Key Stats for Norfolk Southern Stock

- Past-Week Performance: +0.8%

- 52-Week Range: $201.6 to $319.9

- Current Price: $283.3

What Happened?

Norfolk Southern (NSC) delivered its sharpest productivity result in years as the freight railroad, which hauls merchandise, intermodal containers, and coal across the eastern U.S., cut its adjusted operating ratio to 65.3% in Q4 2025 while simultaneously outlining a pending $85 billion merger with Union Pacific that would create the nation’s first coast-to-coast rail network, all while the stock sits at $283.25 against a 52-week high of $319.94.

The January 29 earnings report showed NSC posting adjusted EPS of $3.22 against an LSEG consensus estimate of $2.76, a 17% beat driven by $216 million in full-year productivity savings under its PSR 2.0 program, which stands for Precision Scheduled Railroading and is the operational discipline framework the company uses to run fewer, longer, more efficient trains.

Underneath the EPS beat, the operational proof point that makes the efficiency story credible is the 7% headcount productivity figure NSC achieved in 2025, moving 3% more gross ton miles, which measure total freight weight hauled, with 4% fewer employees, while free cash flow surged to $2.2 billion, nearly $500 million above the prior year.

The January 2026 ribbon-cutting of Warrior Met Coal’s new Blue Creek metallurgical coal mine in Alabama, a two-year partnership NSC helped finance by expanding its line to the Port of Mobile, adds up to 6 million tons of annual coal volume to a network that recorded record merchandise revenue in 2025 across every underlying business group.

CEO Mark George stated on the Q4 2025 earnings call that “whatever revenue growth we do get, it’s going to drop through at attractive incrementals given the capacity that we have,” a comment grounded in a 2026 capital budget reduced to $1.9 billion, a $450 million two-year reduction, leaving the network structurally ready for volume upside without incremental spending.

NSC’s competitive position over the next three to five years rests on three converging forces: the STB merger application resubmission targeted for April 30, the $650 million cumulative cost takeout the company expects to reach by year-end under PSR 2.0, and a restructured commercial organization with incentivized specialized sales roles now live across the network, all pointing toward a railroad that has already compressed its operating ratio by roughly a full point in two years and is positioned to accelerate that trajectory if merger approval unlocks single-line pricing power against truck.

Wall Street’s Take on NSC Stock

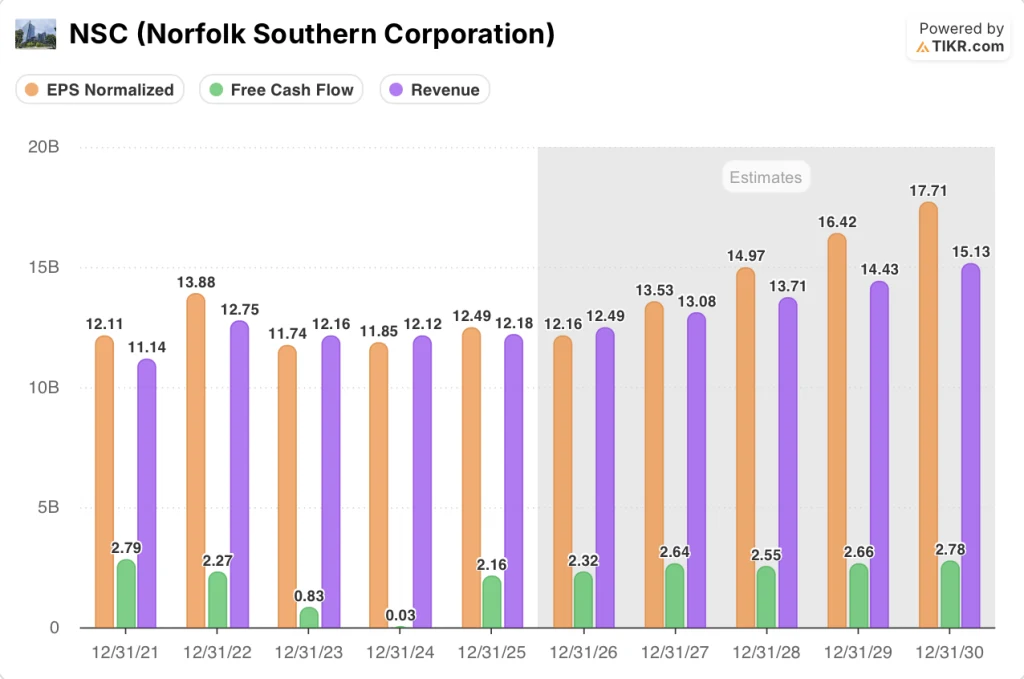

The $2.16 billion in free cash flow NSC generated in FY2025, recovering from a near-zero $0.03 billion in FY2024, confirms that the PSR 2.0 cost overhaul, which drove $216 million in productivity savings, has fundamentally reset the railroad’s earnings power rather than simply timing cost items.

The FY2026 normalized EPS dip to $12.16 from $12.49 in FY2025 reflects headwinds management already quantified: roughly 4% wage and benefits inflation, a 25% insurance premium spike, and normalized land sale income falling from approximately $70 million back to a $30 million to $40 million run rate.

Additionally, as TIKR estimates, EPS is set to rebound to $13.53 in FY2027 as the $150 million in new cost takeouts compound on top of the $500 million already captured over two years, revenue will scale toward $13.08 billion, and the Warrior Met Coal Blue Creek mine, now fully operational and targeting up to 6 million annual tons, will add a contracted volume source the FY2025 results did not yet fully reflect.

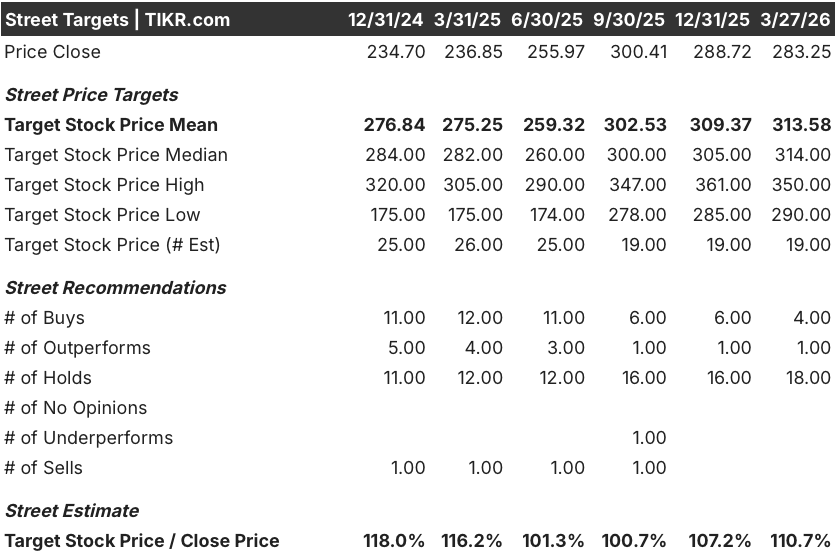

However, Wall Street is cautiously constructive but not yet convicted: 4 buys, 1 outperform, and 18 holds among 23 analysts arrive at a mean price target of $313.58, implying 10.7% upside from $283.25, as analysts await confirmation that volume recovery materializes alongside the already-proven cost structure.

The analyst target range spans $290 on the low end to $350 on the high end, with the floor essentially pricing in continued merger overhang and soft intermodal demand, while the $350 ceiling reflects a scenario where the Union Pacific STB resubmission on April 30 advances without further procedural friction.

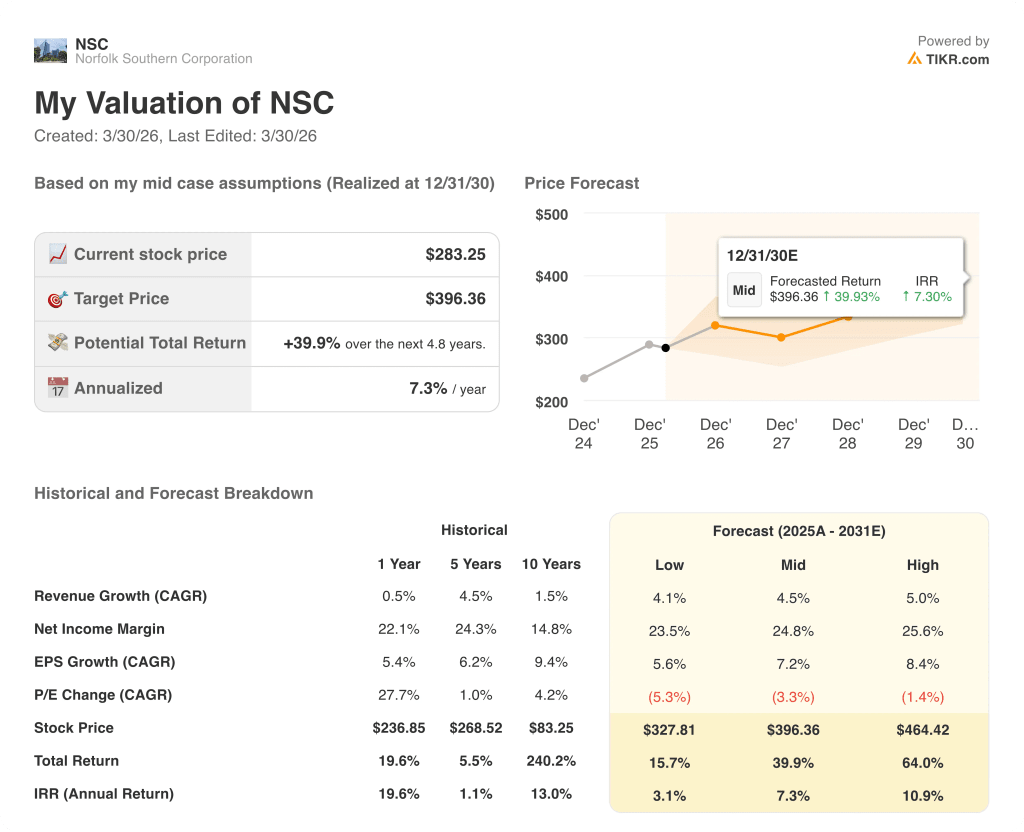

What Does the Valuation Model Say?

TIKR’s model implies FCF margin expanding from 17.7% in FY2025 to 20.2% by FY2027, a trajectory justified by the $450 million two-year capital budget reduction to $1.9 billion and the railroad’s latent network capacity to absorb volume without proportional cost additions.

The market is treating NSC as a stagnant Hold while FCF has compounded from near-zero to $2.16 billion in a single year, making the current 23.3x forward earnings multiple look misaligned with a railroad now operating at decade-best safety and efficiency levels.

The Warrior Met Coal Blue Creek ramp, targeting up to 6 million annual tons from a mine now fully operational, gives TIKR’s modest 2.5% revenue growth assumption for FY2026 a concrete, contracted volume source that the consensus has not fully priced in; TIKR’s mid-case price target of $313.58 rests partly on this incremental coal contribution.

Also, management’s guidance of flat-to-down headcount against a network capable of absorbing several points of volume growth signals that incrementals on any revenue recovery will drop through at unusually high margins, a dynamic the 18 Hold ratings on the street have not yet rewarded.

If intermodal volumes, already down 6% quarter-to-date through mid-March and pressured by trade tariff uncertainty and CSX competitive response, deteriorate further in FY2026, TIKR’s $12.49 billion revenue estimate breaks and the FCF expansion thesis loses its primary growth engine.

The April 30 STB merger resubmission is the single event to watch: a procedurally complete filing advances the timeline toward a potential H1 2027 close and re-rates the stock toward the $350 analyst high target, while a second rejection resets the overhang and pressures the $290 floor.

Should You Invest in Norfolk Southern Corporation?

The only way to really know is to look at the numbers yourself. TIKR gives you free access to the same institutional-quality financial data that professional analysts use to answer exactly that question.

Pull up NSC stock and you’ll see years of historical financials, what Wall Street analysts expect for revenue and earnings in the quarters ahead, how valuation multiples have moved over time, and whether price targets are trending up or down.

You can build a free watchlist to track Norfolk Southern Corporation alongside every other stock on your radar. No credit card required. Just the data you need to decide for yourself.

Access Professional Tools to Analyze NSC stock on TIKR for Free →