Universal Health Services (NYSE: UHS) has been one of the steadier performers in the healthcare sector, with the stock now trading around $229 per share after a solid run throughout the year. Strong execution, stable patient volumes, and improving operational efficiency have supported the company’s climb, although analysts remain measured in their expectations from here.

Recently, UHS highlighted improving forward growth trends, including a recovery in its behavioral health business and better visibility on reimbursement. These developments have helped rebuild confidence in the company’s long term earnings outlook and suggest that UHS is gradually strengthening its financial foundation after a challenging few years.

This article breaks down where Wall Street analysts believe UHS could trade by 2027. We review consensus targets and valuation models to map out the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

UHS trades at about $229 per share today. The latest analyst average price target sits near $249 per share, which suggests roughly 9% upside. That places UHS in the modest upside category.

Key details from analyst estimates:

- High estimate: $302 per share

- Low estimate: $190 per share

- Median target: $251 per share

- Ratings: 7 Buys, 2 Outperforms, 9 Holds, 1 Underperform

For investors, these targets show that analysts expect UHS to continue performing well, but they are not calling for a major rerating. The spread between the high and low estimates highlights mixed conviction. The stock’s next move will depend on whether UHS can sustain its margin performance and patient volumes in the quarters ahead.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

UHS Growth Outlook and Valuation

The company’s fundamentals appear steady, supported by balanced expectations for revenue growth and profitability over the next few years.

- Revenue is forecast to grow about 6.6% through 2027

- Operating margins are expected to hold near 11.4%

- Shares currently trade around 9.5x forward earnings

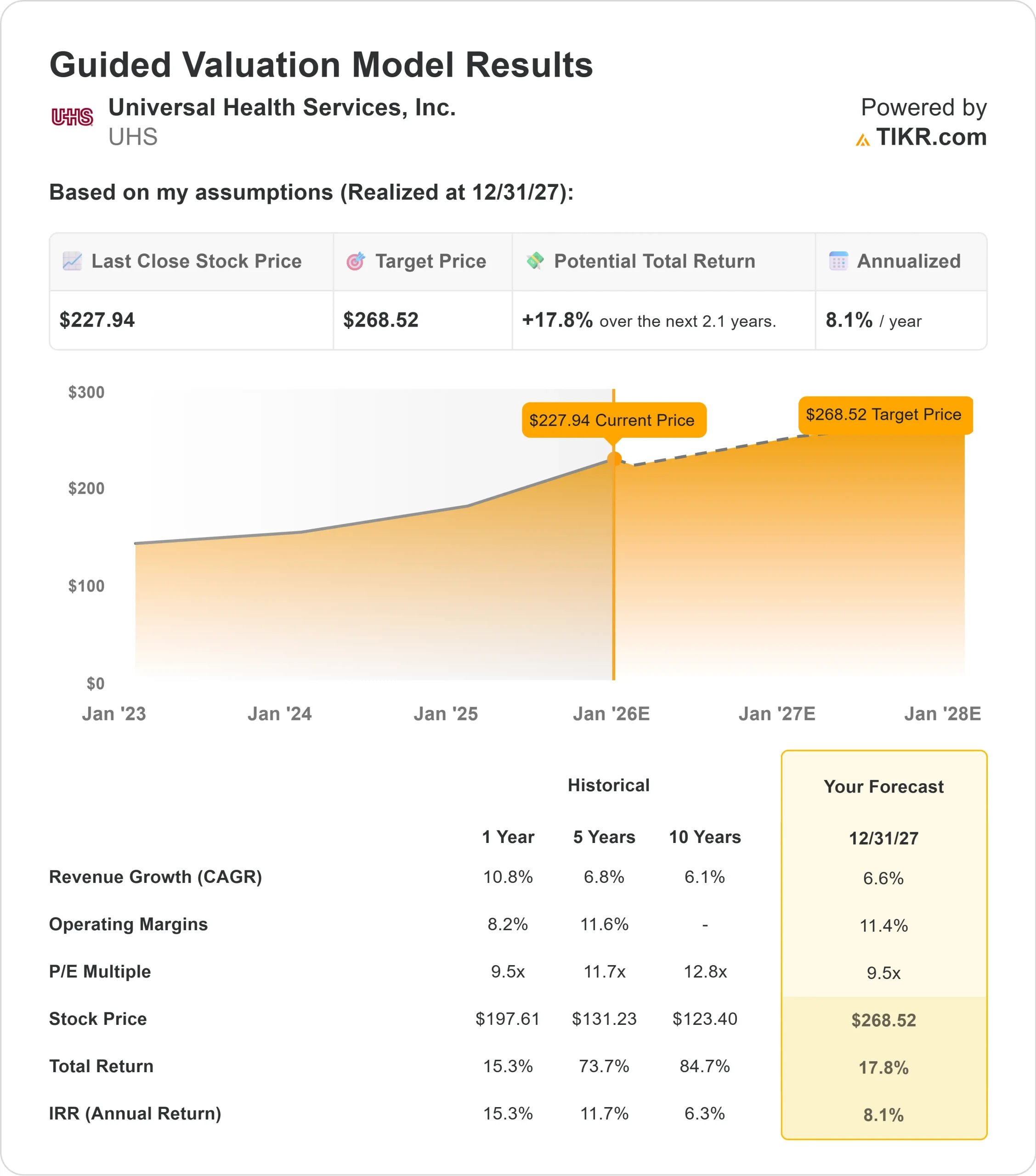

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 9.5x forward P E suggests about $269 per share by 12/31/27

- That implies roughly 18% total upside, or about 8.1% annualized returns

These numbers point to steady compounding rather than aggressive growth. The valuation looks reasonable given the company’s margin profile, and the model reflects a scenario where UHS simply maintains its current level of execution.

For investors, UHS appears to be a stable operator with a clear path to consistent returns. The upside is driven by predictable earnings and disciplined cost management rather than high growth expectations.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts see several factors supporting UHS over the next few years. The company continues to benefit from healthy demand trends, particularly in its behavioral health segment, where patient activity and reimbursement outlooks have been improving. Operational discipline has also helped stabilize performance and strengthen overall earnings quality.

The balance sheet remains in good shape, giving UHS flexibility to invest in service expansion and staffing improvements where needed. For investors, these strengths suggest UHS has a durable foundation that can support steady results even without aggressive growth.

Bear Case: Valuation and Operating Risks

Despite its strengths, UHS faces risks that could limit its upside. The stock already trades near what many analysts consider a fair valuation, which makes significant multiple expansion less likely. The business also remains exposed to industry wide pressures such as labor costs, staffing shortages, and shifts in reimbursement conditions.

The wide range between analyst targets reflects this uncertainty. Some believe UHS can continue to strengthen margins, while others worry that the recovery in behavioral health may not be smooth. For investors, the risk is that UHS may already reflect much of its progress, leaving less room for surprise upside.

Outlook for 2027: What Could UHS Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests UHS could trade near $269 per share by 12/31/27. That would represent about 18% upside from today or roughly 8.1% annualized returns.

This outlook assumes UHS continues to execute well and maintains its current profitability profile. For investors, UHS offers a steady long term story. The stock may not deliver dramatic gains, but it provides consistent margins, reliable cash flow, and a valuation that supports predictable compounding through 2027.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>