HCA Healthcare, Inc. (NYSE: HCA) has been performing well, with shares trading near $481 after a strong year supported by steady patient volumes and consistent profitability. The stock has benefited from stable demand across its hospital network and disciplined cost management. Investors are now asking how much upside is left after such a strong run.

Recently, HCA delivered another steady quarter with healthy same-facility admissions growth and improving labor efficiency. The company also continued to expand its outpatient footprint and invest in new service lines, reinforcing confidence in long term demand. These developments show that HCA is still executing well even as the broader healthcare sector navigates rising costs and tighter operating conditions.

This article explores where Wall Street analysts think HCA could trade by 2027. We use consensus targets and valuation models to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Almost No Upside

HCA trades near $481/share today. The latest analyst average price target is $478/share, which signals essentially 0% upside from here. Forecasts span a wide range, showing steady but cautious sentiment among analysts.

Street expectations:

- High estimate: $525/share

- Low estimate: $368/share

- Median target: $492/share

- Ratings: 13 Buys, 1 Outperform, 9 Holds, 1 Underperform

Analysts still view HCA as a high quality operator, but most believe recent performance is already reflected in the current price. The gains from improving labor trends, resilient patient volumes, and stable margins appear largely priced in. For investors, there is no clear valuation gap to close. Upside from here would need to come from better than expected earnings growth or stronger reimbursement visibility.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

HCA Growth Outlook and Valuation

HCA’s long term fundamentals appear steady. Growth is not especially fast, but the company continues to produce reliable earnings supported by consistent patient volumes and disciplined cost management.

Key inputs from TIKR’s Guided Valuation Model:

- Revenue is projected to grow 5.6%

- Operating margins are expected to remain near 15.6%

- Shares trade at roughly 14x forward earnings

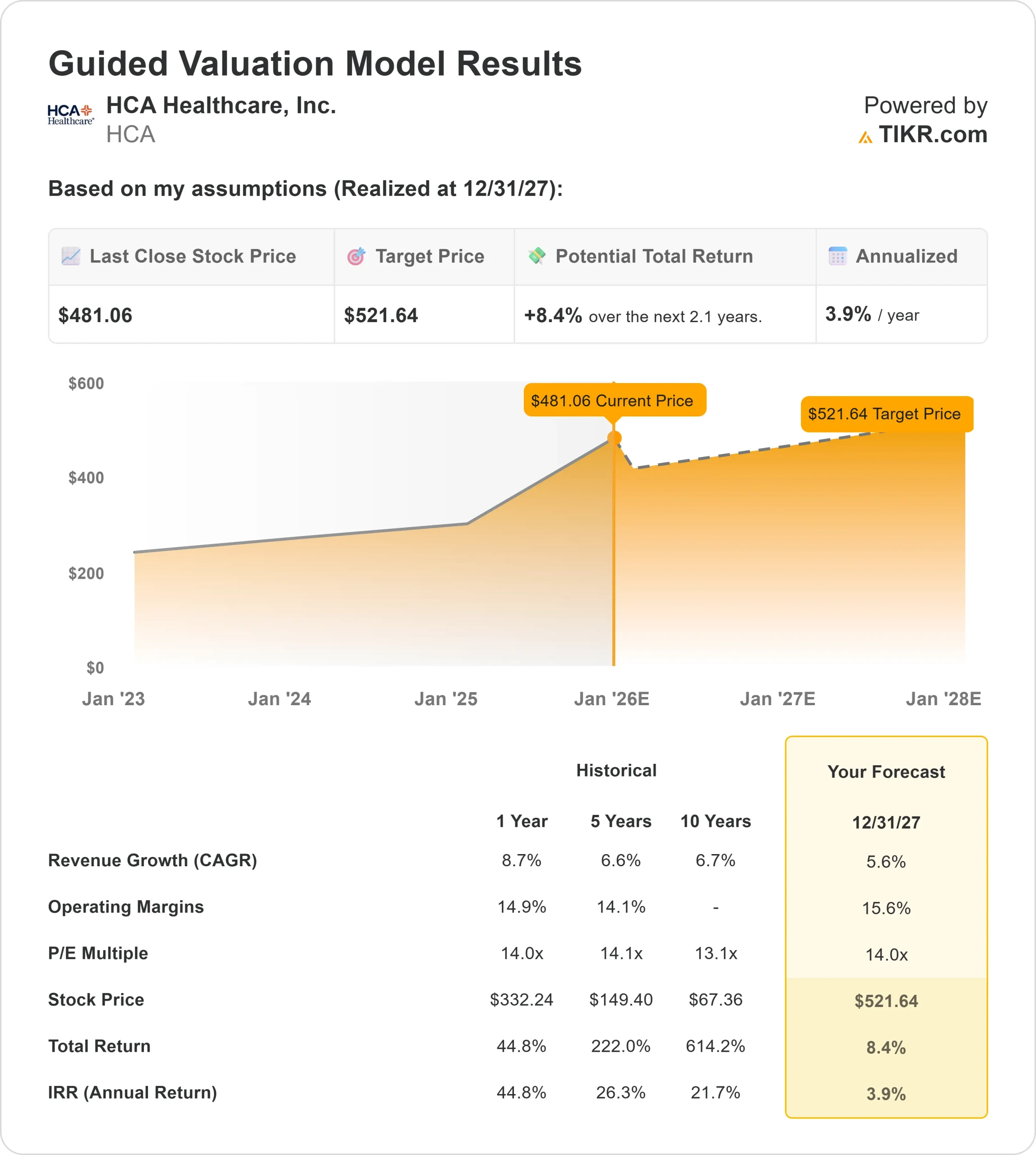

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 14x forward P E suggests about $522/share by 2027

- That implies about 8.4% total return, or roughly 3.9% annualized

These numbers point to slow but steady compounding rather than high growth. The valuation suggests that HCA can continue delivering consistent earnings, although upside may remain limited unless margins improve more meaningfully.

For Investors, HCA looks like a stable, dependable operator with a resilient earnings base. Returns are likely to be moderate, driven by consistency rather than rapid acceleration. The stock favors predictability, but offers limited room for a major re-rating unless performance exceeds current expectations.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

HCA continues to execute well across its operations. Patient volumes remain steady, and management has improved staffing efficiency despite elevated labor pressures across the industry. The company has also been expanding its outpatient network and building out service lines that enhance long term growth potential.

These strategic investments help diversify revenue and create a more stable operating environment. For investors, these strengths highlight HCA’s ability to maintain performance even when broader healthcare conditions are challenging.

Bear Case: Limited Valuation Upside

Despite its strengths, HCA faces valuation constraints. With shares already near their 52 week high of $484, much of the improvement in margins and volumes appears reflected in the current price.

The hospital sector continues to deal with rising labor costs, slower reimbursement growth, and persistent regulatory uncertainty. These pressures make significant multiple expansion unlikely in the near term. For investors, the concern is not HCA’s execution, but whether the stock already reflects most of its near term potential.

Outlook for 2027: What Could HCA Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests HCA could trade near $522/share by 2027. That represents about 8.4% total return, or roughly 3.9% annualized.

While the outlook reflects stability, it does not point to a major re-rating. The valuation model already assumes steady margins and consistent volume growth. To generate stronger upside, HCA would need to deliver better than expected earnings growth or improved operating leverage.

For investors, the takeaway is clear. HCA remains a reliable long term operator with consistent fundamentals, but returns from today’s price may be modest. The stock favors stability and disciplined execution rather than high growth or significant valuation upside.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>