Carvana Co. (NYSE: CVNA) has continued its impressive rebound as profitability improves and leverage declines. Shares trade around $323/share, reflecting a volatile but much stronger business than a year ago. The company’s turnaround has been driven by tighter cost controls, better margin performance, and stronger unit economics that have reshaped investor sentiment.

Recently, Carvana reported another period of meaningful margin improvement, supported by stronger gross profit per unit and more disciplined inventory management. The company also made progress on refinancing efforts that reduced near term debt pressure and improved liquidity. These developments suggest a business that is stabilizing financially while building a foundation for more predictable growth.

This article explores where Wall Street analysts think Carvana could trade by 2027. We pulled together consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

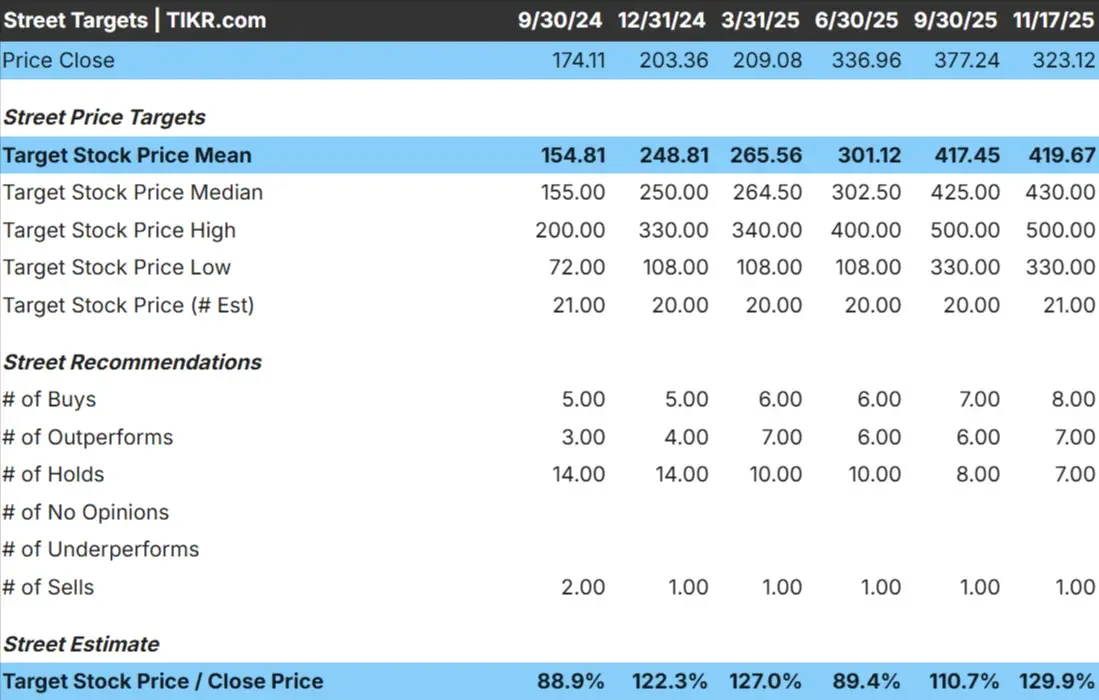

Carvana trades near $323/share today. The average analyst price target is about $420/share, which implies roughly 32% upside. That qualifies as meaningful upside based on current expectations. Forecasts still vary widely, showing that analysts have mixed conviction about how durable the company’s improvements will be.

- High estimate: ~$500/share

- Low estimate: ~$330/share

- Median target: ~$430/share

- Ratings: 8 Buys, 7 Outperforms, 7 Holds, 1 Sell

For investors, the takeaway is that analysts see room for gains, but the stock’s trajectory depends on Carvana maintaining momentum in profitability and balance sheet repair. If execution stays consistent, the stock could outperform over the next few years.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Carvana: Growth Outlook and Valuation

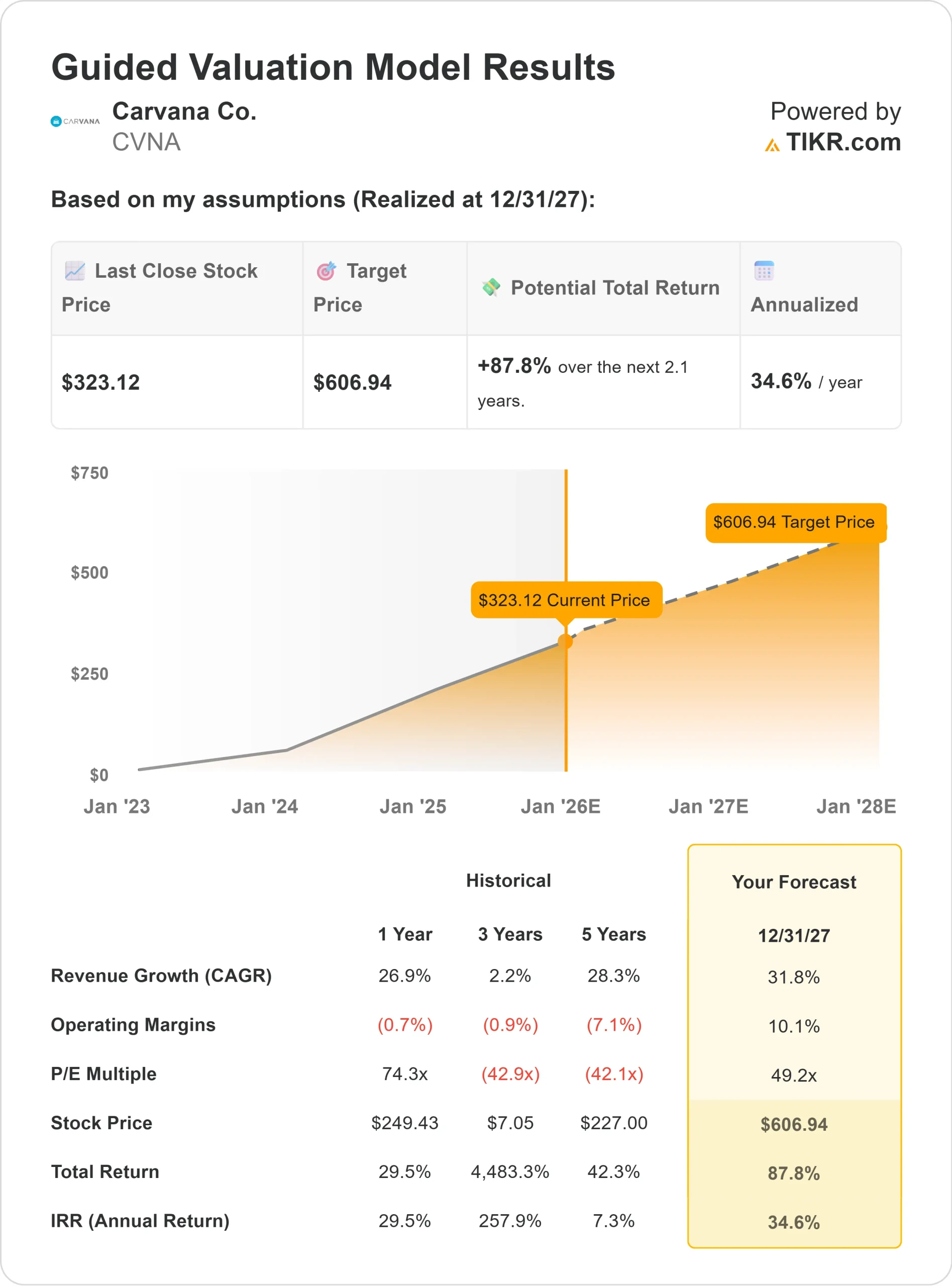

Carvana’s fundamentals appear much stronger than they were in prior years. Analysts expect meaningful progress in profitability and operating efficiency, which shapes the valuation outlook.

- Revenue growth is projected at 31.8% through 2027

- Operating margins are expected to reach 10.1%

- Shares trade at a forward P E of 49.2x

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 49x forward P E suggests a value near $607/share by 2027

- That implies about 88% upside, or roughly 35% annualized returns

These numbers suggest Carvana can compound rapidly if current execution holds. The business does not require extraordinary sales growth for the stock to work. Instead, the path to higher returns depends on stable margins, disciplined costs, and avoiding a return to heavy leverage.

For investors, Carvana offers significant upside potential, but the story hinges on consistent operational performance rather than aggressive expansion.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Bullish analysts highlight Carvana’s improving operational discipline. The company has tightened its logistics network, refined its purchasing processes, and steadily rebuilt profitability through stronger unit economics. These improvements reduce volatility and make the business more predictable than it was in earlier years.

Carvana has also strengthened its financial position. Improved liquidity and lower balance sheet stress give the company more flexibility to execute its strategy without relying on heavy external financing. These positive shifts have rebuilt confidence that Carvana can sustain its turnaround.

For investors, these strengths suggest that Carvana is transitioning from a high growth but inconsistent operator to a more stable business with clearer pathways to earnings expansion.

Bear Case: Volatility and Execution Risk

Despite the progress, some analysts remain cautious. Carvana still trades at a premium valuation, which leaves little room for error. Any slowdown in margin improvement or operational efficiency could quickly compress the stock’s multiple.

Competition is another concern. Traditional dealerships and digital platforms continue to improve their online buying experiences, making the landscape more crowded. Carvana’s high sensitivity to market swings also remains a factor, and periods of economic uncertainty could weigh on sentiment.

For investors, the risk is that expectations may be running ahead of fundamentals. Carvana must maintain consistent execution to justify its current valuation and the upside implied by analyst models.

Outlook for 2027: What Could Carvana Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Carvana could trade near $607/share by 2027, which would represent about 88% upside and roughly 35% annualized returns.

While this scenario reflects strong potential, it already assumes continued improvement in efficiency, margins, and financial discipline. To outperform these expectations, Carvana would need to deliver stronger execution across its logistics network, cost structure, and customer experience.

For investors, Carvana offers one of the most compelling upside profiles among consumer automotive stocks, but it comes with above average volatility. The opportunity is real, but consistent performance will determine whether the stock can reach the valuation implied in the model.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>