Cheniere Energy (NYSE: LNG) trades near $205/share after a stretch of volatility in global LNG markets. Softer pricing and slower year over year growth have weighed on results, but Cheniere remains the largest LNG exporter in the United States with a stable contract driven business model. Analysts continue to view the company as a dependable long term operator with meaningful upside potential.

Recently, Cheniere advanced its next expansion phase at the Corpus Christi Stage 3 project and secured new long duration sales agreements that extend its commercial visibility well into the next decade. Forward expectations remain solid as capacity additions stay on schedule. These developments show that the company continues to execute well even as broader LNG sentiment cools.

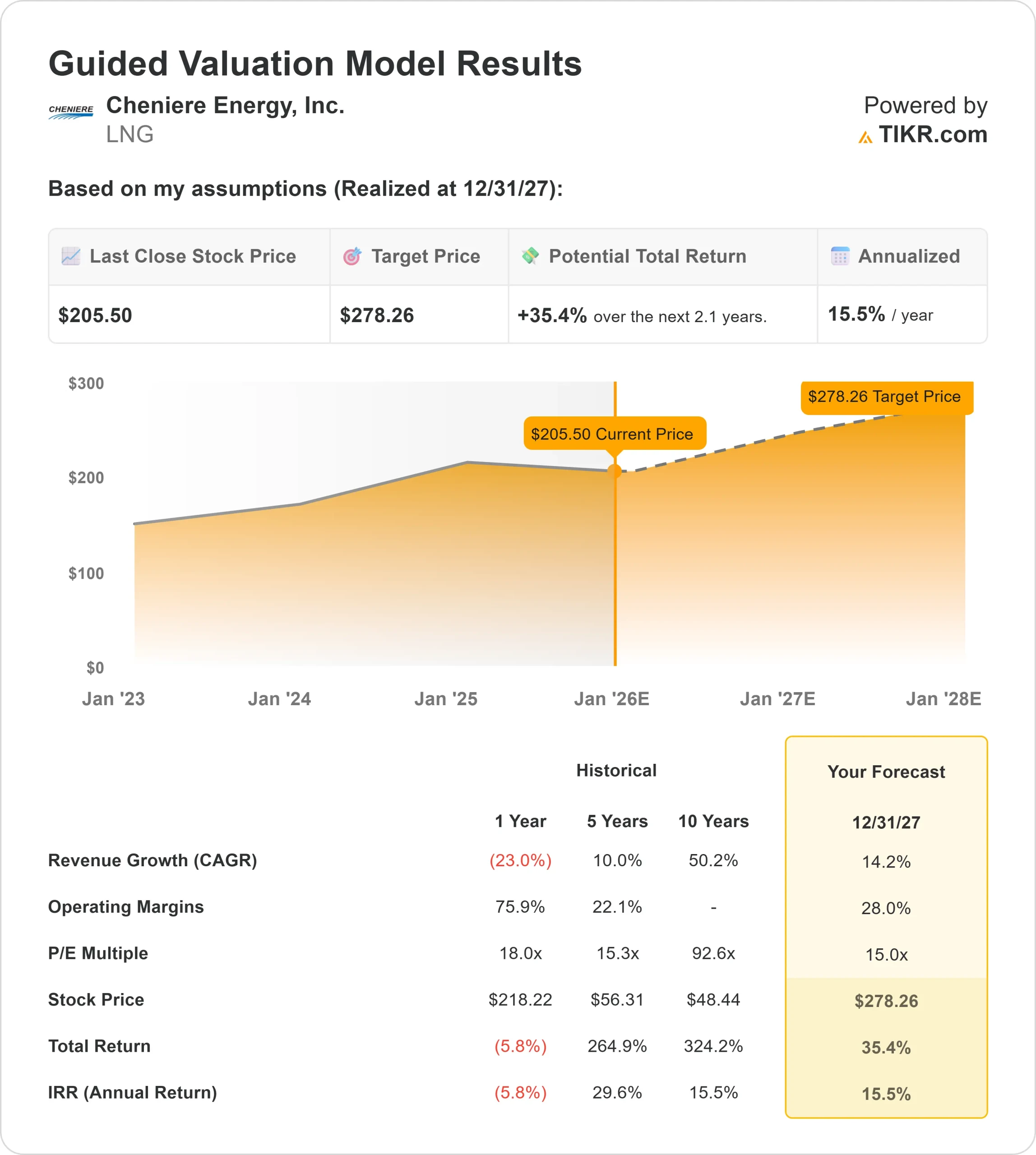

This article outlines where analysts believe the stock could be headed by 2027, based on consensus expectations and TIKR’s Guided Valuation Model. These figures reflect analyst assumptions and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

LNG trades around $205/share today. The latest average analyst price target is $271/share, which suggests about 32% upside. This places the stock firmly in the meaningful upside category.

- High estimate: $290

- Low estimate: $241

- Median target: $274

- Ratings: 14 Buys, 7 Outperforms, 3 Holds

For investors, the tight range across these estimates is important. Analysts appear confident in Cheniere’s long term earnings stability, supported by multi year contracts and consistent export volumes. Downside risk looks limited unless global LNG demand weakens significantly.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

LNG: Growth Outlook and Valuation

The company’s fundamentals appear steady and supported by predictable cash flow:

- Revenue is projected to grow about 14.2% through 2027

- Operating margins are expected to remain near 28%

- Shares trade at a forward P E of 15x

- Based on analysts average estimates, TIKR’s Guided Valuation Model using a 15x forward P E suggests about $278/share by 2027

- That implies roughly 35% upside, or about 15% annualized returns

These numbers suggest Cheniere can compound steadily without requiring aggressive assumptions. The business benefits from long term contracts, reliable export demand, and meaningful scale advantages that support stable margins.

For investors, LNG functions more like a dependable cash flow operator than a cyclical commodity play. As long as volumes hold and execution remains consistent, the stock has a clear path to steady long term gains.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Cheniere benefits from a highly predictable business model. Long term LNG contracts help stabilize revenue, and global demand continues to expand as countries transition away from coal. Ongoing expansion projects also extend Cheniere’s growth runway and reinforce its position as a major supplier in the global energy landscape.

For investors, these strengths suggest a dependable operator with consistent earnings potential. The company’s focus on contract driven cash flow supports the outlook for long term compounding.

Bear Case: Key Risks to Monitor

Despite strong fundamentals, Cheniere faces several risks. The company operates with significant financial obligations tied to its infrastructure assets, and long term LNG pricing trends remain important for future contract negotiations. Market sentiment can shift quickly if global demand cools or if LNG prices decline for an extended period.

For investors, these risks do not undermine Cheniere’s stability, but they can affect valuation. Long term performance will depend on consistent execution, financial discipline, and the broader trajectory of global LNG demand.

Outlook for 2027: What Could LNG Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model using a 15x forward P E suggests LNG could trade near $278/share by 2027. That represents about 35% upside, or roughly 15% annualized returns.

This outlook already assumes solid execution on margins, contract volumes, and expansion progress. Stronger upside would likely require a more favorable pricing environment or a faster ramp in new capacity. Even without that, investors can expect steady compounding supported by long term contract visibility.

For investors, LNG stands out as a durable operator with a clear path to stable long term returns. The company’s contract driven model and continued expansion efforts provide a strong foundation for performance over the next several years.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>