DaVita Inc. (NYSE: DVA) has been under pressure over the past year. Shares trade near $115/share, down roughly 30%, as cost inflation, labor challenges, and slower reimbursement growth weighed on sentiment. Even with the pullback, DaVita remains a durable operator supported by steady patient volumes and recurring cash flow.

Recently, DaVita signaled early progress after reporting better than expected operating trends and more stable labor expenses, one of the biggest concerns facing healthcare operators. The company is also expanding its value based care initiatives, which aim to improve patient outcomes while lowering total care costs. These developments suggest DaVita may be gaining momentum even as the broader healthcare landscape remains challenging.

This article explores where Wall Street analysts believe DaVita could trade by 2027. We pulled together consensus price targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

DaVita trades around $115/share today, and analysts see modest room for the stock to recover. The latest average analyst price target is $145/share, which implies about 26% upside. The range of estimates remains wide, highlighting uncertainty around how quickly business conditions will improve:

- High estimate: $186/share

- Low estimate: $126/share

- Median target: $143/share

- Ratings: 1 Buy, 7 Holds, 1 Underperform

For investors, 26% upside places DaVita in the modest upside category. The stock could outperform if margins continue stabilizing and cost pressures ease, but the wide spread between targets shows that analysts are still cautious. Any recovery is likely to be steady rather than dramatic.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

DaVita: Growth Outlook and Valuation

DaVita’s fundamentals appear steady, supported by stable patient demand and consistent profitability. The valuation model highlights how most of the expected return comes from earnings stability and a discounted valuation multiple rather than high growth.

- Revenue is forecast to grow 4.2% through 2027

- Operating margins are expected to remain near 15.4%

- Shares trade at 9.5x forward earnings, below historical levels

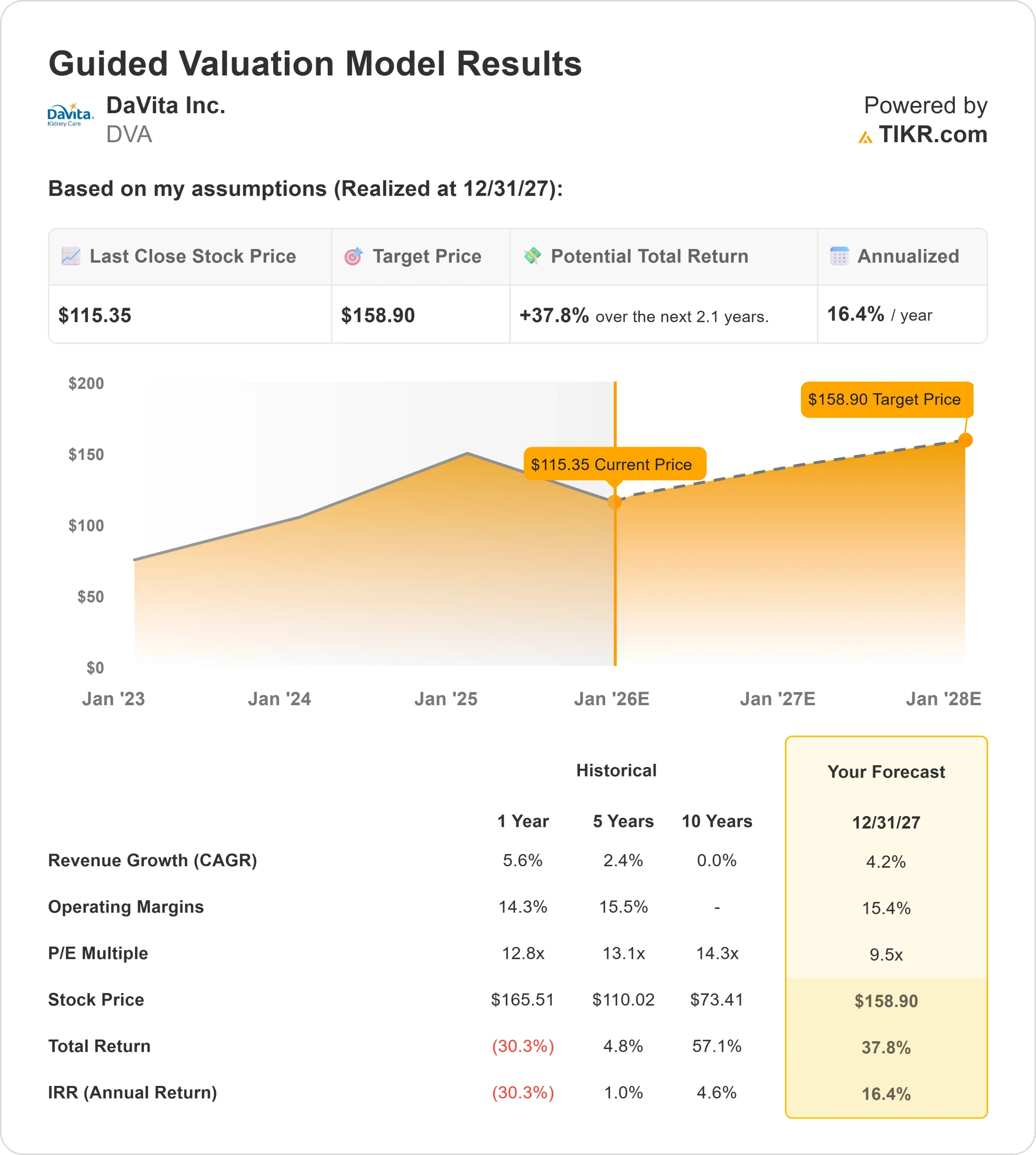

- Based on analysts average estimates, TIKR’s Guided Valuation Model suggests about $159/share by 12 31 27

- That implies 38% upside, or roughly 16% annualized returns

These numbers suggest DaVita can deliver meaningful returns even without strong growth. The stock looks reasonably valued for a company with recurring demand and improving cost visibility.

For investors, DaVita is more of a steady compounder than a fast grower. The investment case relies on stable margins, predictable patient volumes, and disciplined cost management. If the company maintains this consistency, investors could see solid long term results supported by both earnings and valuation recovery.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

DaVita benefits from a business model built on predictable patient demand and a long track record of operational reliability. Patient volumes have remained stable, and the company has improved its operating discipline after a tough period marked by rising costs. This stability helps maintain investor confidence during uncertain industry conditions.

Management’s investment in value based care programs further supports the long term thesis. These initiatives aim to improve outcomes while reducing total care costs, which could enhance DaVita’s positioning in kidney care. For investors, the combination of recurring demand and gradually improving cost visibility supports a constructive outlook.

Bear Case: Regulation and Cost Pressures

Despite recent progress, DaVita still faces important risks. Reimbursement increases tend to lag inflation, which limits earnings flexibility when costs rise. Labor expenses, although improving, remain elevated relative to historical levels. The company also carries higher leverage than many healthcare peers, which adds risk if industry conditions weaken.

Regulatory oversight and evolving care models introduce additional uncertainty. For investors, these factors mean that while the upside is meaningful, it is not guaranteed. Market sentiment can shift quickly if reimbursement expectations soften or if cost visibility deteriorates again.

Outlook for 2027: What Could DaVita Be Worth?

Based on analysts average estimates, TIKR’s Guided Valuation Model suggests DaVita could trade near $159/share by 12 31 27. This would represent about 38% upside, or roughly 16% annualized returns. This outlook assumes stable demand, consistent margins, and a return to a more typical valuation range.

While this would be a solid recovery, it already assumes progress in cost stability. To generate even stronger upside, DaVita would likely need smoother reimbursement trends and continued success in its value based care efforts. Without these drivers, investors should expect steady and measured performance.

For investors, DaVita appears to be a dependable long term operator with room for meaningful upside as the business environment normalizes. The investment case centers on stability, disciplined execution, and durable cash generation.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>