Baxter International Inc. (NYSE: BAX) has been working through a difficult stretch. Revenue has declined, margins have tightened, and the stock trades near $17/share after a steep reset. The decline reflects weaker fundamentals across several divisions, but analysts still see potential for recovery as Baxter focuses on stabilizing operations and rebuilding profitability.

Recently, Baxter has continued moving forward with its restructuring plans, focusing on simplifying its operations, reducing debt, and tightening overall cost discipline. These efforts are intended to create a more stable and predictable earnings base over time. However, the company’s most recent results have been mixed and investor sentiment remains cautious. The stock has fallen sharply as revenue trends and earnings have yet to fully stabilize, and analysts are watching closely to see whether Baxter can translate its internal improvements into steadier financial performance.

This article breaks down where analysts expect Baxter to trade by 2027 using consensus Wall Street targets and TIKR’s valuation model. These figures reflect analyst expectations and are not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

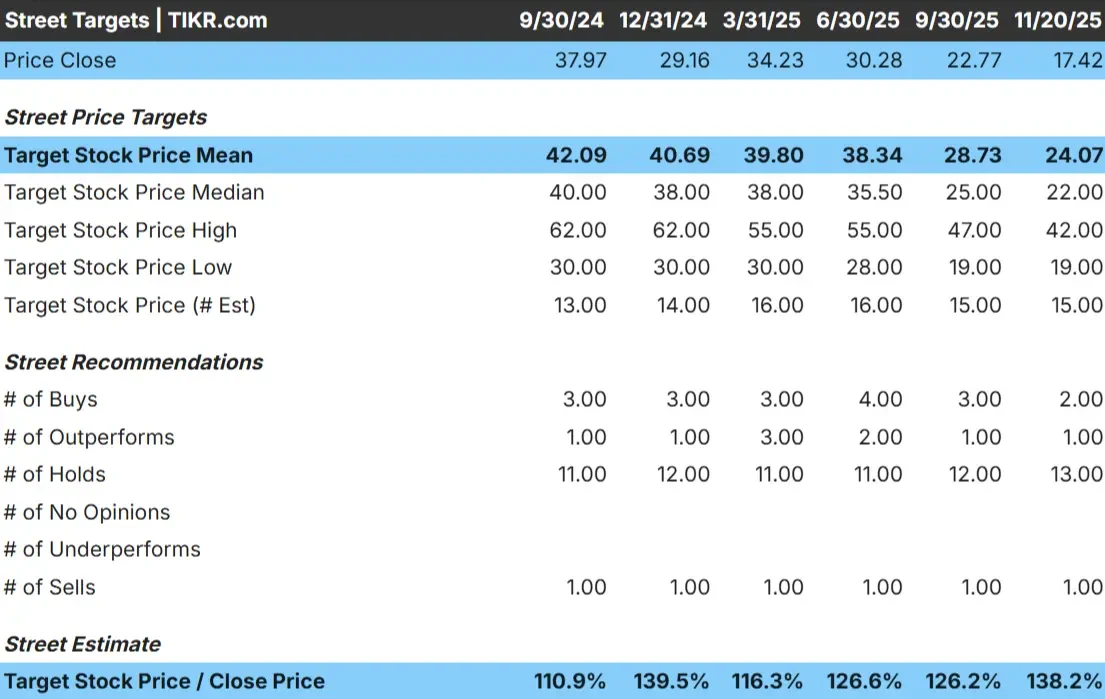

Baxter trades at about $17/share today. The latest analyst average price target is $24/share, which points to roughly 38% upside from current levels. This places Baxter in the meaningful upside category based on analyst expectations.

Key numbers from the target grid:

- High estimate: $42/share

- Low estimate: $19/share

- Median estimate: $22/share

- Ratings: 2 Buys, 1 Outperform, 13 Holds, 1 Sell

Analysts see room for recovery, although the wide spread between low and high estimates shows that conviction is still mixed. For investors, this suggests Baxter could rebound if profitability continues improving and the company maintains steadier execution. The cautious rating distribution also shows expectations remain conservative, but the valuation reset creates room for upside if the company stays on track.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Baxter Growth Outlook and Valuation

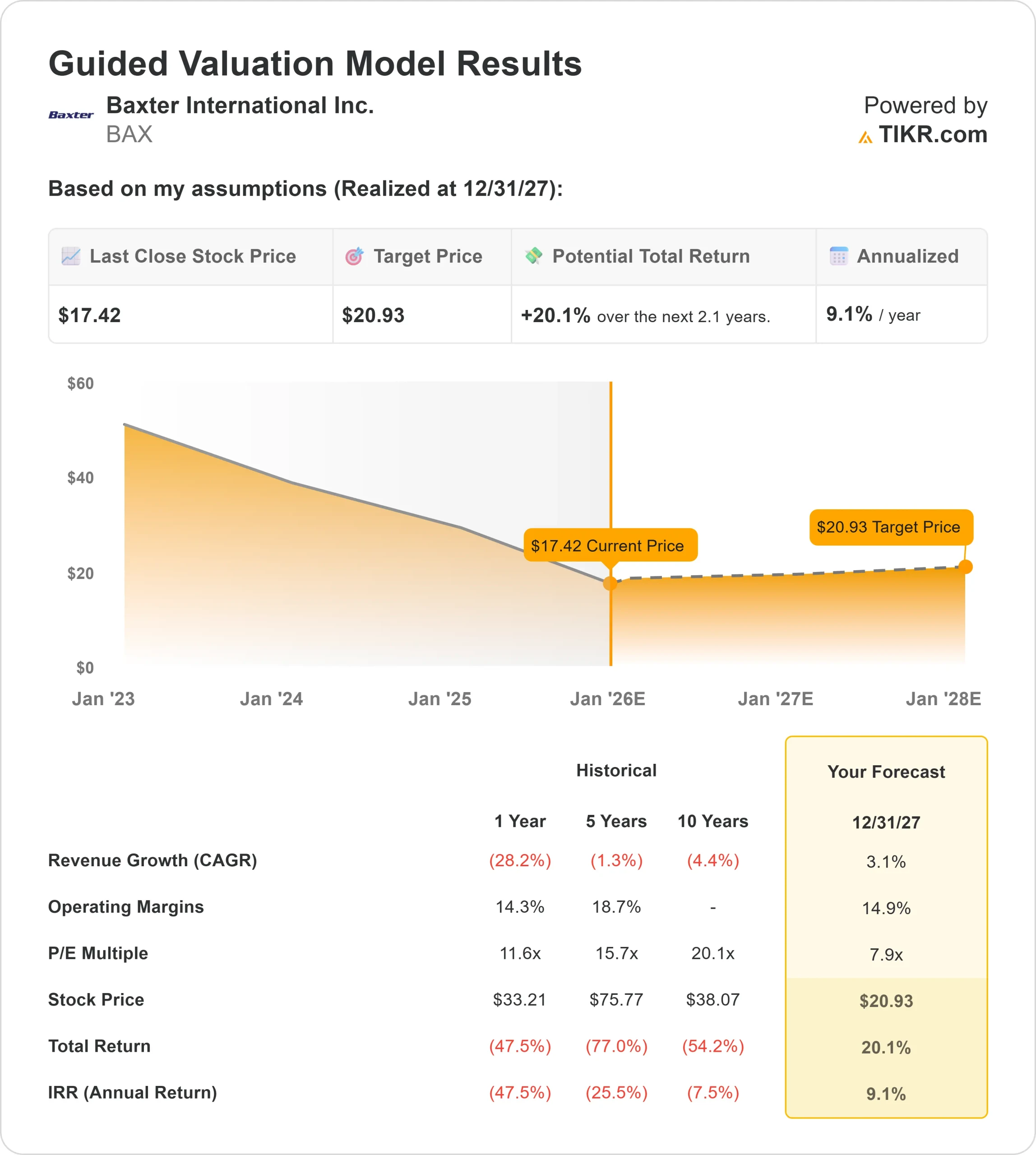

Baxter’s forward outlook points to a recovery that is steady, but not especially fast. The model inputs show a business that is slowly stabilizing rather than accelerating.

- Revenue growth forecast: 3.1%

- Operating margin expected: 14.9%

- Forward P E: 8x

- Last close: $17/share

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 8x forward P E suggests $21/share by 12/31/27

- That implies about 20% upside, or roughly 9% annualized returns

These numbers suggest Baxter can deliver consistent progress, but not rapid expansion. Most of the return potential comes from improving profitability and a valuation that sits well below historical levels. For investors, this means Baxter does not need strong growth for the stock to work. Stability in margins and earnings would be enough to support a gradual rerating.

For investors, Baxter screens as a steady recovery story. The path to upside depends on continued execution and maintaining a stronger earnings base rather than relying on aggressive revenue growth.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Despite recent challenges, analysts still see reasons to be constructive. Baxter has placed strong emphasis on operational discipline, simplifying its portfolio, and reinforcing the areas of the business that generate more reliable cash flow. This shift helps the company build a more stable financial foundation after years of inconsistent performance.

The company is also working to strengthen its balance sheet, which has been a key concern for investors. As financial pressure eases, Baxter gains more flexibility to invest in higher quality opportunities and focus on product categories that support long term profitability. For investors, these steps show the company is moving in the right direction and rebuilding confidence in its future earnings potential.

Bear Case: Weak Growth and Execution Risk

Even with improving trends, Baxter still faces meaningful risks. Growth expectations across the company remain soft, and several product segments have struggled to generate consistent demand. This creates uncertainty around how quickly Baxter can reestablish reliable top line momentum.

There is also execution risk. The company has undergone significant internal changes, and maintaining operational stability will be essential. If Baxter struggles to sustain margin improvement or fails to deliver steady results, the current valuation discount could persist.

For investors, the bear case centers on whether Baxter can maintain progress without slipping back into inconsistent performance.

Outlook for 2027: What Could Baxter Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Baxter could trade near $21/share by 12/31/27. That represents about 20% upside, or roughly 9% annualized returns.

While this outlook signals a steady recovery, it assumes that Baxter continues improving margins and maintaining financial discipline. Stronger upside would likely require clearer product momentum, more consistent growth across divisions, or faster progress on portfolio optimization.

For investors, Baxter screens as a reasonable long term hold with valuation driven upside. The path to stronger returns depends on consistent execution and continued strengthening of its earnings base.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>