O’Reilly Automotive (NASDAQ: ORLY) trades near $99/share today after a steady year in auto parts retail. Growth has cooled compared to earlier years, but the company continues to benefit from strong margins, stable demand for repair parts, and one of the most efficient operating models in specialty retail.

Recently, O’Reilly highlighted improving same store sales heading into the winter season and reported stronger momentum in professional sales. Management also tightened expense control and improved inventory turnover, helping preserve margins even in a soft consumer environment. These developments show that O’Reilly is still executing well despite a more normalized backdrop.

This article explores where Wall Street analysts expect ORLY to trade by 2027. We pulled together consensus price targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

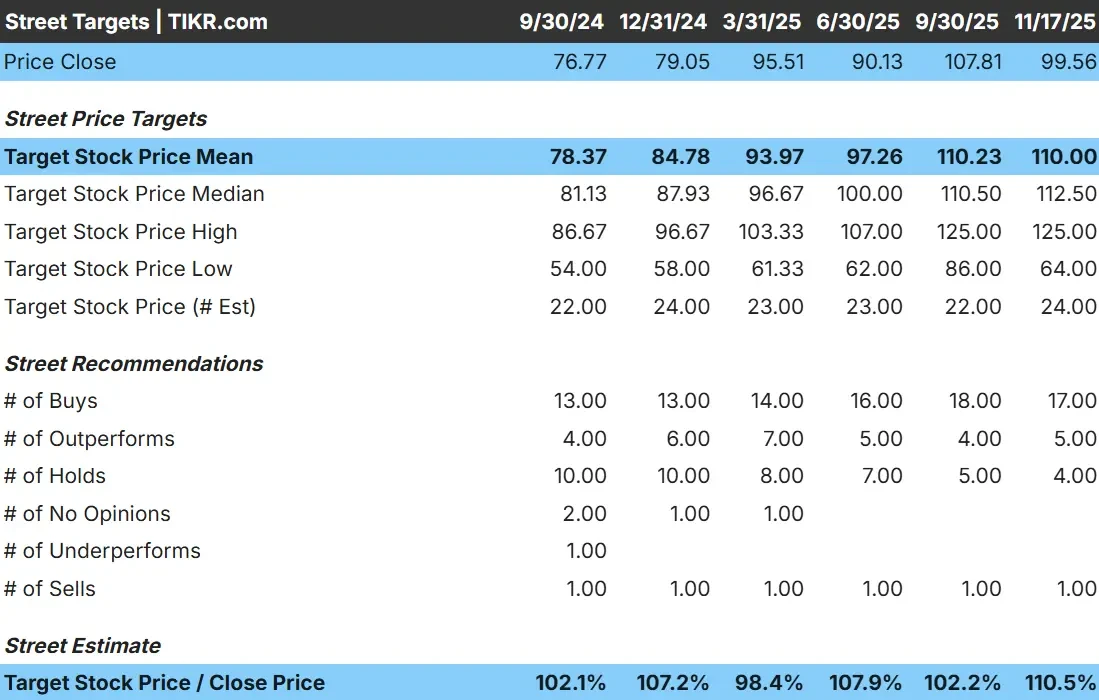

O’Reilly trades around $100/share today. Analyst targets point to modest gains from current levels:

- Median target: $113/share

- High estimate: $125/share

- Low estimate: $64/share

- Ratings: 17 Buys, 5 Outperforms, 4 Holds, 1 Sell

With roughly 10% to 11% upside to the mean target, analysts expect modest appreciation. The wide range between the high and low estimates shows mixed conviction. For investors, this suggests ORLY could outperform if results stay strong, but much of the expected upside may already be reflected in the stock.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

O’Reilly: Growth Outlook and Valuation

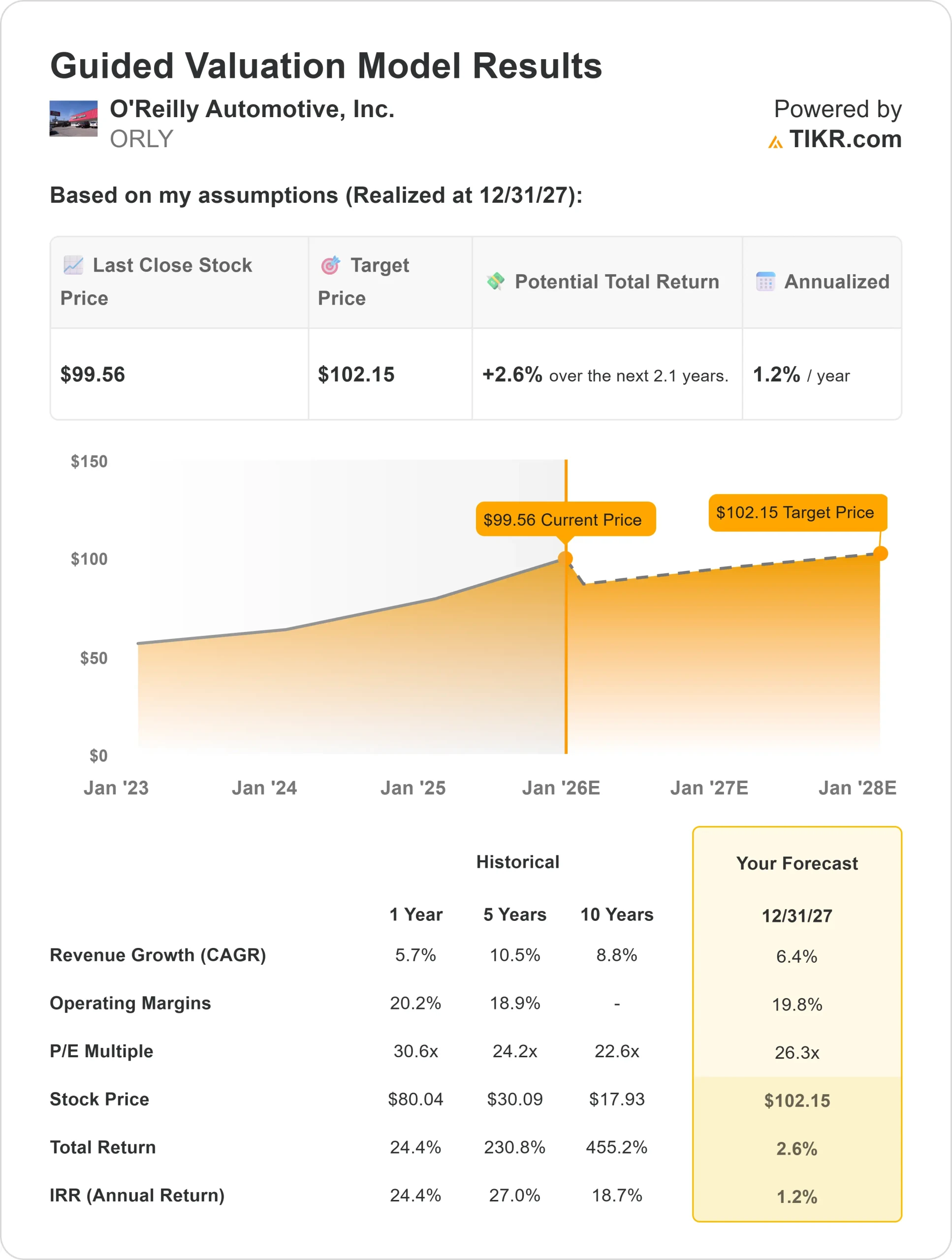

The company’s fundamentals appear steady based on the latest model inputs:

- Revenue growth is forecast at 6.4%

- Operating margins are expected to hold near 19.8%

- Shares are valued using a 26x forward P E multiple

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests about $102/share by 2027

- That implies roughly 3% upside, or about 1% annualized returns

These numbers point to a business that continues to execute well but is not priced for major gains. For investors, O’Reilly looks more like a steady compounder with reliable financial performance rather than a stock positioned for meaningful valuation expansion in the near term.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

O’Reilly’s operating model continues to stand out for its strong margins, disciplined cost structure, and dependable performance in many types of economic environments. Demand for maintenance and repair parts tends to hold up even when discretionary spending weakens, giving the company a steady base of recurring business.

Management has also continued to improve store efficiency, strengthen professional relationships, and optimize operations across its network. For investors, these strengths support confidence that O’Reilly can keep delivering reliable earnings growth over time.

Bear Case: Slowing Growth and Valuation Limits

Despite its strengths, O’Reilly faces some natural constraints. Growth has normalized from earlier highs, and margins are already elevated, limiting room for further improvement. As a result, valuation becomes more sensitive to any slowdown in same store sales or profitability.

Competition remains active in the auto parts category, with major peers investing to defend market share. If industry conditions soften or pricing tightens, investors may question whether ORLY’s premium valuation is sustainable. For investors, this highlights the importance of consistent execution to defend the current stock price.

Outlook for 2027: What Could O’Reilly Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests ORLY could trade near $102/share by 2027, which represents about 3% upside and roughly 1% annualized returns.

This outlook already assumes stable growth and solid margins. For stronger upside, O’Reilly would need to outperform analyst expectations through faster revenue growth or additional efficiency gains. Without that, the stock appears positioned for steady but limited returns over the next few years.

For investors, O’Reilly remains a high quality operator with dependable fundamentals, but the current valuation suggests modest upside unless earnings accelerate beyond current forecasts.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>