Key Takeaways:

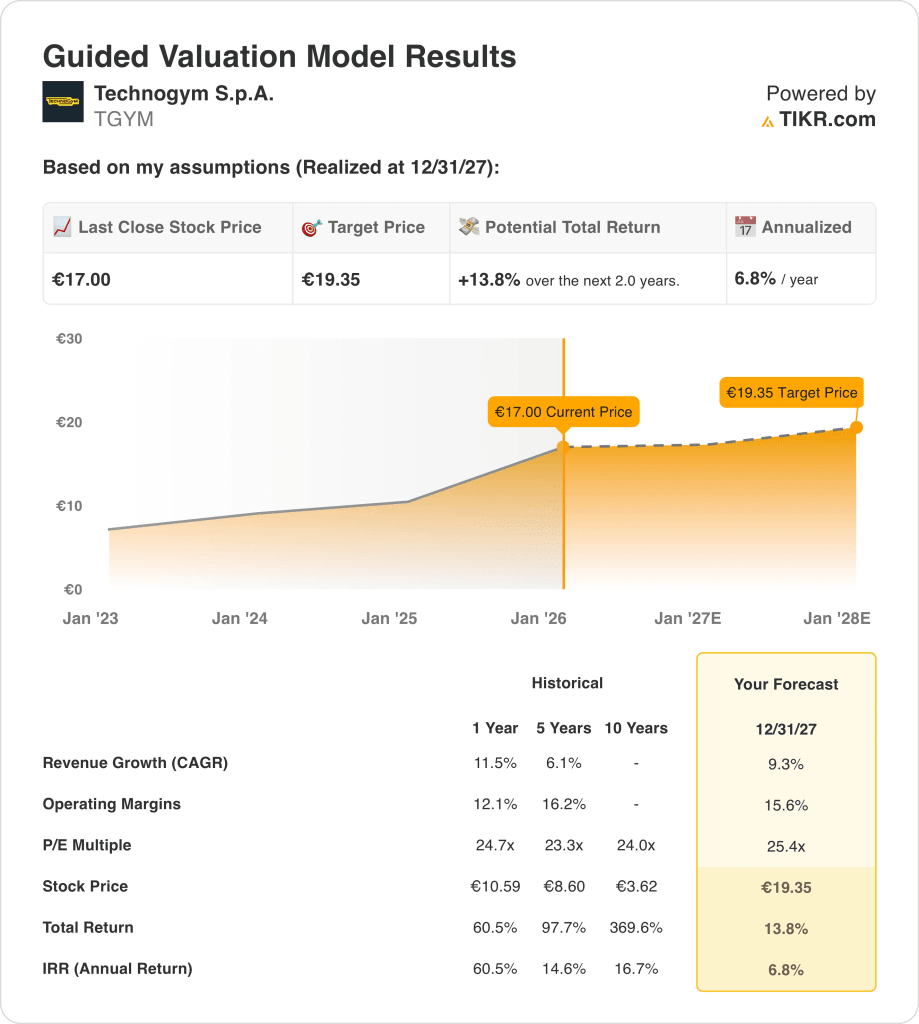

- Valuation Setup: Based on the valuation assumptions applied, Technogym’s framework points to a target price of €19 by 2027 and reflects steady revenue growth alongside normalized operating margins.

- Price Projection: The model implies upside from a current price of €17 to €19, supported by projected revenue growth of 9% and operating margins expanding to 16%.

- Potential Gains: This scenario represents a total return of 14% over the next 2 years, driven by earnings growth rather than multiple expansion.

- Annual Return: The forecast translates into an annualized return of 7% through 2027 which is consistent with a stable mid-cap consumer equipment profile.

Technogym S.p.A. (TGYM) is a fitness and wellness equipment giant that designs and sells premium solutions worldwide while generating €901 million in revenue in 2024 across commercial, hospitality, and home fitness markets.

The company recently reported Q2 2025 revenue of €280 million that beat expectations by 4%, which signals resilient demand despite slower growth in discretionary consumer spending.

For full-year 2024, Technogym delivered revenue of €901 million and normalized net profit of about €100 million, showing that scale and brand positioning continue to convert into earnings.

Operating income reached roughly €123 million in 2024, translating into operating margins near 14%, as pricing discipline and a higher mix of premium and digital products supported profitability.

Even as revenue, margins, and profits strengthen, the stock trades near €17 with an implied market value around €2 billion, indicating continued investor caution on long-term growth durability and creating tension between operating execution and valuation.

What the Model Says for TGYM Stock

The model links 9% revenue growth and 16% operating margins to Technogym’s premium positioning and steady capital returns profile.

Using a normalized 18x exit P/E, the framework projects earnings growth without multiple expansion as the primary driver of equity value.

This implies a move from €17 to €19 by 2027, equal to 14% total upside or about 7% annualized returns.

Our Valuation Assumptions

TIKR’s Valuation Model lets you plug in your own assumptions for a company’s revenue growth, operating margins, and P/E multiple, and calculates the stock’s expected returns.

Here’s what we used for TGYM stock:

1. Revenue Growth: 9.3%

Technogym delivered revenue growth of 12% in 2024 and 11% over the last year, supported by premium equipment demand and expanding digital engagement across commercial and home fitness segments.

Growth is moderating from earlier post-pandemic peaks as discretionary spending normalizes, yet recent quarterly revenue of €280 million still grew 14% year over year, indicating resilient underlying demand.

Forward growth is supported by global wellness adoption, higher penetration of connected equipment, and steady expansion across hospitality and professional fitness channels, while risks include consumer spending sensitivity and competitive pricing pressure.

According to consensus analyst estimates, a 9.3% revenue growth assumption reflects steady global demand and brand strength balanced against slower category growth and a more normalized fitness equipment cycle.

2. Operating Margins: 15.6%

Technogym’s operating margins expanded from 11% in 2021 to 14% in 2024 as scale benefits, pricing discipline, and premium product mix improved profitability across regions.

Recent operating income of €123 million demonstrates continued margin momentum, supported by higher-margin digital services and reduced cost pressure compared with earlier inflation-driven periods.

Margin risks include increased marketing investment and competitive pricing in consumer channels, while support comes from software-enabled equipment, operational efficiency, and a larger installed base.

In line with analyst consensus projections, operating margins of 15.6% represent a normalized level that balances structural efficiency gains with ongoing reinvestment to sustain long-term growth.

3. Exit P/E Multiple: 25.4x

Technogym currently trades near a forward earnings multiple in the mid-20s, reflecting its premium brand position and consistent profitability within the global fitness equipment market.

Historically, the stock has sustained valuation levels above 20x during periods of stable growth and margin expansion, supported by strong cash generation and a disciplined balance sheet.

Investor caution remains tied to category cyclicality and long-term growth durability, meaning multiple expansion depends on continued earnings delivery rather than revenue acceleration alone.

Based on street consensus estimates, a 25.4x exit multiple reflects balanced expectations that earnings growth and margin stability persist without assuming aggressive re-rating beyond recent trading ranges.

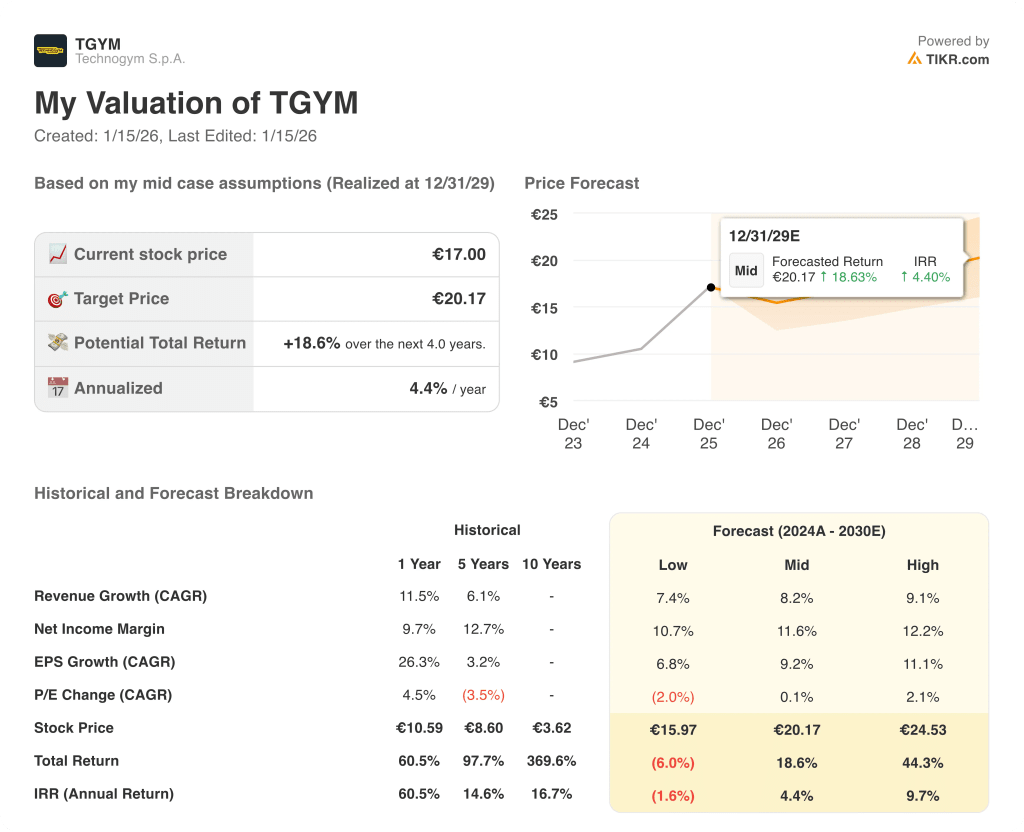

What Happens If Things Go Better or Worse?

Technogym’s outcomes depend on global fitness demand, brand-led pricing discipline, and execution across connected equipment and services, setting up a range of possible paths through 2029.

- Low Case: If demand remains uneven across consumer channels and cost discipline limits margin lift, revenue grows around 7.4%, net income margins stay near 10.7%, and valuation remains cautious, leaving returns tied to modest earnings progress → -1.6% annualized return.

- Mid Case: With core commercial and hospitality demand executing as expected, revenue growth near 8.2%, net income margins improving toward 11.6%, and valuation stability, earnings expansion supports measured upside → 4.4% annualized return.

- High Case: If premium equipment adoption and digital penetration strengthen execution, revenue reaches about 9.1%, net income margins approach 12.2%, and valuation pressure eases, allowing price appreciation to accelerate → 9.7% annualized return.

The €20.17 mid-case target price is achievable as commercial gyms continue upgrading equipment, hospitality and corporate wellness spending recovers, and connected fitness adoption supports earnings growth without requiring multiple expansion or optimistic market sentiment.

How Much Upside Does It Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

Test how sensitive Technogym’s valuation is to slower gym capex cycles or margin normalization using downside and upside scenarios on TIKR for free →

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!