Zimmer Biomet Holdings Inc. (NYSE: ZBH) has been under pressure as the stock trades near $89 after a challenging stretch for orthopedic device makers. Procedure volumes have stabilized, but growth has not accelerated enough to rebuild investor confidence. Even so, analysts expect gradual improvement as margins hold steady and valuation stays below historical norms.

Recently, Zimmer Biomet reported encouraging momentum across its knee and hip franchises while continuing to expand adoption of its ROSA robotics platform. The company also completed the ZimVie spinoff, which gives management a more focused portfolio and a clearer path to improving long term profitability. These developments show that ZBH is still reshaping its foundation even in a mixed medtech environment.

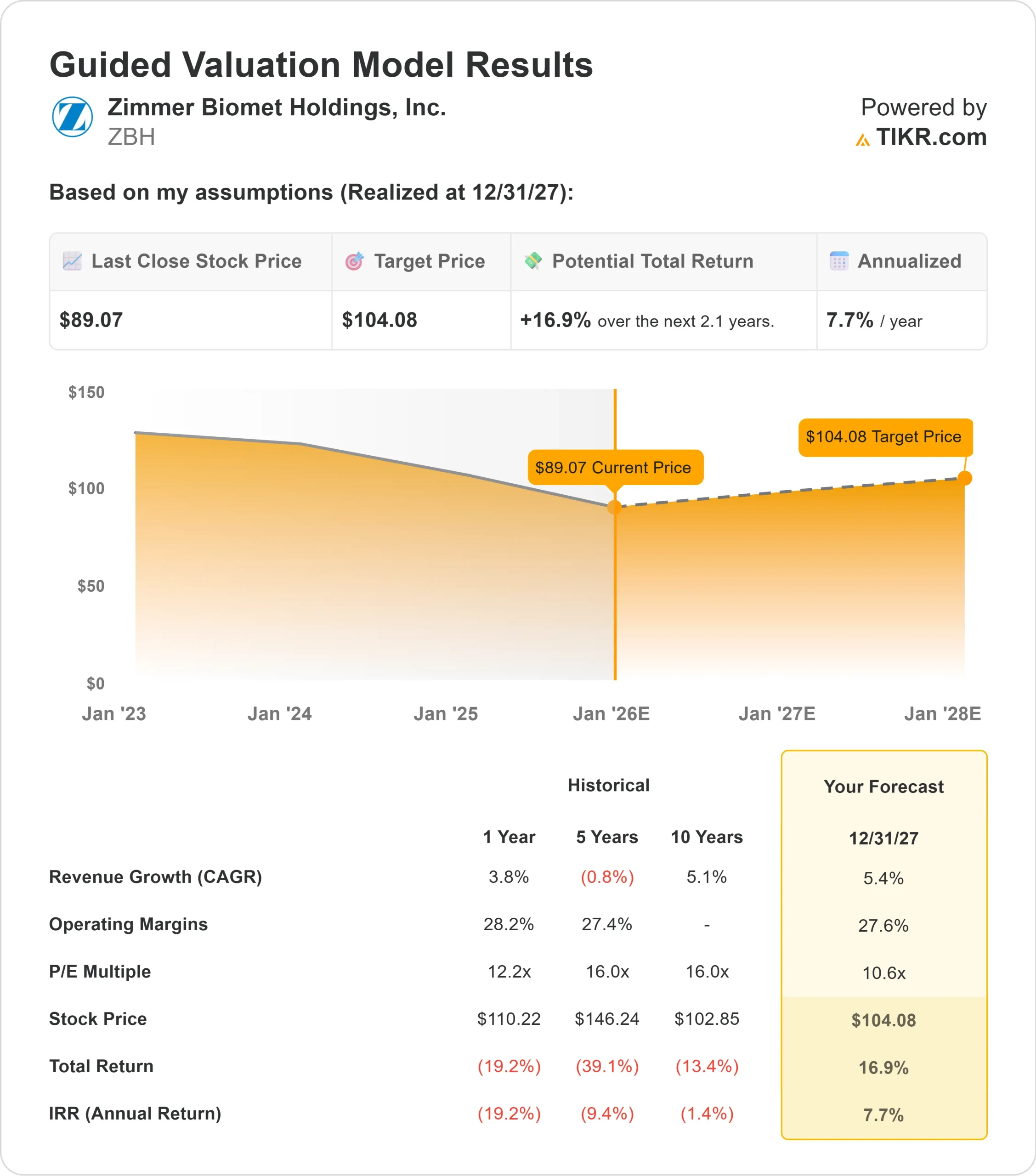

This article outlines where Wall Street expects ZBH to trade by 2027, using consensus price targets and TIKR’s Guided Valuation Model. These figures reflect analyst expectations and not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

ZBH trades around $89 per share today. The latest average analyst price target is $104, which implies about 16% upside. This places the stock in the modest upside category. Forecasts are tightly grouped, showing a steady consensus across analysts:

- High estimate: $130

- Low estimate: $88

- Median target: $100

- Ratings: 6 Buys, 4 Outperforms, 17 Holds, 1 Underperform, 1 Sell

The narrow spread between high and low targets suggests analysts expect the stock to move gradually rather than sharply. For investors, this level of upside means ZBH could outperform if execution improves or if procedure volumes strengthen, but expectations remain conservative.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

ZBH: Growth Outlook and Valuation

The company’s outlook appears steady based on the key inputs in the valuation model:

- Revenue is expected to grow about 5.4%

- Operating margins are forecast to hold near 27.6%

- Shares trade near 11x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11x forward P E suggests ZBH could trade near $104 per share by 2027

- That implies about 17% total upside, or roughly 8% annualized returns

These numbers point to stable compounding rather than rapid acceleration. The stock does not need fast growth for the model to work. For investors, the main appeal is valuation support. With the shares priced below their historical average multiple, much of the risk is already reflected in today’s price. Steady margins and predictable procedure volumes are enough to sustain the return path implied by the model.

The deeper takeaway is that ZBH functions as a consistency story instead of a high growth one. The valuation reflects stability more than excitement. If the company continues expanding its robotics presence and maintains reliable orthopedic demand, the stock could gradually re rate over time, but the current setup leans on dependable execution rather than big catalysts.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Zimmer Biomet continues to benefit from durable global demand for essential joint replacement procedures. Its presence in hips and knees remains strong, and the expanding ROSA robotics platform strengthens its competitive positioning. These drivers give the company a solid foundation that supports earnings stability even when industry growth slows.

Management’s ongoing focus on simplifying operations and improving its portfolio mix has also created a clearer path for margin expansion. For investors, these internal improvements suggest that ZBH is positioning itself for steadier long term performance and a more focused competitive strategy.

Bear Case: Slow Growth and Mixed Sentiment

Despite its strengths, ZBH still faces a slow growth profile. The company has struggled to produce meaningful revenue acceleration compared to faster growing medtech peers. This has kept investor sentiment cautious and prevented the stock from reclaiming a premium valuation.

Competition also remains intense. Orthopedic devices represent a crowded category with heavy innovation from other major players. For investors, the bear case centers on the risk that ZBH continues to grow slowly and lacks clear catalysts, which could leave the stock trading at a discount for longer than expected.

Outlook for 2027: What Could ZBH Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11x forward P E suggests Zimmer Biomet could trade near $104 per share by 2027. That represents about 17% upside or roughly 8% annualized returns.

While this outlook points to a steady recovery, it already assumes mid single digit growth and stable margins. To unlock stronger upside, ZBH would need clearer signs of accelerating procedure volumes or broader adoption of its ROSA robotics system. Without stronger catalysts, investors should expect solid but limited returns that reflect disciplined execution rather than high growth.

For investors, ZBH looks like a dependable medtech operator with manageable risks and a valuation cushion that offers downside protection. The potential for more meaningful gains depends on the company outperforming the cautious assumptions currently built into analyst models.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>