Medtronic plc (NYSE: MDT) has been navigating a period of slower growth and margin pressure. The stock trades near $99/share after a steady recovery through 2025. Demand across key device categories has remained stable, and analysts continue to view Medtronic as a dependable operator rather than a fast growth name.

Recently, Medtronic reported results that showed encouraging momentum. The diabetes segment improved after new system approvals, and the company made progress in expanding its surgical robotics platform. These developments suggest Medtronic is still capable of driving product led growth even as it operates in a competitive medical device landscape.

This article outlines where Wall Street analysts expect Medtronic to trade by 2028. We have pulled together consensus price targets and TIKR’s valuation model to map out the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

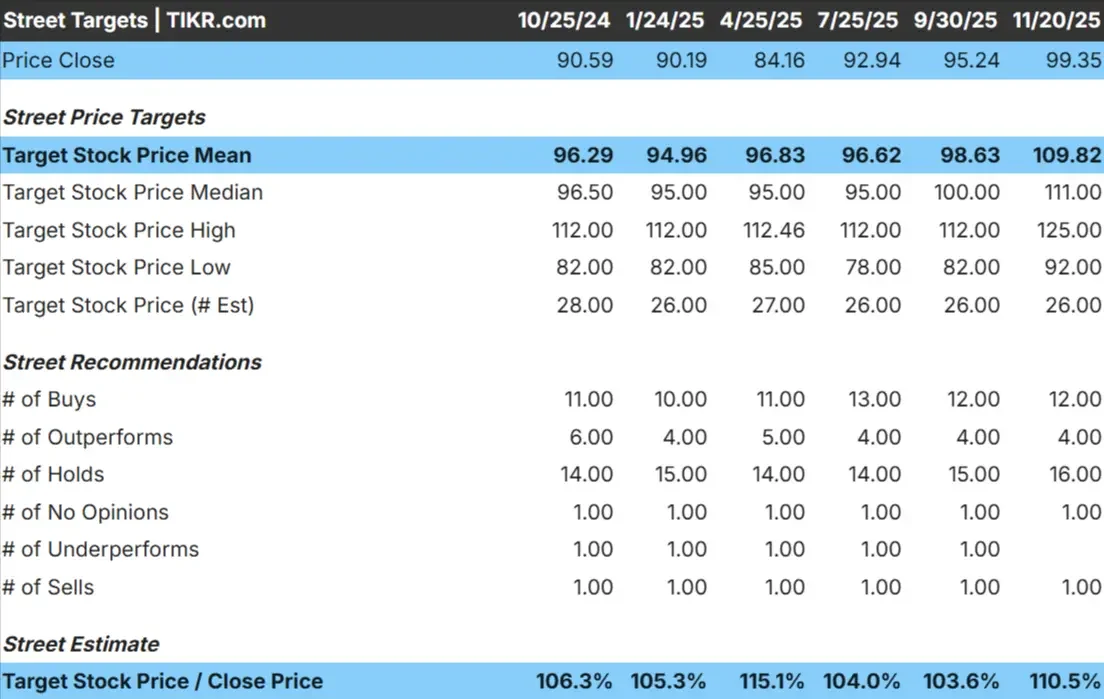

Medtronic trades near $99/share today. The latest average analyst price target is $110/share, which implies about 10% upside, placing the stock in the modest upside category.

- High estimate: $125/share

- Low estimate: $92/share

- Median target: $111/share

- Ratings: 12 Buys, 4 Outperforms, 16 Holds, 1 Sell

The tight spread between the high and low estimates suggests steady but cautious confidence. For investors, this points to a stock that can move gradually higher as long as execution remains consistent across core device categories. Upside could expand if adoption strengthens in diabetes technologies or surgical robotics.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Medtronic: Growth Outlook and Valuation

The company’s fundamentals appear steady, with expectations centered around consistent margins and dependable revenue trends:

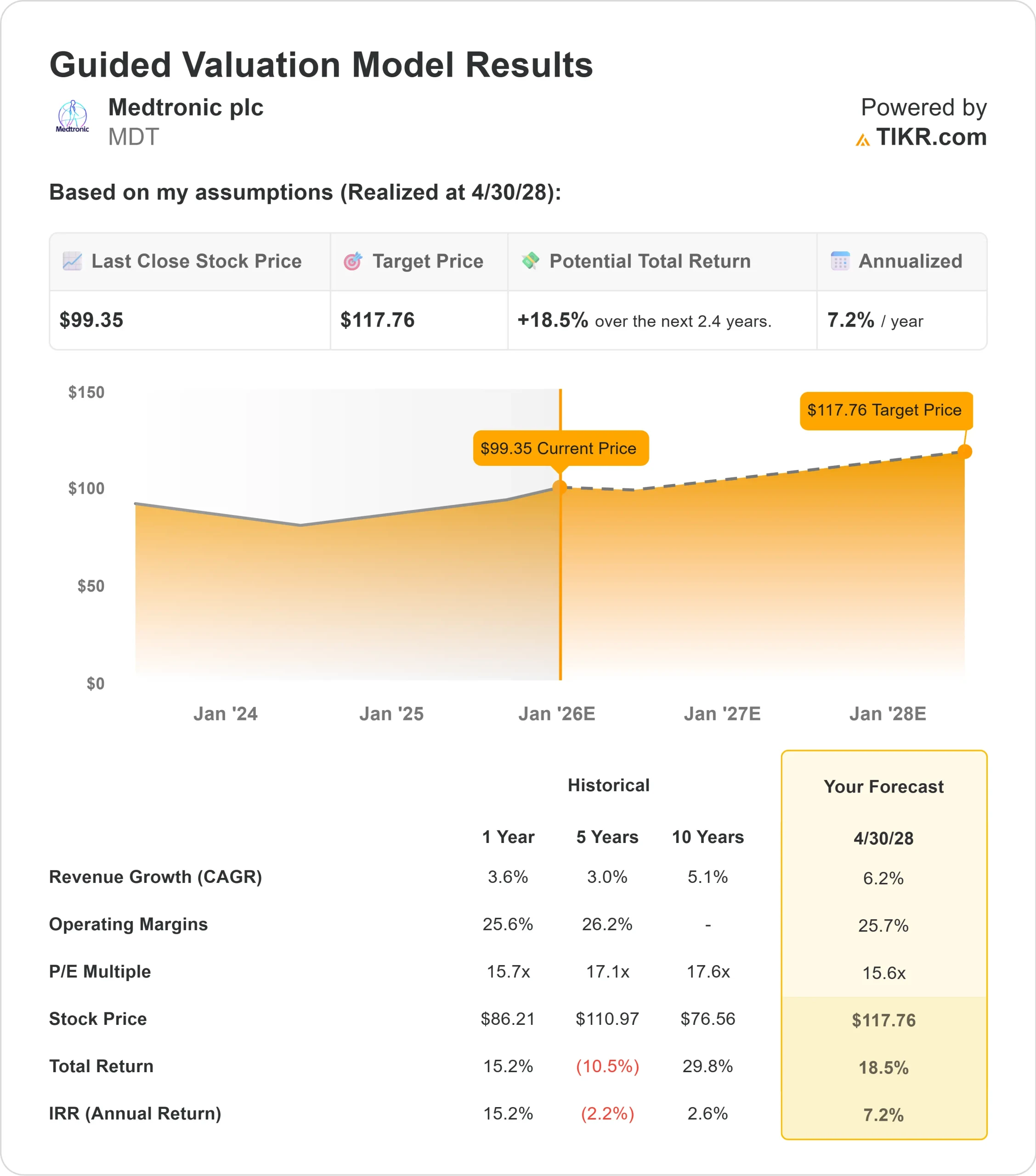

- Revenue is projected to grow 6.2%

- Operating margins are expected to hold near 25.7%

- Shares trade at about 15.6x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 15.6x forward P E suggests about $118/share by 2028

- That implies roughly 18.5% upside, or about 7.2% annualized returns

These numbers point to a modest but reliable compounding path. Medtronic does not need rapid growth for the stock to work, and stable margins support the current outlook. For investors, the setup suggests steady long term returns, with potential for stronger upside if product adoption or margin improvement exceeds expectations.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Medtronic’s global scale and broad device portfolio remain central strengths. Steady procedure activity across cardiac care, neuroscience, and surgical technologies helps support consistent revenue, while the improving performance of its diabetes segment has added a clearer path to growth.

Management’s continued focus on innovation and operational reliability also supports optimism. Progress in robotics and ongoing supply chain improvements suggest Medtronic is positioning itself for long term competitiveness. For investors, these factors reinforce the expectation of steady earnings and predictable compounding.

Bear Case: Growth and Competitive Pressure

Despite its strengths, Medtronic faces meaningful challenges. Growth remains slower than some faster moving peers, and competition is expanding across several therapeutic areas. Regulatory complexities can also create delays that slow momentum.

Companies like Abbott, Boston Scientific, and specialized device makers are increasingly active in overlapping markets. For investors, the concern is that Medtronic’s broad portfolio may not accelerate quickly enough to justify a major re rating. If execution slips or new products lag, returns may remain steady rather than strong.

Outlook for 2028: What Could Medtronic Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Medtronic could trade near $118/share by 2028.

That would represent about 18.5% total upside, or roughly 7.2% annualized returns.

While this outlook reflects a solid recovery, it assumes stable margins and mid single digit revenue growth. To unlock stronger upside, Medtronic would need to outperform in areas like diabetes system adoption, robotics expansion, and operational efficiency. Without that, investors should expect moderate but reliable returns.

For investors, Medtronic looks like a stable long term holding. The company can continue compounding through consistent execution, but outsized gains will depend on management exceeding today’s expectations.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>