Key Stats for GOOGL Stock

- Past week’s performance: -9.2%

- 52-week range: $141 to $349

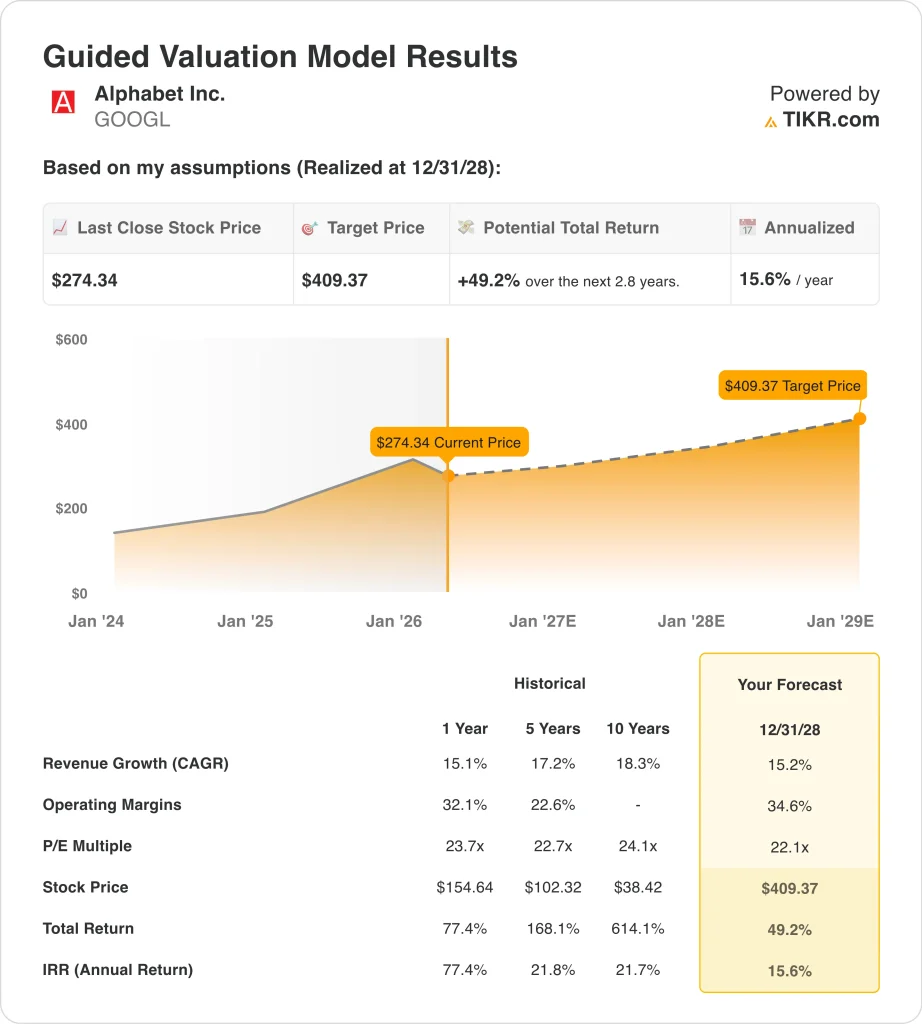

- Valuation model target price: $409

- Implied upside: 49.2% over 2.8 years

Value your favorite stocks like GOOGL with 5 years of analysts’ forecasts using TIKR’s new Valuation Model (It’s free) >>>

What Happened?

Alphabet (GOOGL) stock fell about 9.2% over the past week, and the sell-off looked more like a risk-reset than a fundamental breakdown. The biggest news overhang was a Los Angeles jury verdict that found Google and Meta liable in a youth social media addiction case. That ruling raised concern that more lawsuits could target YouTube’s design features and increase legal risk across large internet platforms.

The pressure also came during a weak stretch for large-cap tech. Reuters reported that the Nasdaq entered correction territory as investors weighed Middle East tensions, social media verdict risk, and whether Big Tech’s huge AI spending will produce enough returns. Alphabet was directly named among the stocks under pressure in that broader move.

At the same time, investors are still debating Alphabet’s AI buildout. The company said in February that 2026 capital expenditures are expected to be $175 billion to $185 billion, up sharply from $91.4 billion in 2025, as it expands servers and data centers. That level of spending can support Google Cloud, Gemini, and Search, but it also keeps the market focused on near-term payback.

There was also a more company-specific policy issue in the background. Google said on March 18 that it was working with the UK’s Competition and Markets Authority on new digital market rules and on options that could let users opt out of some AI search features. That does not change the core business today, but it reminds investors that Alphabet is balancing rapid AI product launches with rising regulatory scrutiny.

See analysts’ growth forecasts and price targets for GOOGL (It’s free) >>>

Is GOOGL Stock Undervalued?

Under valuation model assumptions realized through 12/31/28, the stock is modeled using:

- Revenue growth (CAGR): 15.2%

- Operating Margins: 34.6%

- Exit P/E Multiple: 22.1x

Based on these inputs, the model estimates a target price of $409.37, implying 49.2% total upside from the current share price and a 15.6% annualized return over the next 2.8 years.

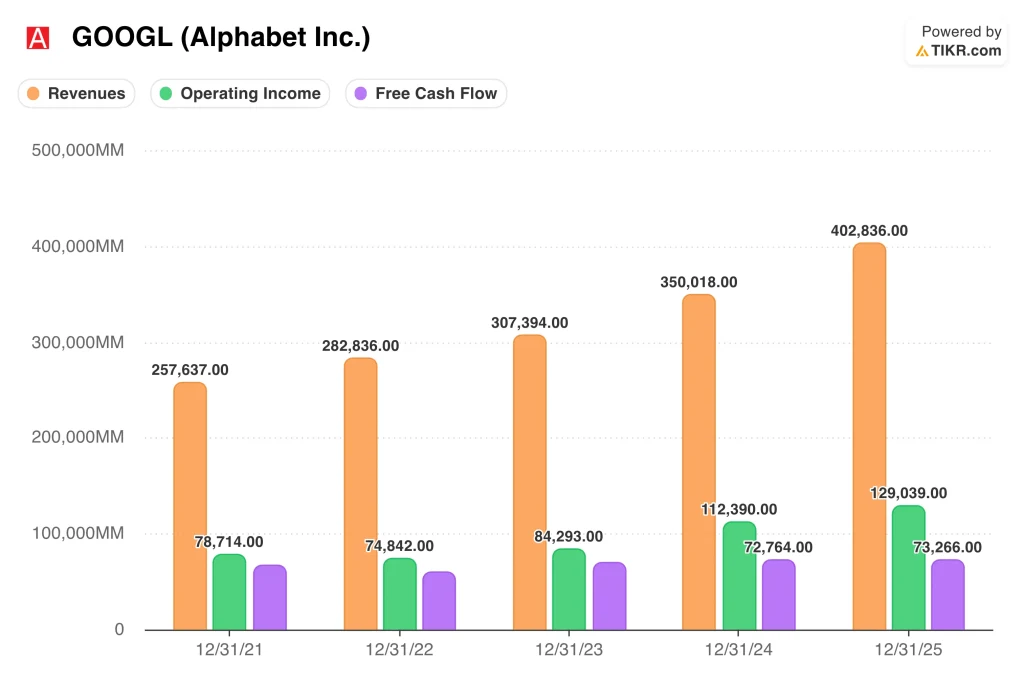

That setup looks demanding, but not extreme, when compared with Alphabet’s recent business results. Revenue rose 15.1% in 2025 to $402.8 billion, while operating income climbed 14.8% to $129.0 billion. Free cash flow reached $73.3 billion, so the model is asking for growth that is close to Alphabet’s current scale-adjusted performance, not a dramatic reacceleration.

Margins are also central to the valuation. The model assumes 34.6% operating margins, above the 32.0% LTM figure and above the 32.1% one-year historical level shown in the valuation image. That means the upside case depends on Alphabet turning AI demand into higher-margin revenue faster than costs rise, especially in Cloud and Search.

The multiple does not look stretched against the company’s own history. The model uses a 22.1x exit P/E, which is below the 23.7x one-year historical P/E and close to the 22.7x five-year historical level shown in the valuation image. With the stock at 23.7x NTM earnings and with a $376.93 street target price, the market is valuing Alphabet more like a mature compounder than a pure AI momentum name.

Alphabet also has balance-sheet flexibility that many peers do not. It ended the period with $126.8 billion in cash and short-term investments and with net cash of $59.8 billion. That matters because the company can fund AI infrastructure, buy back stock, and absorb legal or regulatory shocks without depending on outside capital.

What’s Driving the GOOGL Stock Going Forward?

The next major catalyst is Q1 2026 earnings, which are expected on April 21, 2026. Investors will want to see whether Google Cloud can sustain the momentum that helped drive Q4 and whether AI products are lifting demand across both enterprise software and core advertising. They will also look for any change to the massive 2026 capex plan.

Management has already framed the long-term opportunity clearly. In the Q4 2025 earnings release, CEO Sundar Pichai said, “It was a tremendous quarter for Alphabet and annual revenues exceeded $400 billion for the first time.” He also said Gemini 3 was a major milestone and that Cloud and YouTube finished the year with strong momentum, which matters because those are two of Alphabet’s most visible AI monetization engines.

Cloud remains one of the most important business drivers. In Q4, Google Cloud revenue rose 48% to $17.7 billion, and Reuters reported that the growth was fueled by AI demand and by continued compute constraints. That is important because cloud revenue is more incremental to Alphabet’s AI thesis than mature Search revenue, and it can justify higher margins if utilization stays strong.

Search still matters most to the numbers, though, and that is where regulatory and product risks are most sensitive. Alphabet is dealing with UK digital market remedies, fresh legal scrutiny around platform design, and constant investor questions about whether AI answers will reshape the economics of search advertising. So the stock likely needs both durable and growth and visible AI monetization to regain momentum from here.

Estimate a company’s fair value instantly (Free with TIKR) >>>

Should You Invest in Alphabet Inc.?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up GOOGL, and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track GOOGL alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Analyze Alphabet stock on TIKR Free→

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!