further out, 2031, 2032.” That kind of multi-year forward visibility is unusual for a hardware supplier.

Four demand layers are driving the acceleration. The baseline cloud layer consumer uploads, enterprise video, and business data remain strong. Enterprises are now storing all operational data they can capture rather than discarding it. AI training and retraining of large multimodal models continue to consume enormous storage. And most underestimated in the current consensus: inferencing. Sennesael estimated that roughly two-thirds of AI compute power in 2026 is being used for inference workloads, and the full output of every AI interaction from chatbots to agentic AI pipelines is being stored on HDDs. That is a category of demand that barely existed three years ago.

See historical and forward estimates for Western Digital stock (It’s free!) >>>

Scaling Exabytes Without Adding Factories

What makes the setup financially compelling is how WDC plans to deliver on the demand growth.

Sennesael was explicit: WDC does not need to add unit capacity to support above-25% exabyte CAGR. The average nearline drive today ships at 23 terabytes. Its 40-terabyte ePMR (Energy-Assisted Perpendicular Magnetic Recording, a technology that enhances the magnetic write process to enable higher capacity per drive) is in qualification with three customers and on track for volume production in the second half of calendar 2026. HAMR (Heat-Assisted Magnetic Recording, which uses a laser on each drive head to enable writing at higher densities) drives rated at 44 terabytes are in qualification with four customers and set for a volume ramp in 2027. Moving from a 23-terabyte average to 44 terabytes per unit means WDC can nearly double exabytes delivered without building new factories.

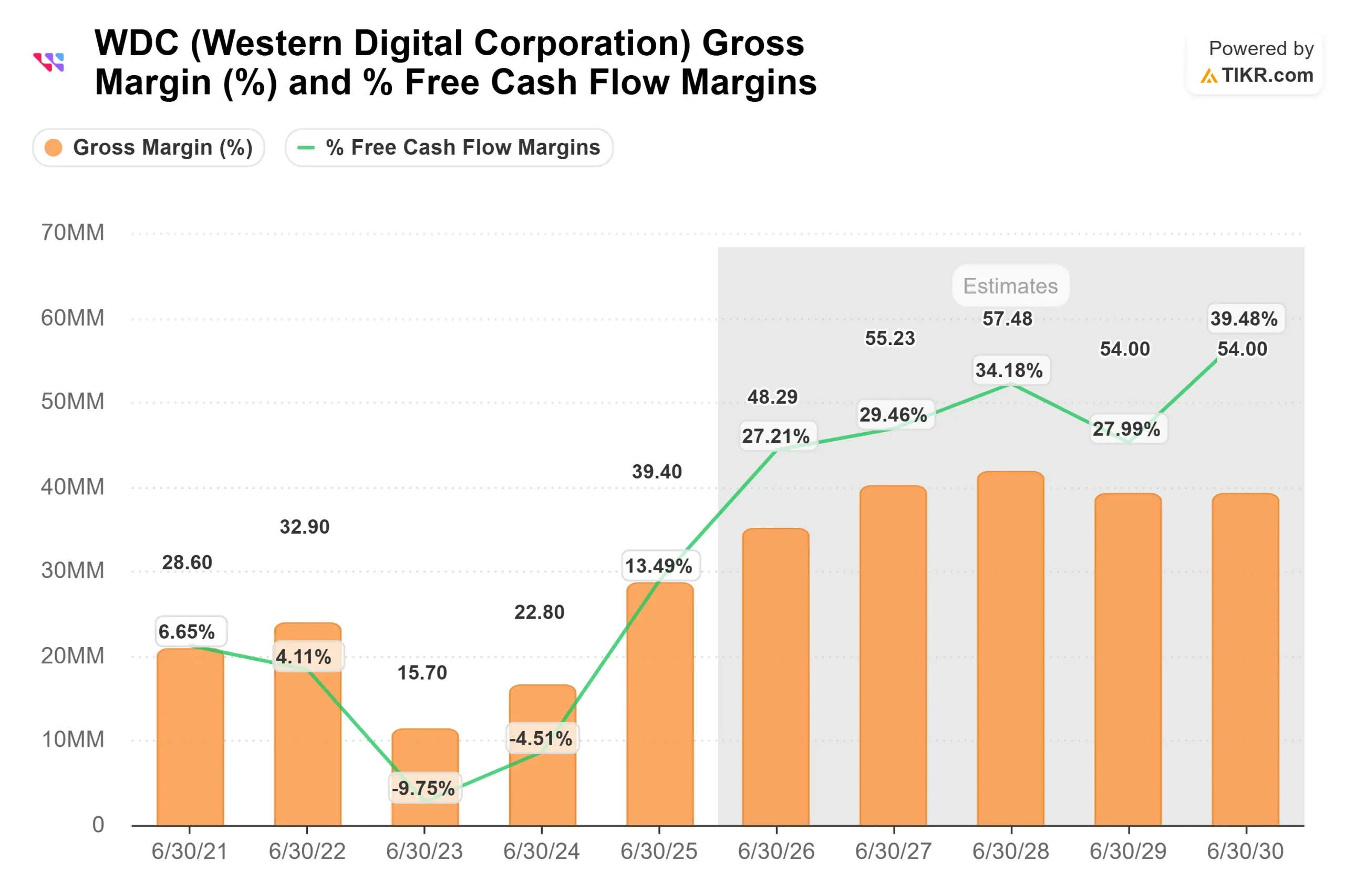

That dynamic flows directly into margins. Per TIKR consensus estimates, EBITDA margins are modeled to expand from around 40% in FY2026 to around 48% in FY2027 and above 52% in FY2028 because revenue scales far faster than the existing cost base. Sennesael confirmed this at the conference: “Revenue is going to grow a lot faster than our operating expense.”

An additional margin lever not fully priced into most models: UltraSMR (Ultra-Shingled Magnetic Recording, a firmware technique that overlaps data tracks to deliver roughly 20% more exabytes from the same hardware). Two of WDC’s largest hyperscalers are already running nearly all their exabyte demand on UltraSMR. Sennesael said WDC plans to convert nearly all major customers by the end of 2027, a free cash flow-accretive shift requiring no new capital spending.

WDC vs. Its Only Real Rival

The nearline HDD market is effectively a two-player industry. Western Digital and Seagate Technology Holdings (STX) together dominate the data center storage segment.

Both stocks have surged on the same AI tailwind, but their strategies differ. Seagate committed fully to HAMR earlier. WDC kept both ePMR and HAMR running in parallel. That parallel investment costs more in R&D, but it gave customers a proven option while HAMR builds its reliability track record in live fleets. The payoff: WDC’s gross margins ran ahead of Seagate’s during the ramp phase, even while spending more per platform.

Per TIKR, WDC currently trades at 19.89x NTM EV/EBITDA against Seagate’s 23.68x, a modest discount to its closest peer despite WDC’s margin advantage this cycle. The broader peer group median sits at around 11x NTM EV/EBITDA, reflecting how far above ordinary hardware cycles the market is pricing both companies.

See how Western Digital performs against its peers in TIKR (It’s free!) >>>

TIKR Advanced Model Analysis

- Current Price: $439.44

- Target Price (Mid): ~$800

- Potential Total Return: ~74%

- Annualized IRR: ~14% / year

See analysts’ growth forecasts and price targets for Western Digital stock (It’s free!) >>>

The TIKR mid-case model runs on two primary revenue CAGR drivers: nearline HDD exabyte volume growth from hyperscaler AI infrastructure spending, and per-terabyte pricing expansion as the product mix shifts toward higher-capacity 40TB ePMR and 44TB HAMR drives. The margin driver is operating leverage, revenue scaling well ahead of a largely fixed cost base, pushing net income margins toward around 40% in the mid case.

The upside path requires UltraSMR adoption to accelerate on schedule and HAMR ramp costs to normalize faster than modeled. The downside risk is a HAMR qualification slip that delays the 2027 volume ramp, compressing near-term capacity growth and giving Seagate an opening to take incremental hyperscaler share. The broader structural risk is that LTAs are not take-or-pay contracts. WDC’s capacity commitments rest on demand signals that have been consistently accurate but are ultimately not guaranteed.

Street analysts stand at 17 Buys, 4 Outperforms, 4 Holds, 2 No Opinions, and 1 Underperform, with a mean target of around $508 per TIKR. The Street is broadly constructive. The disagreement is not whether the thesis is real, but how long the demand cycle holds.

Conclusion

One milestone determines whether the TIKR mid-case path to around $800 by 6/30/30 holds: whether 40-terabyte ePMR exits qualification and enters volume production on schedule in the second half of calendar 2026. The Q4 FY2026 earnings report on July 29, 2026, is the first read. Watch gross margin against the company’s guided 51% to 52% range, the terabytes-per-unit shipped figure, and any commentary on HAMR customer qualification progress. A gross margin print above 52% alongside rising terabytes per unit would confirm the road map is tracking, and the current pullback from $525 would look, in retrospect, like the last clean entry before the inflection.

See what stocks billionaire investors are buying so you can follow the smart money with TIKR.

Should You Invest in Western Digital?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up Western Digital, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Western Digital alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Western Digital on TIKR Free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!