Danaher Corporation (NYSE: DHR) trades near $227/share, roughly flat over the past year as the company works through a slow recovery cycle. Growth has been soft, but Danaher’s strong margins and large recurring consumables base continue to support a steady long-term foundation.

Recently, management noted improving trends in its bioprocessing business and highlighted stronger sequential demand within key life sciences categories. The company has also made progress simplifying its portfolio after the Veralto spin-off, which has helped sharpen operational focus. New diagnostic product launches are contributing to more stable performance, suggesting Danaher may be slowly building momentum again.

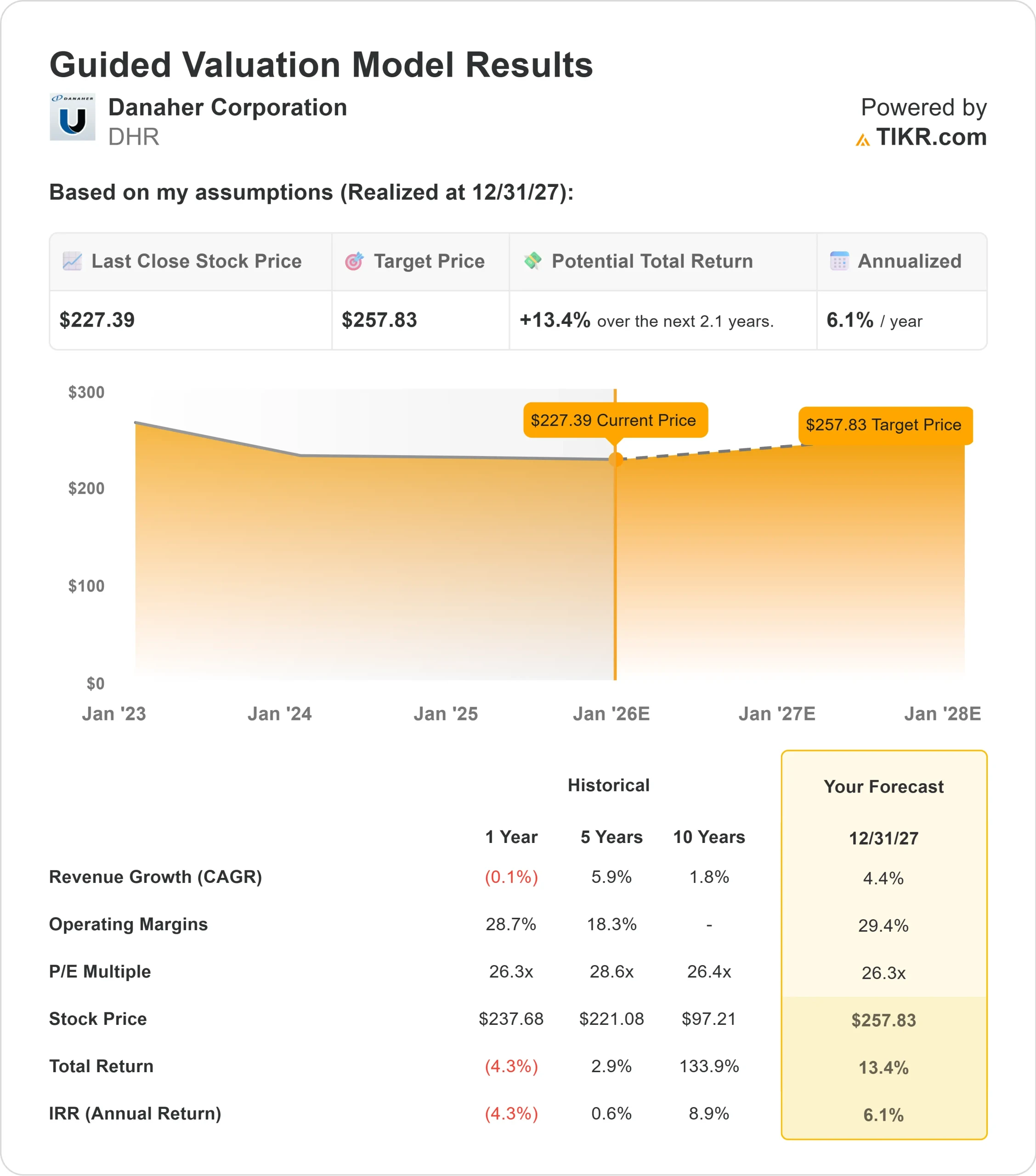

This article examines where analysts believe Danaher could trade by 2027. We used consensus forecasts and TIKR’s Guided Valuation Model to outline the potential path forward. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

Danaher trades at about $227/share today. Analysts see the stock trending toward an average price target of $254/share, which suggests around 12% upside. This places the stock firmly in the modest upside category.

- High estimate: $310/share

- Low estimate: $220/share

- Median target: $253/share

- Ratings: 17 Buys, 3 Outperforms, 3 Holds

For investors, this stable range signals that analysts largely agree on Danaher’s steady, measured outlook. Most of the expected gains come from consistent execution rather than aggressive growth. The stock is widely viewed as a reliable compounder with controlled risk.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

DHR: Growth Outlook and Valuation

Danaher’s fundamentals appear steady, supported by a large installed base and a meaningful mix of recurring consumables that help stabilize earnings through softer demand periods.

- Revenue growth forecast: 4.4%

- Operating margin forecast: 29.4%

- Forward P E used: 26.3x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 26.3x forward P E suggests Danaher could trade near $258/share by 12/31/27.

- That implies about 13% upside, or roughly 6% annualized returns.

These inputs point to a company that can continue compounding at a measured pace. The return profile is steady rather than aggressive, since growth expectations remain modest. For investors, Danaher looks like a consistent operator where predictable margins and recurring revenue support the model’s outlook, with additional upside possible if bioprocessing or diagnostics recover faster than expected.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Investors remain optimistic because Danaher’s business model is built around stability. A large portion of its revenue comes from consumables and services tied to its installed systems, which creates a recurring and predictable income stream. As management works to simplify the portfolio and strengthen core operating segments, execution has become more focused and disciplined.

New product activity in diagnostics and signs of improvement in bioprocessing also contribute to the more constructive outlook. These developments suggest the company is slowly regaining momentum while maintaining the quality and consistency that long-term investors value.

Bear Case: Slow Recovery and a Premium Valuation

The main concern is that Danaher’s growth recovery may take longer than expected. Recent years have shown meaningful declines across several performance metrics, reflecting softer demand in key markets. Although conditions are stabilizing, the recovery remains gradual and leaves limited room for surprises.

Valuation also poses a risk. At roughly 26x forward earnings, the stock trades at a premium that assumes improvement in both growth and operating performance. If demand trends remain slow, the market may hesitate to support further multiple expansion. For investors, this means the return potential could stay modest unless fundamentals improve at a faster pace.

Outlook for 2027: What Could Danaher Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model points to a value of about $258/share by 12/31/27. That equates to roughly 13% upside, or around 6% annualized returns from current levels.

This outlook suggests a steady return path, driven primarily by predictable earnings and stable margins. Stronger upside would require a more pronounced rebound in life sciences demand, increased contribution from new products, or broader improvement across Danaher’s operating segments.

For investors, Danaher remains a dependable long-term operator. The stock offers consistency, while the potential for stronger gains depends on growth improving beyond today’s conservative expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>