Loblaw (L) is one of those companies that most Canadians interact with every week without thinking about it. The stores are familiar, the brands are everywhere, and the business has quietly become one of the most important defensive names in the country.

For investors, Loblaw often falls into the category of companies that rarely surprise you but consistently deliver. The company is built on scale, logistics strength, and a portfolio that blends grocery, pharmacy, and health offerings. That combination has helped Loblaw navigate a complicated retail environment with more stability than most competitors.

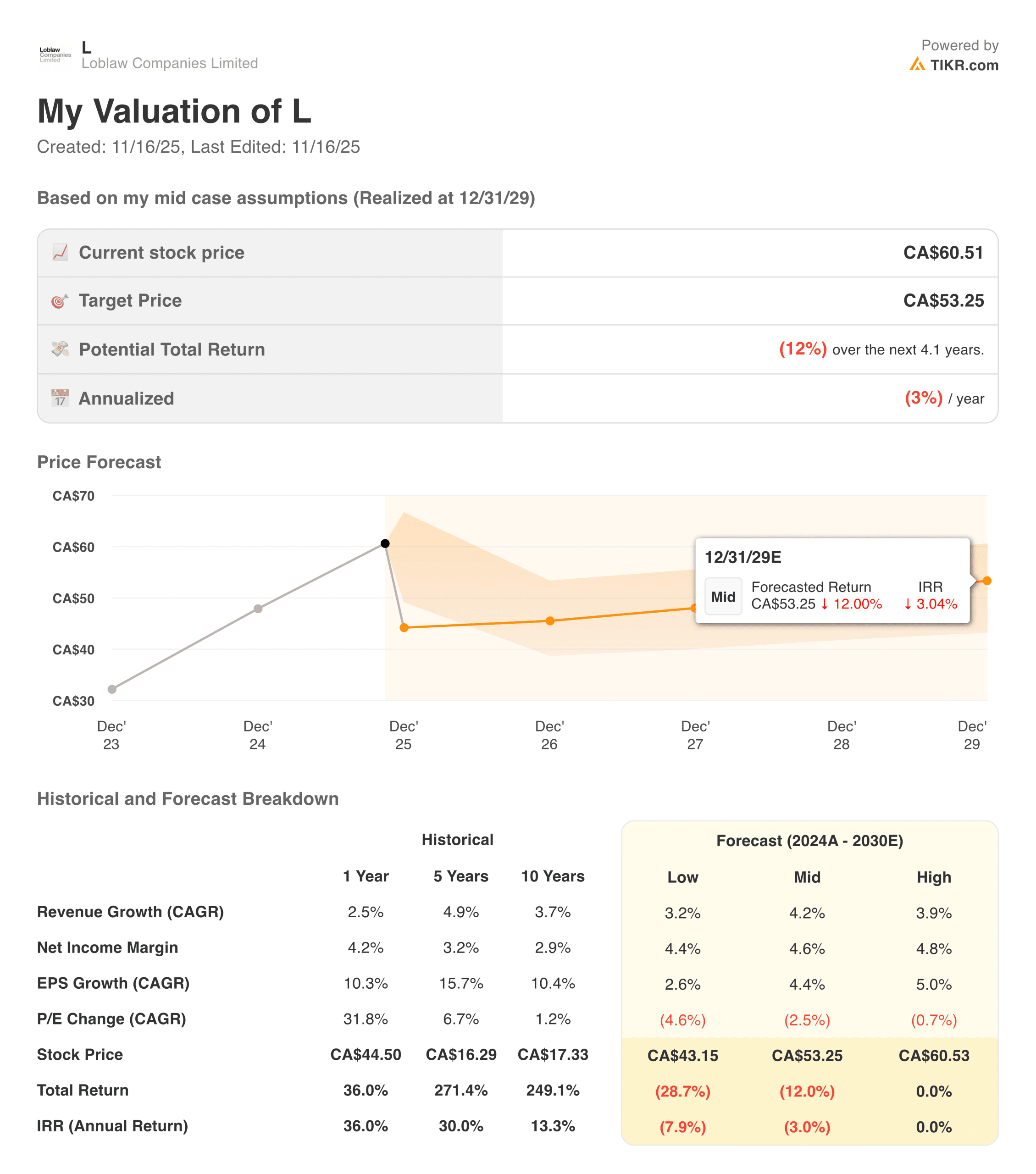

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The past year showed how that structure holds up during challenging periods. Inflation hit consumer budgets, food prices came under scrutiny, and retailers faced ongoing cost pressures. Even so, Loblaw managed to maintain steady traffic, protect margins, and generate earnings growth. The company leaned on its private label brands, optimized promotions, and continued investing in its loyalty and digital programs. These moves helped it stay competitive while keeping profitability on track.

As investors think about 2026, the question becomes whether Loblaw can keep delivering this predictable performance. The backdrop is improving. Consumer spending is normalizing, inflation is easing, and the company’s mix of defensive staples and higher margin categories continues to work in its favor. Loblaw is not a fast growth story, but it is the kind of dependable operator that tends to outperform when stability matters most. Understanding the drivers behind that stability helps clarify where the stock may be heading next.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Loblaw returned 27.2 percent over the past 0.87 years, which translates into a 32.1 percent CAGR. The stock climbed gradually through early 2025 as the company posted steady revenue growth and delivered consistent EBIT expansion across both grocery and pharmacy.

Investors often look for signs of margin pressure in an inflationary environment, but Loblaw held its ground. The company balanced promotional spending with strong sales in its controlled private-label brands, especially President’s Choice and No Name, helping protect profitability.

| Metric | Q3 2025 | YoY Change |

|---|---|---|

| Revenue | 18.27B | +0.9% |

| Gross Profit | 5.45B | +3.6% |

| Gross Margin | 29.8% | +80 bps |

| Adjusted EBITDA | 2.19B | +4.3% |

| Adjusted Operating Income | 1.40B | +4.5% |

| Adjusted Net Earnings | 658M | +5.5% |

| Adjusted EPS | 2.12 | +6.5% |

| Free Cash Flow | 1.44B | Flat |

| Capex | 435M | +6.1% |

Earnings strength came through again in Q3. Food retail continued to show solid performance, while Shoppers Drug Mart contributed healthy gains from front store and pharmacy sales. Loblaw also kept operating expenses in check, even as investments in digital and store upgrades continued.

The combination of stable revenue growth, stronger gross margins, and disciplined spending helped the stock maintain its upward trend throughout the year. For investors looking for consistency, the financial story matched expectations.

Look up Loblaw Companies Limited full financial results & estimates (It’s free) >>>

Broader Market Context

Retailers in Canada faced a difficult environment this past year. Consumers adjusted their spending, supply chains remained uneven, and food inflation brought more attention than usual to grocery pricing. Despite that backdrop, Loblaw managed to maintain volume and traffic. This performance reflects the company’s scale advantages and its ability to pivot quickly between promotional periods and margin protection. It also highlights the strength of its loyalty program, which continued to drive engagement and repeat visits.

Looking ahead, the macro environment appears steadier. Inflation is softening, and consumer confidence has begun to improve. That supports a more predictable outlook for 2026. Loblaw’s diversified model gives it flexibility across different spending cycles. When times are tough, grocery and pharmacy keep the business stable. When the environment improves, discretionary categories and higher margin mix contribute more meaningfully. This balance is a core part of what makes Loblaw appealing to long term investors.

1. Grocery and Pharmacy Continue to Drive Stability

Loblaw’s core grocery business remained resilient throughout 2025. Traffic held up, private label penetration increased, and the company continued to invest in supply chain efficiency. These moves helped protect margins despite ongoing pressure from input costs. The grocery segment works as a stabilizer within the broader business, providing steady revenue even when consumer budgets tighten. Investors rarely expect dramatic growth from this segment, but they value its consistency.

Shoppers Drug Mart strengthened that stability. Pharmacy demand remained steady, and front store categories showed improvement as consumer spending patterns normalized. The blend of essential health products and everyday consumables creates a mix that performs well across different economic environments. As the company continues improving merchandising and digital experiences, this segment should remain one of Loblaw’s most predictable earnings contributors heading into 2026.

2. Private Label Strength Supports Margins

Private label remains one of Loblaw’s strongest competitive advantages. President’s Choice and No Name have become household names, and customers rely on them when price sensitivity increases. These brands carry stronger margins than national brands, which helps the company maintain profitability even when promotional activity rises. Over the past year, private label penetration increased again, reinforcing the idea that strong everyday value drives loyalty.

This advantage becomes even more meaningful during periods of uncertainty. Private label gives Loblaw flexibility to adjust pricing, manage costs, and shape the customer experience in ways that competitors with less brand equity cannot easily match. As inflation moderates and consumers regain confidence, private label brands continue playing a central role in driving both value perception and earnings growth. This strength remains one of the key pillars of Loblaw’s long term strategy.

Value stocks like Loblaw Companies Limited in less than 60 seconds with TIKR (It’s free) >>>

3. Strong Capital and Shareholder Returns

Loblaw has been investing heavily in digital transformation, and those efforts showed results this year. Online grocery, expanded pickup options, and improved delivery services all contributed to higher customer engagement. The company’s digital ecosystem allows it to personalize promotions and improve inventory efficiency. These enhancements may not create immediate leaps in profitability, but they strengthen the foundation for long term growth.

The loyalty program remains one of Loblaw’s most powerful strategic tools. PC Optimum continues to expand its reach, driving repeat visits and higher spending per customer. As the program adds more targeted offers and integrates with the broader ecosystem, it deepens customer relationships. The combination of digital infrastructure and loyalty engagement creates a reinforcing loop that supports both traffic and margin growth. Over time, this becomes a meaningful differentiator.

The TIKR Takeaway

TIKR’s long-term view shows a company that rarely strays far from its core strengths. Loblaw does not rely on rapid expansion or aggressive shifts in strategy. Instead, it compounds value through steady execution in grocery, pharmacy, and private label.

When you view the company’s multi-year financials, margins, and segment trends through TIKR, the consistency stands out. The business is structured to perform in a variety of environments, which makes it a reliable anchor in many portfolios.

Should You Buy, Sell, or Hold Loblaw Companies Limited’s Stock in 2025?

The stock’s strong performance in 2025 raises basic valuation questions, but the underlying business continues to deliver. The combination of private label strength, disciplined cost management, and growing digital capabilities gives the company a steady runway. Investors looking for a defensive compounder with a strong track record will likely keep Loblaw on their list.

How Much Upside Does Loblaw Companies Limited Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!