Waters Corporation (NYSE: WAT) trades near $394/share after a strong rebound in 2025. The stock has climbed steadily from its mid year lows as sentiment around instrument demand and lab spending improved. Even with the recovery, analysts still expect modest returns because growth remains steady rather than accelerating.

Recently, Waters reported better than expected performance across key pharmaceutical and biotech markets, with management noting stronger momentum in chromatography systems and expanding service contract adoption. These improving trends have helped offset softer demand in industrial and academic customer segments and continue to support the company’s steady earnings profile.

This article explores where analysts think Waters could trade by 2027. We used consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Flat to Slight Downside

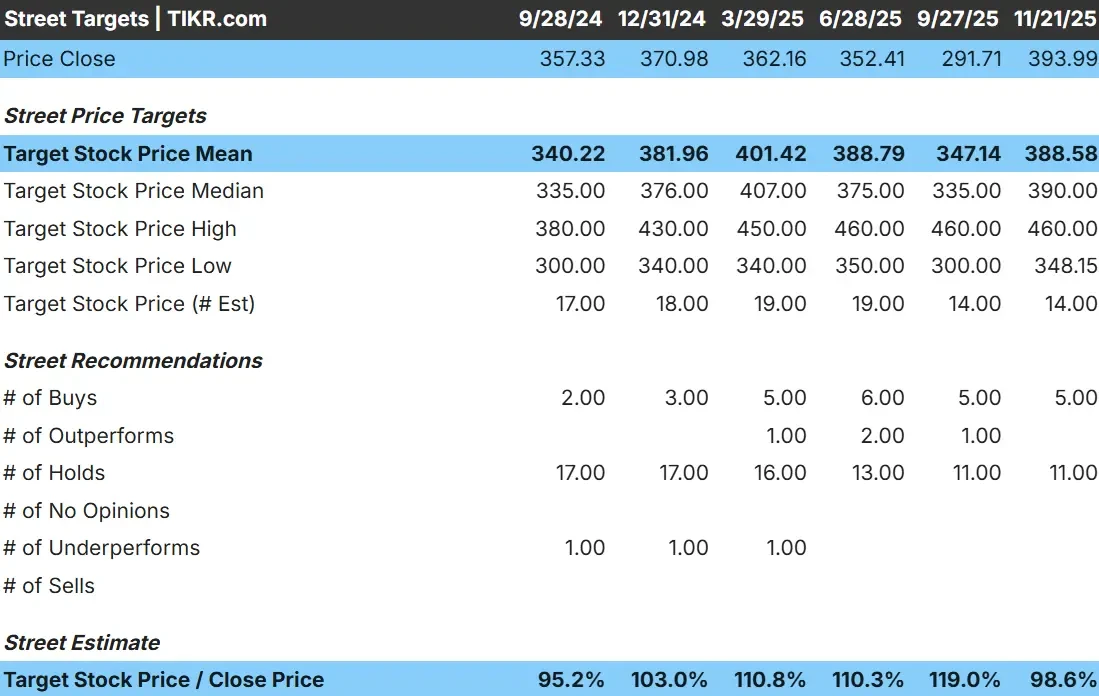

Waters trades around $394/share, and analysts currently estimate an average target of $389/share, which implies about 1% downside. The tight spread between the high and low estimates suggests analysts believe the stock is fairly valued at current levels.

- High estimate: $460/share

- Low estimate: $348/share

- Median target: $390/share

- Ratings: 5 Buys, 11 Holds

For investors, the takeaway is straightforward. Analysts expect the stock to remain relatively stable, with limited movement in either direction. The market appears to be pricing in most of Waters steady fundamentals unless a stronger catalyst emerges.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Waters: Growth Outlook and Valuation

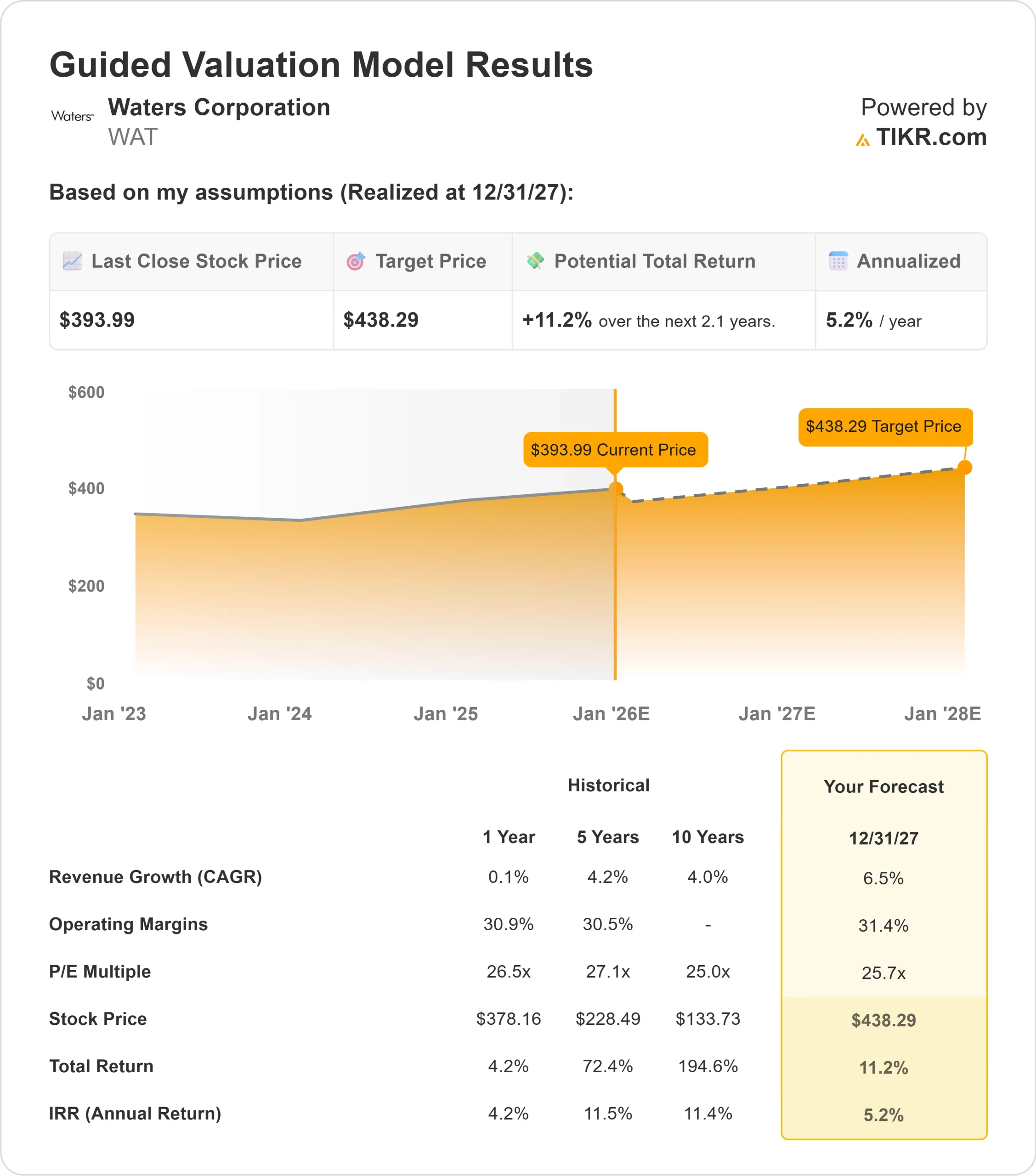

The company’s fundamentals appear steady and predictable, supported by recurring revenue and consistent profitability.

- Revenue is projected to grow 6.5% through 2027

- Operating margins are expected to hold near 31.4%

- Shares trade at roughly 26x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 26x forward P E suggests about $438/share by 2027

- That implies roughly 11% upside, or about 5% annualized returns

These numbers point to a stock that compounds gradually rather than aggressively. Waters valuation already reflects its stable fundamentals, which means upside depends on steady demand, recurring service revenue, and consistent margin execution.

For investors, Waters looks more like a dependable compounder than a fast growth story. The company’s predictable revenue base and strong margins provide a solid foundation, but meaningful upside will likely require stronger equipment demand or another improvement in its long term growth outlook.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Waters remains a key player in analytical instruments used across pharmaceutical and life sciences research. Its large installed base supports strong recurring revenue from consumables and services, which provides stability during slower equipment spending cycles.

Management has highlighted improving order trends in chromatography platforms and steady adoption of service contracts. These strengths help offset uneven demand in industrial and academic markets and reinforce the company’s ability to deliver consistent results through different phases of the industry cycle.

For investors, these dynamics support confidence in Waters long term resilience. While growth may not be rapid, the business offers a combination of stability, margin discipline, and steady demand drivers that help support predictable earnings.

Bear Case: Valuation and Industry Cycles

Waters still faces challenges that can limit its upside potential. The stock trades at a mid 20s forward P E multiple, which already assumes stable performance. With valuation near the higher end of its historical range, there is limited room for meaningful multiple expansion.

The analytical instruments industry also experiences spending cycles that can pressure growth. Reduced capital budgets in biopharma or weakness in industrial markets can slow equipment demand. Competition across chromatography and mass spectrometry platforms adds additional pricing and share pressure.

For investors, the concern is that Waters may continue operating well without generating strong stock returns. Unless revenue growth or margins improve beyond expectations, gains are likely to remain modest.

Outlook for 2027: What Could Waters Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model using a 26x forward P E suggests Waters could trade near $438/share by 2027. That represents roughly 11% total upside, or about 5% annualized returns.

This outlook reflects a company that grows consistently rather than aggressively. The forecast already incorporates mid single digit revenue growth and stable margins. To see more meaningful upside, Waters would need a stronger rebound in equipment demand or a clear acceleration in long term growth trends.

For investors, Waters offers dependable but limited upside potential. The stock’s return path will likely mirror the company’s steady fundamentals unless management delivers results above what analysts are currently projecting.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>