Anglo American (AAL) is in the middle of a major reset, with management calling 2025 a transition year, and the numbers support that view. Revenue fell 7 percent to 8.95 billion dollars as softer pricing and lower volumes in several divisions weighed on results. Underlying EBITDA dropped 20 percent to 2.96 billion dollars, driven by a steep decline at De Beers and lower copper output in Chile.

Despite the weaker earnings, the company delivered meaningful progress on cost control. EBITDA margins held at 32 percent, only slightly below last year’s 37 percent. Working capital releases lifted cash conversion to 108 percent, up from 93 percent a year ago. Free cash flow improved to 322 million dollars, a 69 percent year-over-year increase.

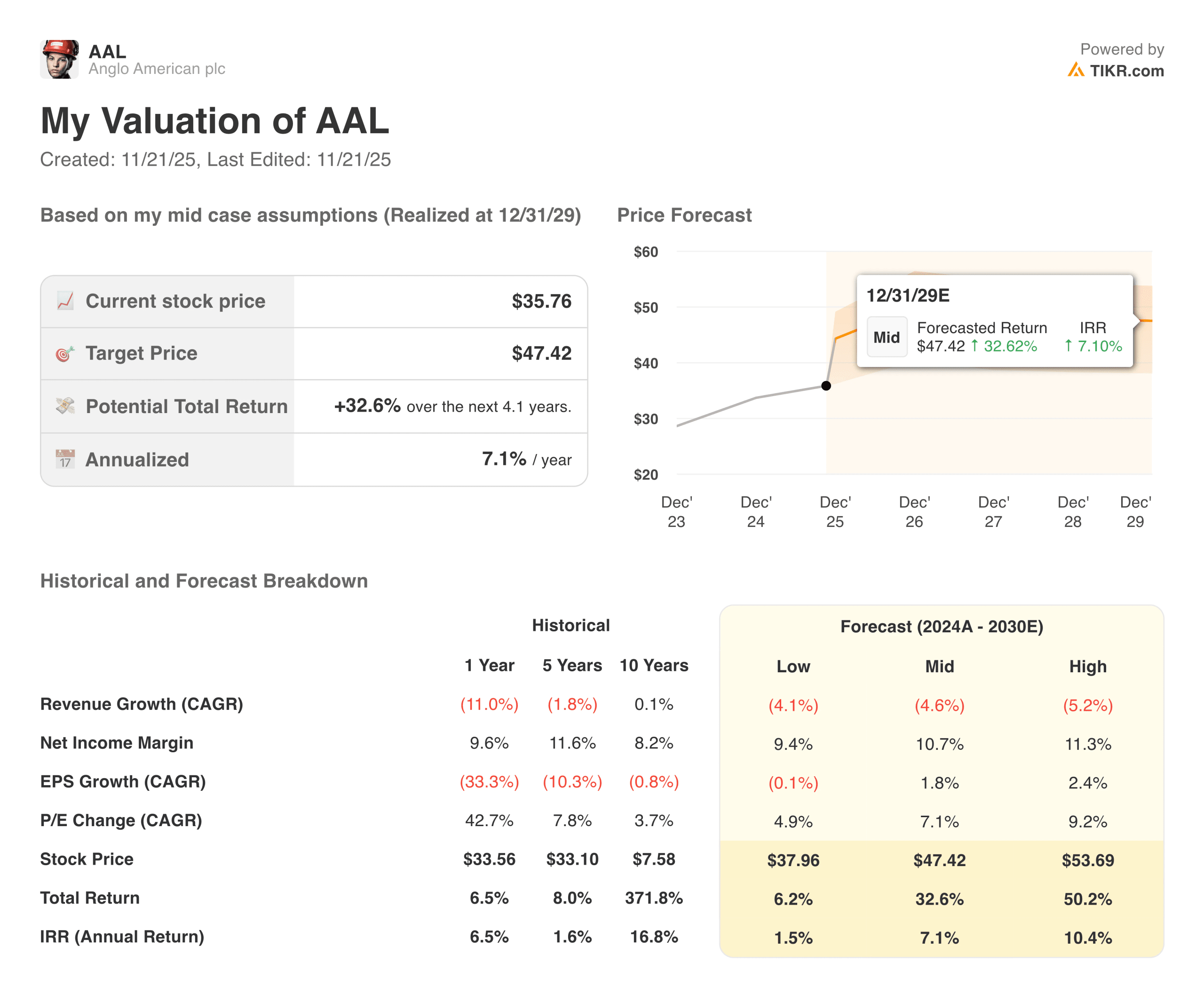

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The simplification plan is also taking shape. Anglo completed the demerger of Valterra Platinum, advanced planned sales in steelmaking coal and nickel, and moved further along in separating De Beers. Net debt ended the period at 10.8 billion dollars, flat year over year and roughly stable from last December.

Commodity exposures also remain highly diversified, as management is pushing toward a future mix in which copper accounts for more than 60 percent of EBITDA. The interim results reflect that strategy, with copper and iron ore providing most of the company’s profitability.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

The biggest earnings drag came from De Beers, as underlying EBITDA from diamonds swung from a $300 million profit to a $189 million loss. Copper EBITDA fell 14 percent as weaker grades and lower recoveries hit Chilean output. Iron ore stayed resilient, holding EBITDA roughly flat at 1.41 billion dollars.

| Metric | H1 2025 | H1 2024 | Change |

|---|---|---|---|

| Revenue | 8.95 bn | 9.61 bn | (7%) |

| Underlying EBITDA | 2.96 bn | 3.70 bn | (20%) |

| EBITDA Margin | 32% | 37% | (500 bps) |

| Underlying EPS | 0.32 | 0.71 | (55%) |

| Free Cash Flow | 322 m | 190 m | +69% |

| Capex | 1.59 bn | 2.13 bn | (25%) |

| Net Debt | 10.8 bn | 10.6 bn | flat |

| Dividend | 0.07 per share | 0.40 per share | lower |

Cash flow showed improvement. Capex fell to $1.59 billion from $2.13 billion, driven by lower sustaining and growth spending. Cash taxes also fell. These factors offset weaker operating cash flow, thereby pushing free cash flow higher.

The balance sheet remains stable. Net debt is roughly unchanged at $ 0.8 billion. Gearing sits at 29 percent. The net debt-to-EBITDA ratio increased to 1.8x due to the earnings decline, but management expects divestment proceeds to support deleveraging later in the year.

Look up Anglo American’s full financial results & estimates (It’s free) >>>

Broader Market Context

Anglo American’s half-year results reflect a mixed commodity landscape. Copper prices stabilized after last year’s softness, but operational constraints offset the benefit. Iron ore markets held firm, supported by stronger recovery rates at Minas-Rio. Diamonds faced persistent oversupply, high inventories, and weak midstream demand.

Capital markets focused on Anglo’s restructuring efforts. Investors want a simpler business with clearer cash generation. The demerger of Valterra Platinum and the pending sales of steelmaking coal and nickel signal real movement. The strategy aims to create a business anchored around copper, premium iron ore, and crop nutrients, all areas with multi-decade demand tailwinds.

For now, earnings volatility remains. Copper grades, De Beers pricing, and inflation all influence results more than management would like. That is why cost reductions, stronger discipline, and reduced project complexity remain the center of the plan.

1. Portfolio Simplification Is Reshaping the Company

Anglo American is pushing ahead with its plan to become a more focused business, and the pace of change has picked up through 2025. The company completed the Valterra Platinum demerger, which removed a major noncore operation and allowed management to redirect capital toward higher return segments. Work continues on potential exits in steelmaking, coal, and nickel, both of which would help simplify the group and reduce future capital demands. A possible separation of De Beers also remains on the table as the diamond market stays weak. The goal is a cleaner portfolio centered on copper, iron ore, and crop nutrients.

This shift matters because a simpler portfolio improves visibility on long-term earnings and cash flow. Management believes that reducing complexity will enhance operational execution and allow for more efficient capital allocation. Investors have been looking for signs that Anglo can narrow its focus after years of operating a broad mix of assets with uneven returns. Portfolio simplification supports stronger return profiles in the core businesses. It also gives the company more room to prioritize growth opportunities in markets with clearer demand trends.

2. Cost Discipline Strengthened Results

Anglo American leaned heavily on cost control during the first half, and the results helped offset weaker operating earnings. The company delivered roughly 300 million dollars in savings and remains on track to achieve about 500 million dollars by year’s end. These actions supported an EBITDA margin of 32 percent even as revenue declined. Working capital releases also lifted cash conversion to 108 percent. Together, these efforts helped the company maintain financial flexibility through a volatile period.

Lower capex contributed to stronger free cash flow, which rose to 322 million dollars despite the earnings decline. Management emphasized that cost discipline will stay at the center of near-term decisions as the company advances restructuring efforts. The strategy is to preserve cash while investing selectively in higher return projects. Investors have responded positively to the clearer focus on cash generation rather than broad expansion. This approach aims to create a foundation for steadier performance through 2026.

Value stocks like Anglo American in less than 60 seconds with TIKR (It’s free) >>>

3. Copper and Iron Ore Anchor the Business

Copper and iron ore remain the pillars of Anglo American’s earnings profile, and both divisions delivered meaningful contributions during the period. While copper volumes were softer due to constraints at certain mines, long-term demand remains supported by grid expansion and electrification markets. Iron ore continues to benefit from healthy pricing and stable operational performance. The company sees these two divisions as core assets with the potential for steady growth. They form the backbone of the simplified portfolio that management is building.

These businesses also carry stronger margins and more predictable demand patterns than some of the legacy segments that Anglo is unwinding. As the company reduces its exposure to diamonds and steelmaking coal, copper and iron ore will represent a larger share of returns. This shift helps reduce earnings volatility and aligns Anglo with long-term metals demand. Management expects that higher-quality assets will enhance group-level returns over time. The company plans to continue investing in productivity improvements and asset reliability across these units.

The TIKR Takeaway

Anglo American is navigating a complex transition, but the interim results show clear progress. Earnings are lower, but cost control, cash generation, and simplification steps created a more stable foundation. The portfolio is leaning toward copper and iron ore, and asset sales will strengthen the balance sheet. TIKR makes it easy to track these shifts through financials, margins, regional revenue splits, and segment EBITDA trends. The platform helps investors see how the company is evolving quarter by quarter.

Should You Buy, Sell, or Hold Anglo American’s Stock in 2025?

Anglo American is still in a transition period, with cost reductions, stronger cash conversion, and a stable balance sheet helping offset softer earnings. Copper and iron ore continue to provide reliable support, while the company moves forward on portfolio simplification at a steady pace.

Risks remain from weak diamond markets, operational challenges in Chile, and inflation pressures that influence unit costs. The long-term picture improves as the portfolio becomes more focused, but investors will need a few more reporting periods to judge how firmly the new strategy takes hold.

How Much Upside Does Anglo American Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!