UnitedHealth Group (NYSE: UNH) has been under significant pressure over the past year. Shares trade near $308 and are down 46%. Higher medical costs and weaker Medicare Advantage margins have weighed on results. Even with sentiment shaken, UNH remains one of the most important companies in U.S. healthcare, and analysts are watching closely for signs of stabilization.

Recently, UnitedHealth reported another quarter of steady revenue growth and highlighted improvements in care delivery and claims processing across its Optum segment. The company also introduced updated medical cost management initiatives aimed at reducing unnecessary utilization. Analysts view these steps as early signs that cost discipline is returning after a difficult period.

This article reviews where Wall Street analysts expect UNH to trade by 2027 based on consensus targets and TIKR’s Guided Valuation Model. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

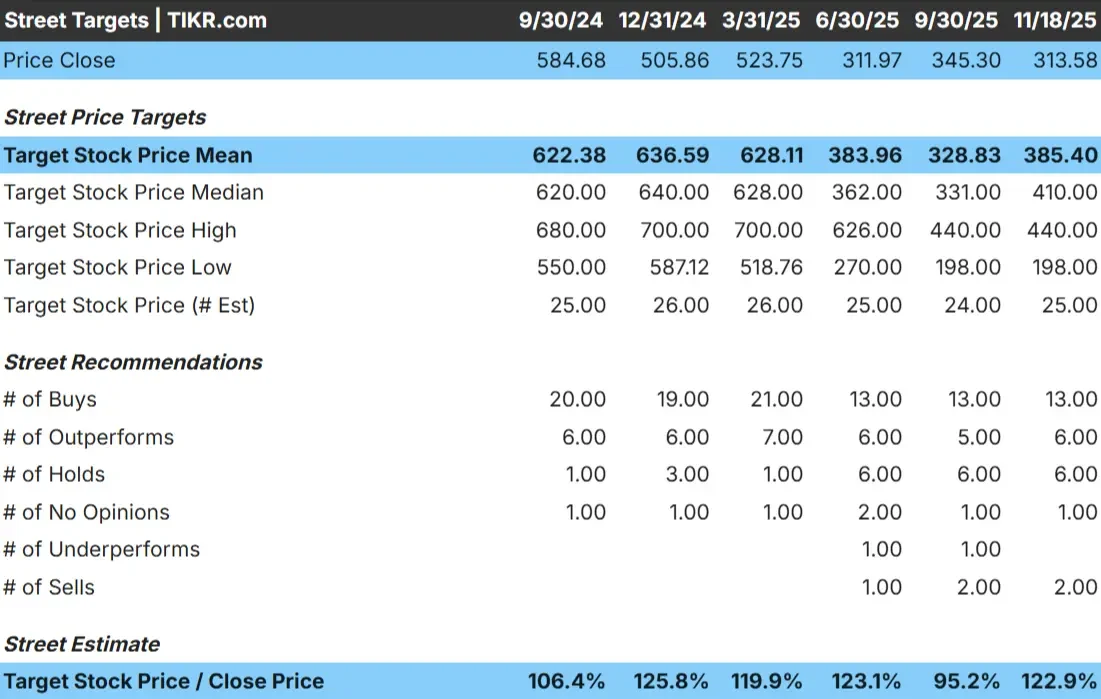

UNH trades around $308/share today. The average analyst price target is $385/share, which points to about 25% upside based on current estimates.

- High estimate: ~$440/share

- Low estimate: ~$198/share

- Median estimate: ~$410/share

- Ratings: 13 Buys, 6 Outperforms, 6 Holds, 1 Underperform, 2 Sells

Analysts see room for the stock to rebound, but the wide range between estimates shows that confidence is still mixed. For investors, the next phase of upside depends on improving medical cost trends and clearer signs that margins are stabilizing. A shift in these areas could support meaningful recovery potential.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

UNH: Growth Outlook and Valuation

The company’s fundamentals appear steady, supported by consistent revenue growth and a more conservative margin profile:

- Revenue is expected to grow 6.2%

- Operating margins are forecast at 5.6%

- Shares trade at a forward P E of 17.4x

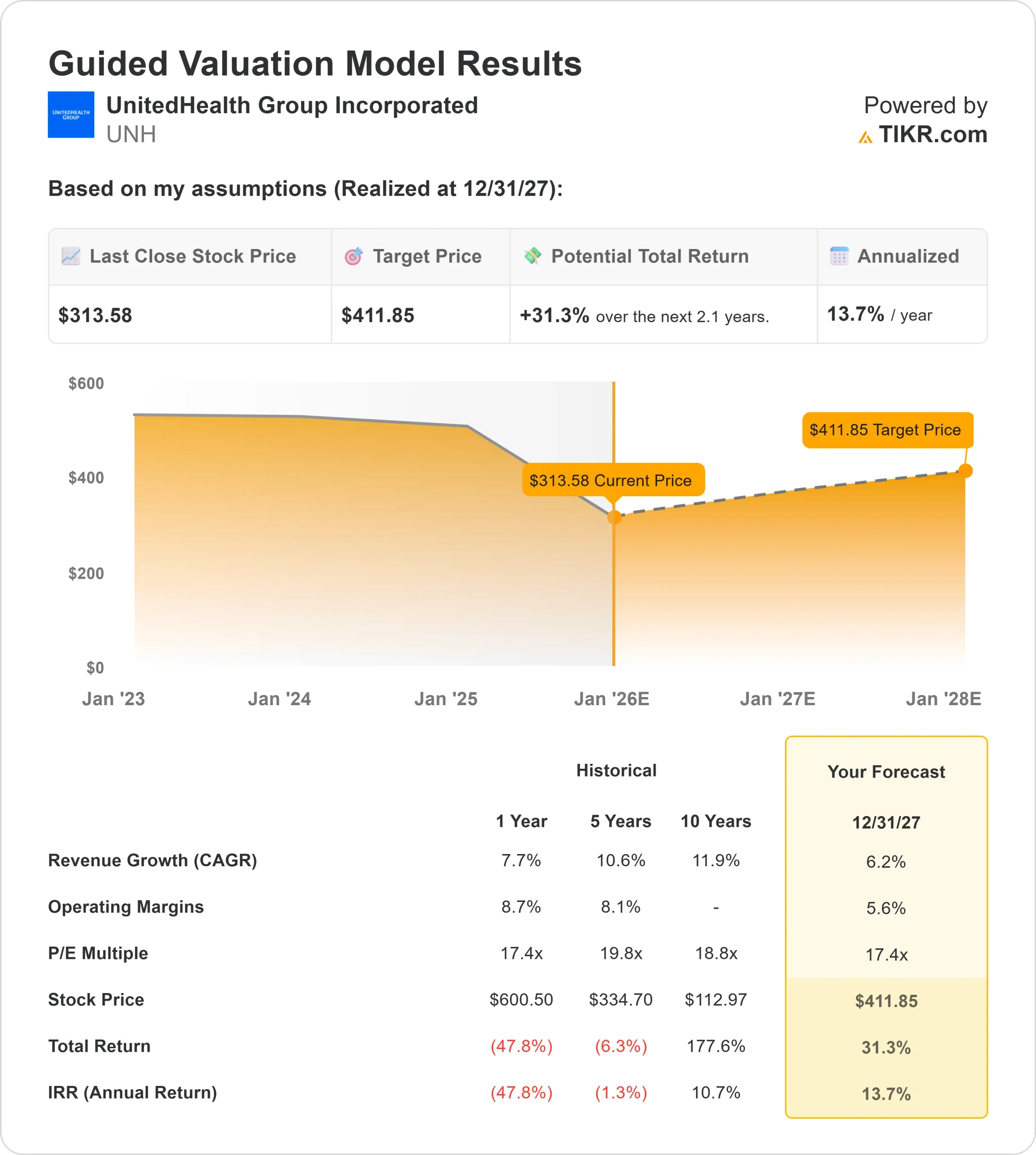

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 17.4x forward P E suggests about $412 by 2027

- That implies 31.3% upside, or roughly 14% annualized returns

These figures point to a stable long term compounding profile rather than a rapid recovery. For investors, UNH looks like a solid large cap healthcare stock with a clear path to improvement as medical cost pressures ease. The potential upside depends on steady execution and better cost discipline across core operations rather than aggressive growth.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Several factors support the long term optimism surrounding UNH. The company benefits from a diversified business model that spans insurance, Optum services, pharmacy benefits, and care delivery. This structure provides stability and reduces reliance on any single segment.

UnitedHealth is also working to improve operational efficiency. Enhancements in care coordination, integration across Optum, and advances in claims processing help counter elevated medical costs. Over time, these improvements can strengthen profitability and support more predictable results.

For investors, these advantages signal that UNH is positioned to regain momentum as cost pressures ease.

Bear Case: Margin Pressure and Regulatory Risk

The biggest concern for UNH remains margin pressure. Elevated utilization and reimbursement challenges within Medicare Advantage create ongoing headwinds. If these trends persist longer than expected, earnings growth may remain limited.

Regulatory uncertainty adds another layer of complexity. Changes in healthcare policy, reimbursement rules, and compliance requirements can impact financial performance and slow margin recovery.

For investors, the bear case centers on timing. UNH’s fundamentals are strong, but a slower path to normalization could keep sentiment cautious.

Outlook for 2027: What Could UNH Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 17.4x forward P E suggests UNH could reach about $412 by 2027. That represents roughly 31% upside and about 14% annualized returns.

This scenario assumes steady revenue growth and a gradual recovery in margins as medical cost trends normalize. It does not depend on aggressive performance, which makes the upside appear achievable if the company continues to execute well.

For investors, UNH offers an appealing mix of stability and potential upside after a sharp reset. The long term fundamentals remain intact, the valuation is more reasonable, and the path to recovery appears clearer than it did a few quarters ago.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>