Williams Companies (NYSE: WMB) has remained steady throughout 2025, supported by strong operating margins and reliable natural gas transport volumes. Shares trade near $59/share, reflecting the stock’s historically low volatility and its role as a dependable infrastructure operator.

Recently, Williams advanced important expansion work on its Transco pipeline system, which remains one of the most essential natural gas corridors in the United States. Management also highlighted rising activity from LNG export facilities, a long-term trend that continues to strengthen demand for natural gas transport. These developments show that WMB is positioned to benefit from structural energy demand even as the broader sector moves unevenly.

This article explores where Wall Street analysts believe Williams could trade by 2027. We compiled consensus targets and valuation model outputs to map the stock’s expected trajectory. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

WMB trades near $59/share, and the Street’s average target is $68/share, which points to roughly 13% upside based on the latest TIKR data. This places WMB in the modest-upside category, with analysts expecting steady gains rather than a major re-rating.

- High estimate: $83

- Low estimate: $53

- Median target: $68

- Ratings: 11 Buys, 4 Outperforms, 8 Holds, 1 Underperform, 1 Sell

The broad range of estimates suggests both optimism and caution. Bullish analysts point to improving natural gas demand trends and the durability of WMB’s contract-driven business, while more cautious voices highlight leverage and the natural limits to growth for pipeline operators. For investors, this means the stock could deliver modest outperformance if execution remains consistent, but expectations should stay realistic.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

WMB Growth Outlook and Valuation

The company’s fundamentals appear stable and supported by long-term transport contracts that help sustain margin strength and predictable earnings:

- Revenue growth forecast: 10.1%

- Operating margin: 39.1%

- Forward P E used: 23x

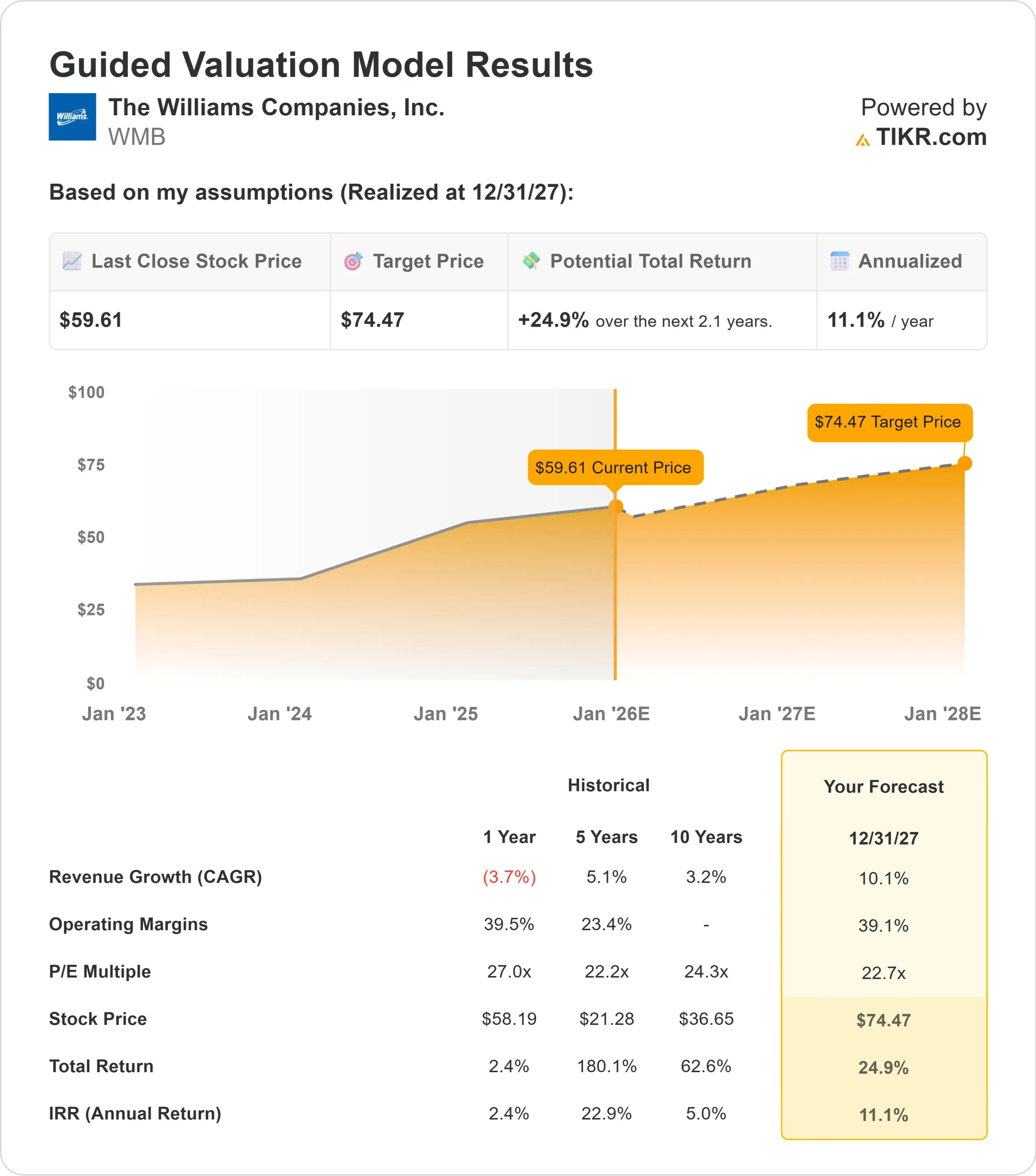

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23x forward P E suggests about $74/share by 2027

- That implies roughly 25% upside, or about 11% annualized returns

These numbers indicate that Williams can compound steadily, driven by consistent throughput volumes and a business model designed for stability. Growth is not expected to accelerate meaningfully, but the company’s recurring revenue base and strong infrastructure footprint create a clear and dependable return path.

For investors, WMB behaves more like a stability-focused energy operator than a high-growth opportunity. Returns are likely to remain anchored in predictable cash flow rather than rapid expansion, which may appeal to those seeking long-term consistency.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts remain optimistic because Williams sits at the center of long-term natural gas demand. Its infrastructure supports essential transportation needs, and the company continues to play an important role in supplying gas to power generation, industrial facilities, and LNG export terminals.

Management’s commitment to expanding key pipeline corridors reinforces confidence in future throughput. These projects help improve long-term capacity and strengthen WMB’s relevance in the U.S. energy system. For investors, these factors point to a business with durable demand and a long runway of operational stability.

Bear Case: Leverage and Limited Repricing

Despite its strengths, WMB faces constraints that may limit how much upside investors ultimately see. The company’s sizable debt load can make it difficult for valuations to expand and can increase sensitivity to interest rate conditions.

There is also the risk that growth normalizes over time. Pipeline operators historically settle into a slower, more predictable pace that limits the potential for outsized returns. For investors, the bear case centers on WMB delivering steady results without exceeding the market’s current expectations.

Outlook for 2027: What Could Williams Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 23x forward P E suggests WMB could trade near $74/share by 2027. That represents roughly 25% upside from today or about 11% annualized returns.

This outlook reflects a realistic and steady performance path. It assumes consistent operations and supportive natural gas demand. For WMB to exceed this range, the company would likely need to deliver stronger than expected throughput, greater benefits from expansion projects, or meaningful progress in reducing leverage.

For investors, WMB presents a clear path to stable and reliable compounding. The stock’s upside is moderate but supported by predictable earnings and long-term demand for natural gas transportation.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>