CarMax Inc. (NYSE: KMX) has been hit hard over the past year. Shares trade near $33/share, far below last year’s levels as demand, margins, and financing trends all weakened. The used-car market remains soft, but analysts still see room for a rebound if affordability improves and inventories normalize.

Recently, CarMax reported another quarter of declining unit sales, but management pointed to early signs of rising customer traffic and stronger appraisal buy rates. The company also continued expanding its omnichannel tools and tightening inventory controls, improving operational efficiency despite a difficult backdrop. These moves suggest CarMax is positioning itself for a recovery rather than standing still.

This article reviews where analysts expect CarMax to trade by 2028 using both Wall Street price targets and TIKR’s Guided Valuation Model. These figures reflect analysts’ average estimates and are not TIKR’s predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

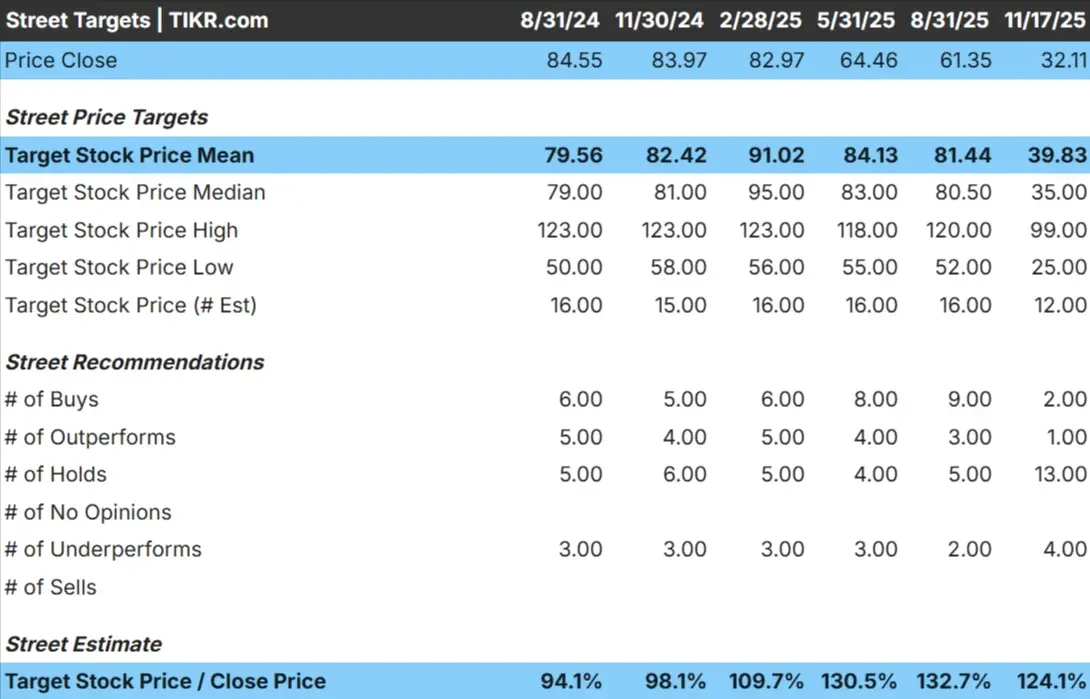

CarMax trades around $33/share today. The latest analyst average price target is $40/share, which points to modest upside from current levels. The forecast range remains wide:

- High estimate: ~$99/share

- Low estimate: ~$25/share

- Median target: ~$35/share

- Ratings: 2 Buys, 1 Outperform, 13 Holds, 4 Underperforms

Analysts see some room for gains, but the predominance of Hold and Underperform ratings shows limited conviction. For investors, this means expectations remain cautious. Any improvement in demand, margins, or financing conditions could support a rebound, but until trends stabilize, sentiment is likely to stay subdued.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

CarMax: Growth Outlook and Valuation

The company’s fundamentals appear soft based on current expectations:

- Forward 2-year revenue CAGR of (1.3%)

- Forward 2-year EBITDA CAGR of (5.2%)

- Forward 2-year EPS CAGR of (3.1%)

- Shares trade at about 14x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 14x forward P E suggests ~$53/share by early 202

- That implies about 64% upside, or roughly 24% annualized returns

These numbers show that CarMax has meaningful upside potential if results stabilize, even without strong growth. The valuation case depends more on normalizing margins and improving efficiency than on rapid revenue expansion.

For investors, CarMax looks like a possible turnaround setup. If affordability improves and volumes recover, the stock could rerate higher from today’s depressed levels.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

CarMax remains one of the strongest operators in the used-car industry. Its scale, brand recognition, and omnichannel capabilities give it competitive advantages that smaller dealers cannot replicate. These strengths help the company retain customer engagement even in a down market.

Management’s focus on improving efficiency and enhancing the buying experience also sets up the company to benefit quickly when demand improves. For investors, these operational adjustments signal a business that is preparing for the next upswing rather than reacting defensively.

Bear Case: Weak Trends and Profit Pressure

Despite its long-term strengths, the near-term picture remains challenging. Revenue is declining, earnings are under pressure, and higher financing costs continue to weigh on buyer affordability. CarMax’s cost structure is built for scale, but softer demand limits the company’s ability to fully leverage those costs.

Competition is also intensifying. Both digital retail platforms and traditional dealerships are becoming more aggressive with pricing and promotions. For investors, the risk is that stabilization takes longer than expected, which would keep margins under pressure and limit near-term upside.

Outlook for 2028: What Could CarMax Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests CarMax could trade near $53/share by early 2028. That would represent about 64% upside, or roughly 24% annualized returns.

This outcome assumes gradual improvement in volumes, better operating leverage, and a return to more normal valuation multiples. To outperform these expectations, CarMax would need to deliver stronger gains in demand, margins, and financing affordability. Without these improvements, upside is likely capped.

For investors, CarMax looks like a potential turnaround opportunity. The stock has room to rerate higher, but the path depends on improving fundamentals and consistent execution in a slow and competitive market.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>