DICK’S Sporting Goods, Inc. (NYSE: DKS) trades near $210/share and continues to perform well in a complicated retail environment. Margins remain strong, cash flow is healthy, and demand across core athletic categories has helped the stock hold its ground even as consumer spending becomes more selective.

Recently, the company reported stronger than expected profitability and highlighted better inventory efficiency across its stores. Management also noted renewed strength in footwear and team sports, two categories that continue to outperform broader discretionary trends. These developments suggest DKS is navigating today’s retail backdrop better than many peers and still has levers to support steady earnings growth.

This article explores where Wall Street analysts expect DKS to trade by 2028. We pulled together consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

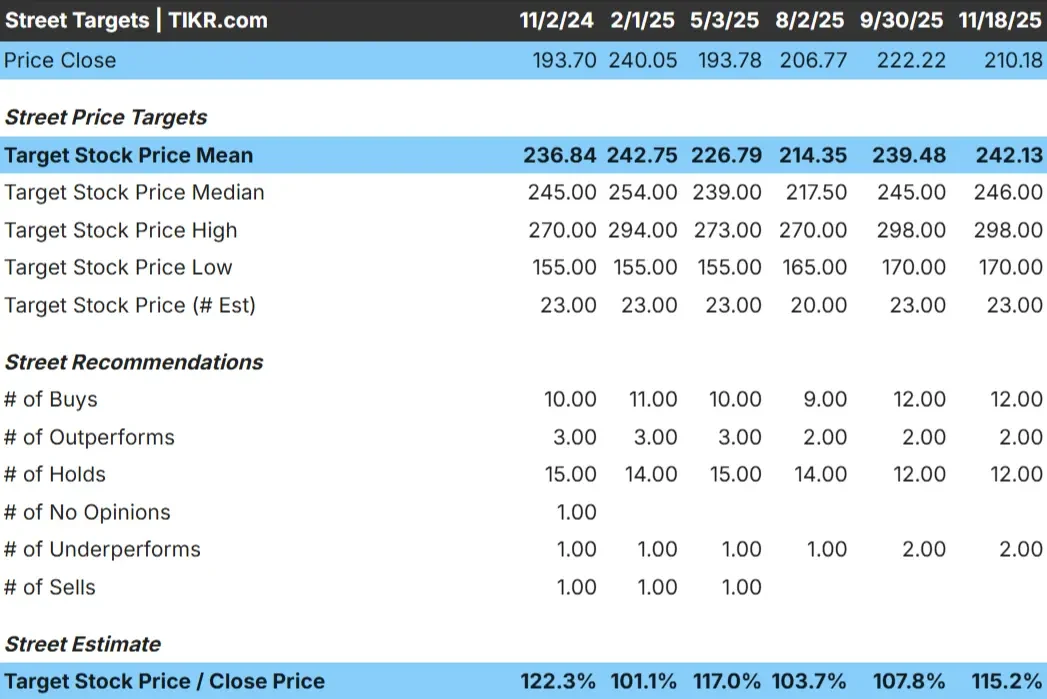

DKS trades at about $210/share today. The average analyst price target is $242/share, which points to roughly 15% upside. Forecasts show a relatively tight range, indicating steady sentiment rather than wide disagreement.

Key numbers:

- High estimate: $298/share

- Low estimate: $170/share

- Median target: $246/share

- Ratings: 12 Buys, 2 Outperforms, 12 Holds, 2 Underperforms

It looks like analysts see some room for gains, but not a major rerating. For investors, the takeaway is that DKS is viewed as a consistent, well managed retailer. The stock could move higher if demand stays healthy or if profitability continues to hold up across core categories like team sports, footwear and outdoor equipment.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

DKS Growth Outlook and Valuation

The company’s fundamentals appear solid based on the valuation model inputs:

- Revenue is expected to grow about 18% through early 2028

- Operating margins are forecast to stay near 8.9%

- Shares trade at a valuation supported by a 13x forward P E

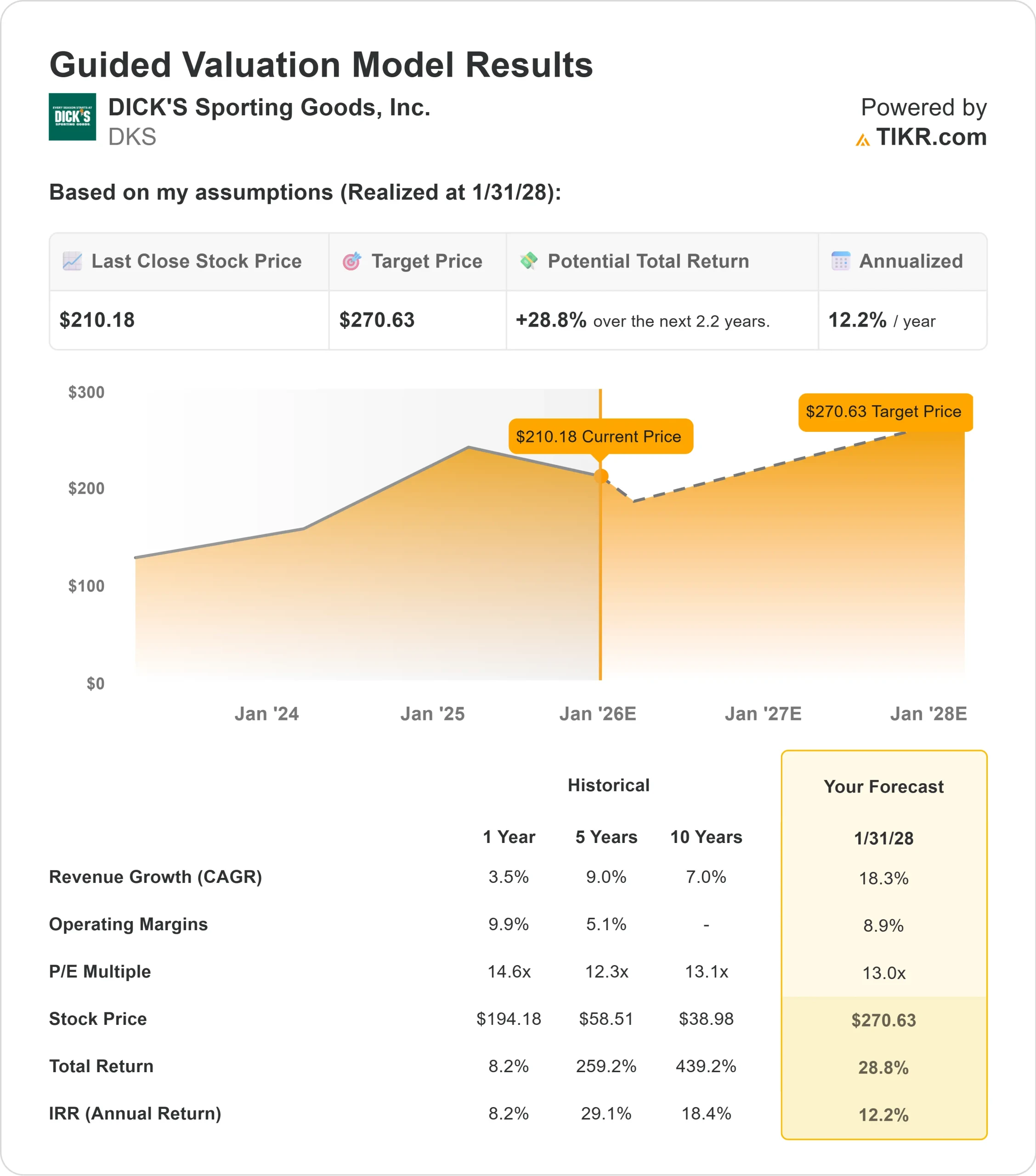

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 13x forward P E suggests about $271/share by early 2028

- That implies roughly 29% upside, or about 12% annualized returns

These numbers indicate that DKS can deliver steady compounding without requiring rapid revenue acceleration. The stock looks reasonably valued for its level of profitability, which means upside is tied to consistent execution and stable margins rather than a major shift in growth.

For investors, DKS resembles a dependable operator with reliable earnings power. Returns are likely to come from predictable performance and disciplined management, making the stock appealing for those seeking balanced, fundamentals-driven growth.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts remain constructive on DKS because the company continues to execute well in an uncertain retail environment. Demand in core categories like footwear, athletic apparel and team sports has stayed resilient, and the company has been able to protect profitability through disciplined inventory management and strong private label performance.

Management’s focus on operational efficiency, improving store productivity and enhancing customer engagement through loyalty programs and omnichannel upgrades also supports the investment case. For investors, these strengths suggest DKS has the tools to maintain steady earnings growth even if the broader retail backdrop softens.

Bear Case: Slowing Growth and Retail Headwinds

Despite the positives, analysts see real risks. Earnings momentum has cooled compared to previous years, and the company could face pressure if consumer spending weakens or if promotional activity picks up across the sporting goods category.

Competition remains a factor as well. More brands are expanding direct to consumer channels, and sporting goods demand can be cyclical. For investors, the key risk is that recent strength in margins and profitability may not be fully sustainable if the discretionary environment becomes more challenging.

Outlook for 2028: What Could DKS Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 13x forward P E suggests DKS could trade near $271/share by early 2028. From today’s price near $210/share, that represents about 29% upside, or roughly 12% annualized returns.

These returns would reflect steady progress rather than a major shift in the business. The valuation already assumes consistent margins and healthy cash flow, so stronger upside would require faster sales growth, more efficient store expansion or continued outperformance in footwear and outdoor categories.

For investors, DKS appears positioned as a dependable retailer with room for moderate gains. The long-term upside is credible, but achieving meaningful appreciation will depend on management driving better growth and maintaining strong operating discipline.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>