Five Below (NASDAQ: FIVE) has rebounded sharply over the past year as investor sentiment improved, but the picture is still mixed. Revenue growth remains healthy, yet margins continue to face pressure, and the stock’s rapid move higher has raised questions about how much upside is left. Even with these challenges, the company’s long runway for new store openings keeps analysts optimistic about its long term growth potential.

Recently, Five Below highlighted stronger trends in its “Five Beyond” format, which continues to expand and lift average transaction values. The company also reported improved inventory positioning heading into the holiday season, giving management confidence in both traffic and merchandising strategy. These developments suggest Five Below is actively strengthening its model at a time when value focused retail is gaining momentum.

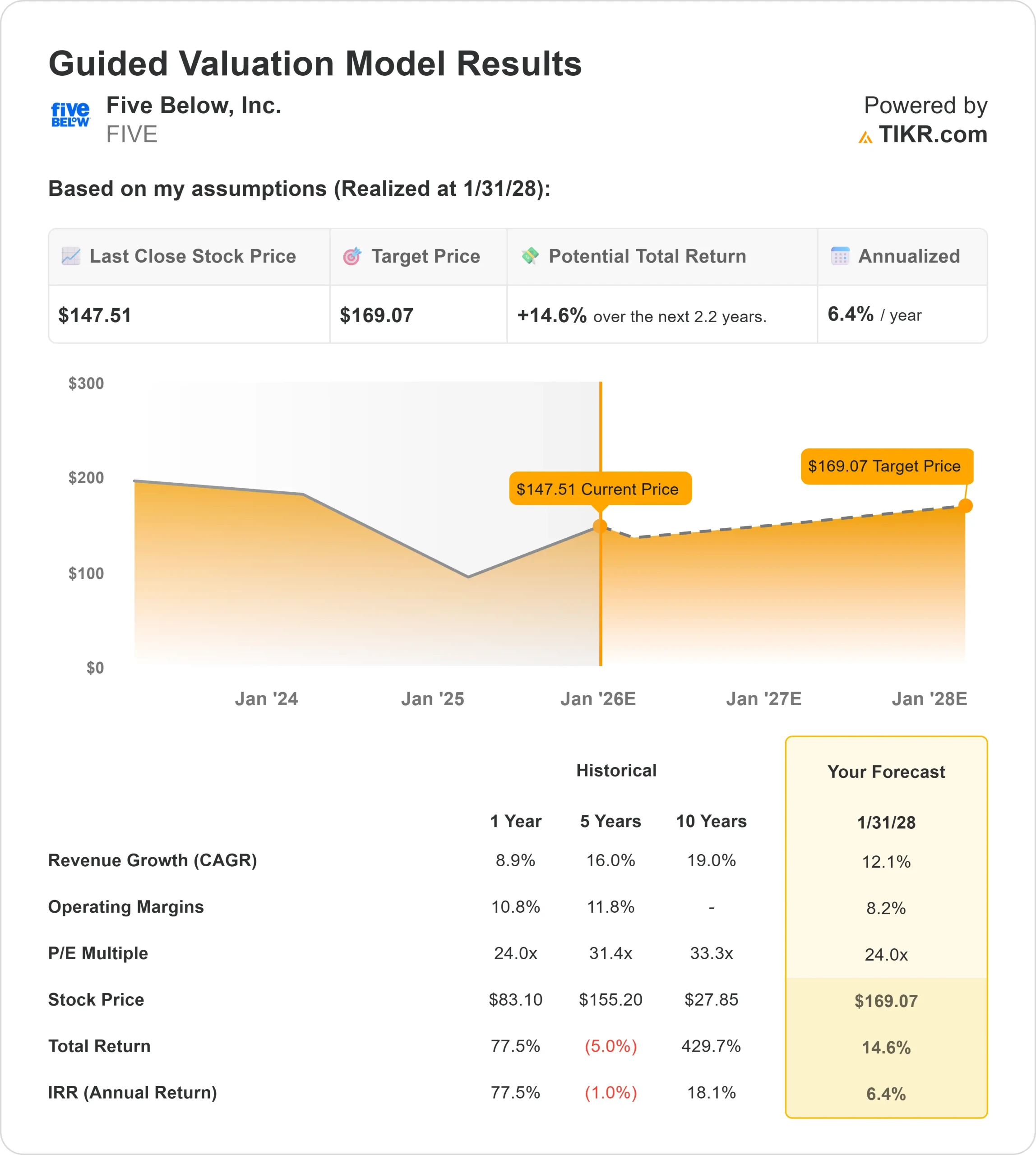

This article explores where Wall Street analysts expect Five Below to trade by 2028. We have pulled together consensus price targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

Five Below trades at about $148/share today. The latest analyst average price target is $162/share, which points to roughly 10% upside, placing the stock in the modest upside category. The wide range of estimates reflects mixed conviction among analysts:

- High estimate: $190/share

- Low estimate: $90/share

- Median target: $167/share

- Ratings: 10 Buys, 2 Outperforms, 11 Holds, 1 Sell

Analysts see some room for gains, but uncertainty around margins and consumer spending keeps expectations balanced. For investors, the stock could move sharply in either direction depending on how well Five Below executes over the next few quarters.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Five Below: Growth Outlook and Valuation

The company’s fundamentals appear steady, supported by healthy revenue growth and continued investment in new stores. Profitability remains softer than past years, which explains why expectations for long term returns are measured rather than aggressive. The valuation model reflects a more balanced outlook for the next few years.

- Revenue is projected to grow about 12.1% annually through early 2028

- Operating margins are expected to land near 8.2%

- The valuation model applies a 24x forward P E

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests about $169/share by 1/31/28

- That implies roughly 14.6% total return, or about 6.4% annualized

These numbers suggest Five Below can compound steadily but not at the pace of its strongest years. Returns look reasonable, but the premium valuation means stronger upside depends on better margin performance or more efficiency from new stores.

For investors, Five Below screens more like a reliable growth retailer than a high return opportunity. Upside from here will depend on management’s ability to improve profitability while scaling its expansion strategy.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts remain optimistic because Five Below continues to execute well on its expansion strategy. The “Five Beyond” format is lifting average transaction values and helping the company expand into higher priced categories without losing its value appeal. The brand also continues to resonate with younger, price sensitive shoppers, supporting consistent traffic even in a softer retail environment.

Inventory management has also improved, allowing Five Below to merchandise more effectively and maintain product availability during peak seasons. For investors, these strengths show the company still has meaningful levers to drive steady revenue growth and maintain its competitive position.

Bear Case: Margin Pressure and Competition

Even with these positives, profitability remains a key concern. Rising labor costs, supply chain pressures, and the pace of new store openings have kept margins from recovering to historical levels. The business needs stronger operating leverage to fully unlock its earnings potential.

Competition is also intense across value retail, with Dollar Tree, Dollar General, Walmart, and Target all fighting for a similar customer base. Any softening in discretionary spending could make margin recovery even more difficult. For investors, the risk is that strong sales growth may not translate into stronger earnings growth if margin pressure persists.

Outlook for 2028: What Could Five Below Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 24x forward P E suggests Five Below could trade near $169/share by 1/31/28. That represents about 14.6% total return, or roughly 6% annualized.

While this reflects a solid long term outcome, it already assumes stable margins and continued store expansion. To unlock stronger upside, Five Below would need clearer signs of margin expansion, better merchandise profitability, or stronger productivity from its newer stores. Without these improvements, returns are likely to remain moderate and aligned with the model’s expectations.

For investors, Five Below stands out as a durable long term revenue grower, but the stock’s next phase of performance will depend on whether management can strengthen profitability while scaling the business.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>