Chewy Inc. (NYSE: CHWY) trades near $35/share after a long stretch of volatility. Growth has steadied, margins are gradually improving, and the business continues to rely on autoship as its recurring revenue engine. Even so, the stock sits well below previous highs, and the market is still waiting for a clearer path toward sustained profitability.

Recently, Chewy announced the expansion of its sponsored ads platform, giving brands more tools to promote products directly on its site. The company also reported rising adoption of its Health services and pet pharmacy offerings, which carry stronger margins and help deepen customer relationships. These developments show that Chewy is investing in higher value revenue streams that can support more profitable long term growth.

This article explores where Wall Street analysts expect Chewy to trade by early 2028. We reviewed consensus price targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

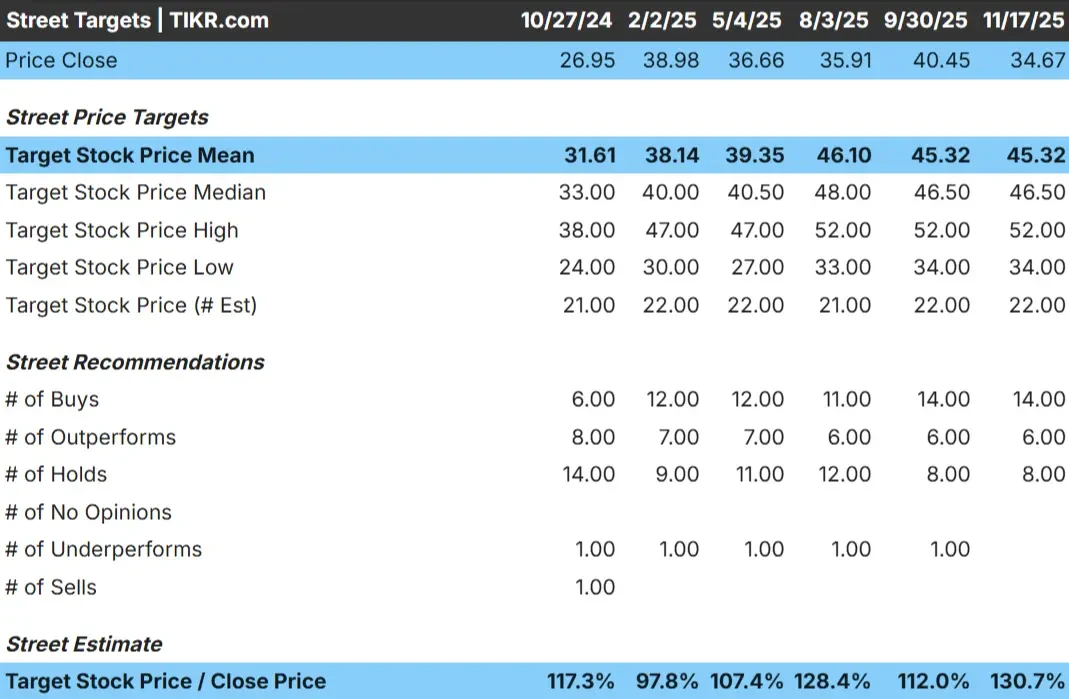

Chewy trades around $35/share today. The latest analyst average price target sits near $45/share, which points to close to 30% upside if expectations hold. The spread between estimates is relatively tight, suggesting analysts see a stable but improving outlook.

- High estimate: $52/share

- Low estimate: $34/share

- Median target: $47/share

- Ratings: 14 Buys, 6 Outperforms, 8 Holds

Analysts appear cautiously optimistic. They see room for gains but not a dramatic rerating. For investors, the stock can move higher as long as Chewy continues to improve margins and strengthen customer loyalty through autoship and subscription based engagement.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Chewy: Growth Outlook and Valuation

Chewy’s fundamentals appear stable, supported by consistent revenue expectations and gradual margin expansion. The valuation inputs point to steady but controlled progress over the next few years.

- Revenue is projected to grow about 7.6% annually

- Operating margins are expected to reach about 3.1%

- Shares trade at roughly 25x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 25x forward P E suggests about $44/share by early 2028

- That implies roughly 28% upside or about 12% annualized returns

These numbers suggest that Chewy can compound steadily, though not at the pace of high growth e commerce peers. The outlook depends on consistent execution, stronger cost discipline, and continued gains in higher margin categories.

For investors, Chewy looks more like a stable, recurring revenue story than a rapid growth play. Returns will likely track the company’s ability to expand margins and improve efficiency rather than breakthrough sales acceleration.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Chewy benefits from a loyal customer base anchored by autoship orders, which help stabilize demand and increase retention. The company is also expanding higher margin areas such as pharmacy, pet health services, and private label products, all of which can support more profitable growth.

Management continues to improve fulfillment efficiency and reduce logistics costs, which is important for a business built on high volume shipments. For investors, these strengths signal that Chewy has the pieces in place to steadily rebuild earnings momentum over time.

Bear Case: Margin Pressure and Competition

Despite its progress, Chewy still operates with thin margins. Logistics costs remain high, and maintaining a nationwide delivery network is expensive. Any missteps in efficiency could weigh on profitability. Competition from Amazon and Walmart also limits pricing power and increases the cost of acquiring new customers.

For investors, the risk is that margin gains may not come fast enough to offset these pressures. If growth slows or promotional spending rises, the timeline for improved earnings could stretch longer than expected.

Outlook for 2028: What Could Chewy Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Chewy could trade near $44/share by early 2028. That would represent about 28% upside from today or roughly 12% annualized returns. These expectations assume steady revenue growth, gradual margin improvements, and continued success in higher value offerings like pharmacy and services.

While this would mark a solid recovery, it still depends on consistent execution. To unlock stronger upside, Chewy would need to outperform in areas such as autoship retention, fulfillment efficiency, and margin expansion. Without that, investors should expect steady but not explosive returns.

For investors, Chewy looks like a reliable long term operator in the pet care space. The company has a clear path toward better earnings, but the potential for outsized gains depends on management continuing to improve profitability and deepen customer engagement.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>