Key Takeaways:

- Integrated Scale: Eni generated €87 billion in revenue over the last twelve months, reflecting diversification across upstream, refining, chemicals, and renewables that reduces single-cycle dependence.

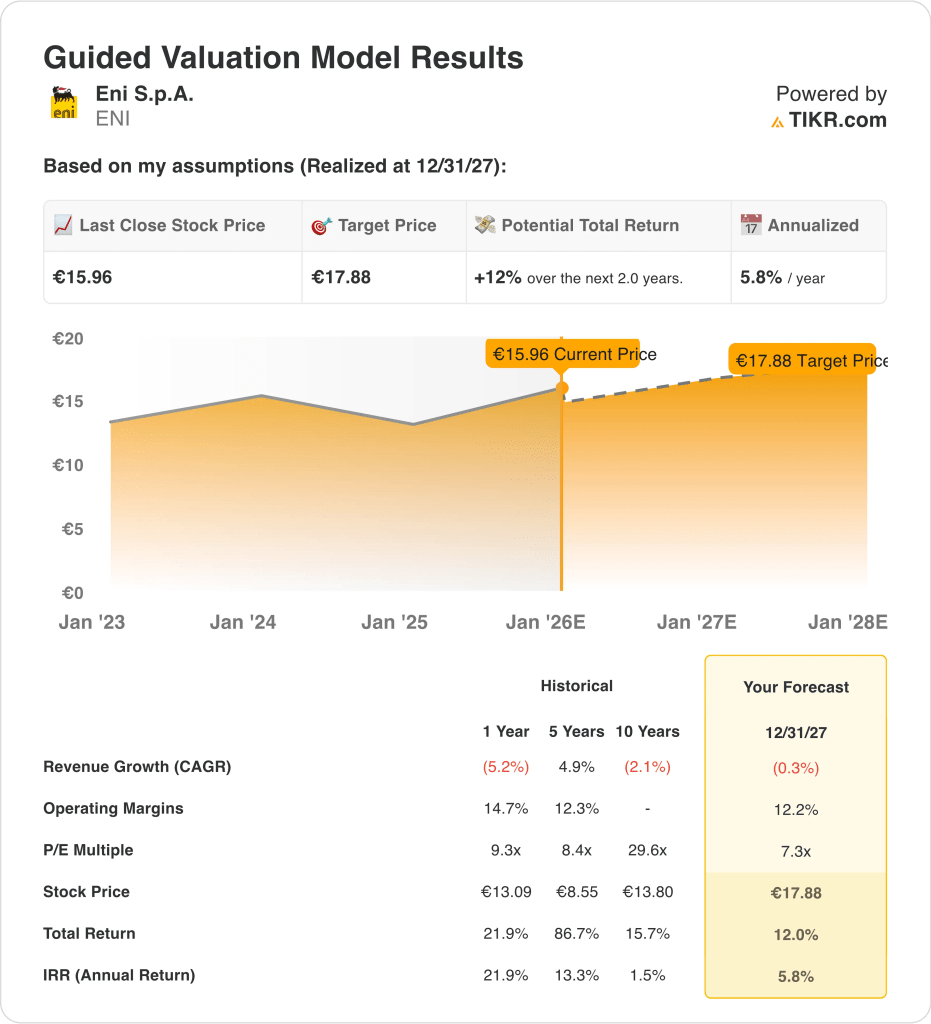

- Price Projection: Based on valuation assumptions, Eni stock could reach €18 by the end of 2027.

- Potential Gains: This target represents about 12% total upside from the current price near €16.

- Annual Return: The implied outcome equates to roughly 6% annualized returns over the next two years, supported by dividends and cash flow rather than multiple expansion.

Eni S.p.A. (ENI) is maintaining a balanced energy strategy, combining upstream cash generation with expanding renewables and disciplined capital returns across a volatile European energy backdrop.

Recent disclosures show BlackRock holding about 5% of Eni, reinforcing institutional confidence in capital discipline and long-term positioning amid volatile European energy conditions.

Over the last twelve months, Eni generated about €87 billion in revenue and €4 billion in EBIT, reflecting normalization following peak commodity pricing rather than volume-driven growth.

Operating margins stood between 10-12% which shows how integrated operations and cost control offset weaker upstream realizations and refining margin normalization.

Net income reached roughly €2.7 billion LTM while free cash flow totaled around €5.6 billion, supporting dividends near €1 per share and ongoing shareholder distributions.

Despite stable cash generation and transition assets gaining scale, the stock trades near 7 times forward earnings, raising the question of whether valuation fully reflects earnings durability outside commodity cycles.

What the Model Says for Eni Stock

We analyzed Eni’s valuation based on its integrated energy operations, resilient cash generation, and shareholder-focused capital returns across volatile commodity cycles.

Assuming 0.3% annual revenue growth, 12.2% operating margins, and a 7.3× exit P/E, the model reflects mature energy economics. Under these assumptions, Eni stock could reach €18 by 2027.

That implies a 12.0% total return from €16, or 5.8% annualized returns over the next two years.

Want to know if Eni’s payout and earnings justify its price? Run the numbers for free on TIKR →

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for ENI stock:

1. Revenue Growth: -0.3%

Eni’s revenue normalized following the 2022–2023 commodity price spike, with last twelve month revenue of €87 billion reflecting structurally lower realized prices rather than volume contraction.

Revenue declined from peak levels as oil and gas pricing moderated, confirming Eni’s exposure to commodity cycles rather than sustained volume-driven expansion across upstream and refining segments.

Upstream production remains stable, but price volatility limits sustained top-line growth beyond inflation-adjusted levels in mature European and global energy markets.

Growth contributions increasingly come from Enilive and Plenitude, though these businesses remain smaller relative to hydrocarbons and cannot yet offset upstream normalization.

Forward expectations indicate flat to low single-digit revenue movement as energy demand stabilizes and pricing normalizes across Europe and global markets.

According to consensus analyst estimates, a -0.3% revenue growth assumption reflects mature energy markets, normalized pricing, and incremental diversification partially offsetting upstream cyclicality.

2. Operating Margins: 12.2%

Eni generated over €4 billion in EBIT on roughly €87 billion in revenue over the last twelve months, producing operating margins near 12% after normalization from cycle highs.

Margins compressed from elevated levels as upstream realizations normalized and refining margins eased, consistent with late-cycle energy conditions.

Historically, Eni’s EBIT margins have ranged between high single digits and low teens across commodity cycles, positioning current profitability near long-term averages.

Integrated operations balance upstream swings with downstream, chemicals, and power contributions, reducing margin volatility but limiting upside during favorable cycles.

Cost discipline and portfolio optimization support margin stability, though transition investments add resilience at structurally lower margins than upstream production.

In line with analyst consensus projections, a 12.2% operating margin reflects normalized pricing, integrated operations, and cost control within a mature energy-cycle environment.

3. Exit P/E Multiple: 7.3x

Eni currently trades near 7 times forward earnings, consistent with European integrated energy peers and reflective of income-focused valuation frameworks.

Historical valuation ranges show limited multiple expansion even during favorable commodity cycles, reinforcing conservative market treatment of cyclical energy earnings.

Investors primarily value Eni on cash yield, balance sheet strength, and payout durability rather than long-term growth optionality.

Dividend distributions and buybacks anchor valuation support while simultaneously limiting expectations for sustained re-rating.

Meaningful multiple upside would require structurally higher returns from transition assets, which remain early-stage contributors to group profitability.

Based on consensus market estimates, a 7.3× exit multiple balances cash generation and income visibility against cyclical exposure and limited re-rating potential.

Evaluate how much of Eni’s normalized cash generation is already priced in, run your own valuation assumptions on TIKR for free →

What Happens If Things Go Better or Worse?

Energy outcomes remain tied to commodity pricing, capital discipline, and how quickly transition assets scale. Here is how Eni stock might look in different scenarios through 2027.

- Low Case: If energy prices weaken further and upstream realizations fall, revenue growth plays around 2% and margins drift toward low 5% → -0.7%% annual return.

- Mid Case: If prices stabilize and integrated operations hold margins near 6%, with revenue growth of 2% → about 5% annual return.

- High Case: If pricing firms modestly and transition assets contribute more cash flow with revenue growth at 2.3% and margins improve toward 6% → could reach 10% annual return.

Eni has moved into a post-cycle phase where cash generation and shareholder distributions matter more than volume expansion.

Reaching roughly €18 per share by 2027 is achievable if margins stay near current levels and valuation remains anchored to cash flow stability rather than renewed multiple expansion.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!