Key Takeaways:

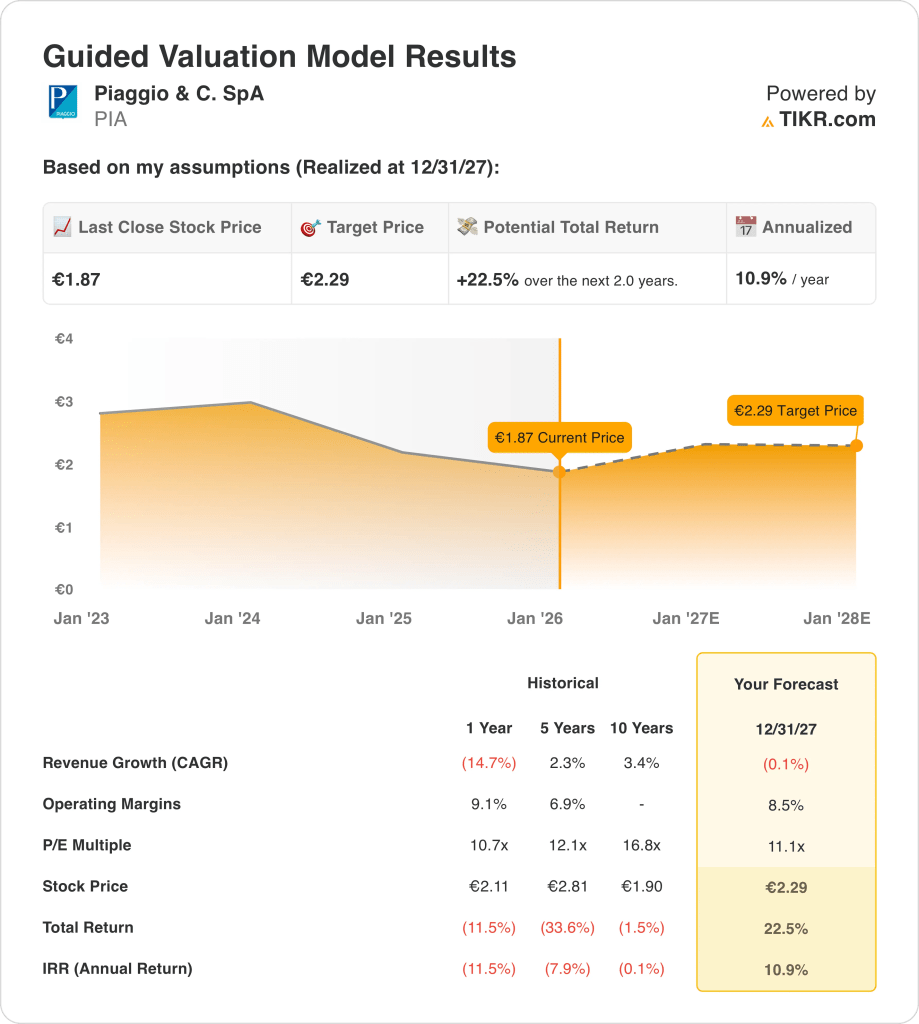

- Price Projection: Based on current operating assumptions, Piaggio stock could reach €2 by 2027 from today’s €2 price.

- Potential Gains: This implies a total upside of 23% over the next 2 years as margins stabilize and earnings recover.

- Annual Return: The model points to an annualized return of 11% through 2027 driven by execution rather than valuation expansion.

Piaggio & C. SpA (PIA) designs and sells scooters, motorcycles, and light commercial vehicles, generating about €2 billion in annual revenue through brands such as Vespa, Aprilia, and Moto Guzzi across Europe and Asia.

In 2025, Piaggio expanded its product lineup at EICMA and entered the Philippine market, reinforcing its global footprint while holding an 18% share of the European scooter market.

Revenue declined to roughly €2 billion in 2024 after weaker demand, but the scale of its brand portfolio remains critical for sustaining volume across cycles.

Operating margins around 9% reflect stable cost control despite lower volumes, showing that profitability has not deteriorated in line with revenue.

Even with established brands and steady margins, the stock trades near €2 with a valuation around 11x earnings, raising questions about whether the market is fully accounting for normalization in demand and earnings.

What the Model Says for PIA Stock

We assessed Piaggio’s outlook using assumptions centered on brand resilience, stable volumes, and cost discipline in a cyclical two-wheeler market.

With -0.1% revenue growth, 8.5% operating margins, and an 11.1x exit multiple, the model reflects normalization rather than aggressive recovery.

This supports a €2 target price, implying a 22.5% total return or a 10.9% annualized return over two years.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for PIA stock:

1. Revenue Growth: -0.1%

Piaggio’s revenue base has been volatile, with a -15% decline over the past year contrasting with a 3% ten-year CAGR, highlighting cyclical exposure and uneven regional demand, according to aggregated analyst estimates reflecting historical instability.

Recent performance shows revenue near €1.6 billion with ongoing pressure from Europe and Asia, while India and scooter replacement demand provide partial offsets without restoring prior growth momentum, according to surveyed analyst expectations grounded in current sales trends.

Looking forward, new model launches and geographic expansion, including Southeast Asia, support volume stability, but pricing limits and consumer caution cap upside over the next two years, based on street consensus estimates balancing catalysts and risks.

A -0.1% revenue growth assumption reflects stabilization rather than recovery, aligning muted demand with Piaggio’s mature product mix and limited near-term volume acceleration.

2. Operating Margins: 8.5%

Piaggio has historically operated with margins between roughly 7% and 9%, placing current profitability near the upper end of its long-term range despite weaker volumes, according to pooled market forecasts informed by cycle positioning.

Recent results show margins around 9% as cost controls and manufacturing discipline offset lower utilization, indicating earnings resilience even as revenue contracted year over year, according to consensus analyst estimates tied to recent financials.

Forward margin support comes from mix improvement in premium scooters and efficiency initiatives, while wage pressure and input costs limit expansion beyond recent levels, based on consensus market estimates reflecting balanced margin drivers.

According to consensus analyst estimates, an 8.5% operating margin assumption represents normalized profitability that sustains cost discipline without assuming material efficiency gains or pricing relief.

3. Exit P/E Multiple: 11.1x

Piaggio’s shares have historically traded between roughly 10x and 17x earnings, with current valuation closer to cycle trough levels following earnings pressure and softer investor sentiment, according to aggregated analyst estimates referencing historical ranges.

Market caution reflects declining revenue, uneven cash flow, and sensitivity to consumer cycles, which constrain multiple expansion despite brand strength in Vespa and Aprilia, according to pooled market forecasts capturing investor skepticism.

For valuation support, earnings must stabilize and margins hold near current levels, while new models sustain demand without requiring aggressive growth assumptions, based on street consensus estimates emphasizing execution over optimism.

Based on consensus market estimates, an 11.1× exit multiple reflects normalized earnings quality and cautious confidence, aligning historical valuation discipline with steady but unspectacular business performance.

What Happens If Things Go Better or Worse?

Piaggio’s outcomes depend on two-wheeler demand stability, brand execution across scooters and motorcycles, and cost discipline, creating a range of possible paths through 2029.

- Low Case: If consumer demand remains cautious, pricing stays competitive, and volumes recover slowly, revenue grows around 1.2%, margins hold near 3.7%, and valuation stays constrained, leaving returns driven mainly by incremental earnings improvement → 3.9% annualized return.

- Mid Case: With core scooter brands holding share, new model launches supporting replacement demand, and costs kept under control, revenue growth near 1.4%, margins improving toward 3.8%, and stable valuation support steady compounding → 8.1% annualized return.

- High Case: If geographic expansion gains traction, product refresh cycles resonate, and operating discipline holds, revenue reaches about 1.5%, margins approach 3.8%, and valuation pressure eases, allowing stronger price recovery → 11.1% annualized return.

Steady execution on product launches, brand relevance, and cost control supports a path to the €2.55 mid-case target by 2029 through modest growth and stable margins, without relying on multiple expansion or market hype.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!