Intact Financial (IFC) has built its reputation by quietly doing what reliable insurers do best. It focuses on underwriting discipline, manages risks conservatively, and generates steady returns from a well-structured investment portfolio. Even in years when the insurance sector feels choppy, the company tends to hold its ground better than most. That pattern was tested in the past year as claims costs rose, auto repair delays persisted, and Canadian insurers worked through the effects of higher inflation. For a stock known for stability, the swings were noticeable.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Yet when you look past the short-term noise, the fundamentals that define Intact are still intact. The company remains the dominant property and casualty insurer in Canada. Its personal and commercial lines continue to benefit from scale, and its specialty insurance businesses provide diversification at a time when not all segments move together. Intact’s size gives it a data advantage, and its long-term pricing approach helps it stay ahead of shifts in claims frequency and severity. That consistency is part of why investors often treat IFC as a long-term anchor rather than a tactical trade.

The question now is simple. After a year of ups and downs, does Intact still look like the dependable compounder it has been for more than a decade? The picture that emerges from recent results, combined with the pricing environment and interest rate landscape, helps clarify the path ahead. Intact may not deliver dramatic surprises, but it still offers something most investors want: steadiness, visibility, and a business model that holds up across cycles.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

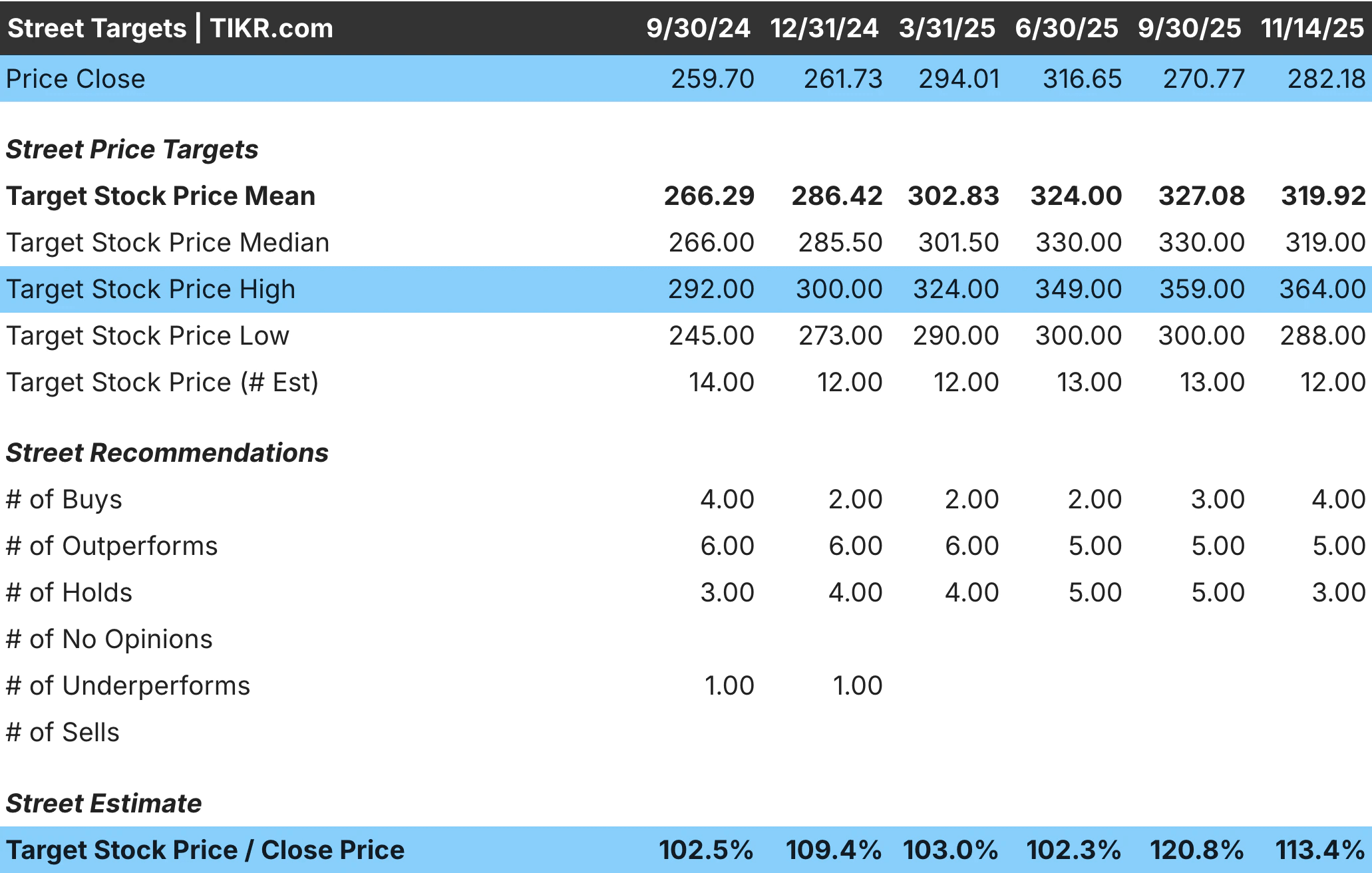

IFC returned 7.3 percent over the past year, translating to an 8.5 percent CAGR. The stock spent the first few months of 2025 climbing steadily as underwriting trends looked solid and investors took comfort in rising investment income. Sentiment shifted in midyear when claims severity across auto and property lines rose faster than expected, pushing insurers to adjust pricing and reserve assumptions. That change created pressure across the sector and pulled IFC shares down from their highs.

| Metric | Q3 2025 | Q3 2024 | YTD 2025 | YTD 2024 |

|---|---|---|---|---|

| Operating DPW | 6,643M | 6,207M | 19,038M | 17,972M |

| Combined Ratio | 89.8% | 103.9% | 89.0% | 94.2% |

| Underwriting Income | 598M | (215M) | 1,867M | 925M |

| Operating Net Investment Income | 402M | 394M | 1,217M | 1,161M |

| Distribution Income | 147M | 132M | 429M | 401M |

| Net Operating Income (NOI) | 797M | 182M | 2,449M | 1,695M |

| Net Income | 861M | 212M | 2,404M | 1,643M |

| NOIPS | 4.46 | 1.01 | 13.71 | 9.49 |

| OROE (Last 12 Months) | 19.6% | 15.8% | – | – |

| BVPS | 103.16 | – | – | – |

| Capital Margin | 3.3B | – | – | – |

| Dividends per Share | 1.33 | 1.21 | 3.99 | 3.63 |

What stands out is how the stock behaved after the downturn. Pricing improvements began flowing through, claims normalization improved visibility, and investment income remained supportive. By the fall, the stock regained momentum, reflecting a market that recognized the business’s underlying resilience.

The pullback looked more like a reset than a shift in long-term fundamentals, which fits IFC’s history. Periods of volatility tend to be temporary because the company’s earnings base is driven by predictable underwriting cycles and a disciplined balance between premium growth and risk management.

Look up Intact Financial‘s full financial results & estimates (It’s free) >>>

Broader Market Context

The Canadian insurance industry spent much of the past year navigating higher repair costs, supply chain delays, and pressure on claims margins. These challenges weighed most heavily on personal auto insurance, where inflation hit hardest. At the same time, higher interest rates boosted investment income across the sector, offsetting some margin pressure and helping results stay reasonably stable. Insurers that managed pricing proactively were better positioned heading into the second half of the year.

Intact’s advantage is that it has seen environments like this before. The company tends to respond early to rising claims costs and usually benefits from having a more diversified product set. Commercial lines remained relatively stable, and specialty insurance showed pockets of strength. As inflation cools and pricing resets fully take hold, the environment looks more favorable for 2025. Investors who follow the sector closely often view companies with steady underwriting discipline as the biggest beneficiaries of normalization, and Intact fits that category.

1. Underwriting Strength Drives Long-Term Stability

Underwriting discipline remains the foundation of Intact’s business. Management has consistently prioritized profitability over rapid premium expansion, even during periods when competitors took more aggressive approaches. That discipline resurfaced as the company adjusted pricing in response to elevated claim severity. These adjustments take time to work through, but they provide long-term stability once they are in place, and early signs point to improvement heading into the new year.

This approach also helps reduce earnings volatility. Strong underwriting cushions the company during unexpected shifts in the economy or in claims patterns. Investors who value predictability tend to gravitate toward insurers that maintain steady combined ratios without relying on investment income to offset weaknesses. Intact’s long history of staying within manageable underwriting ranges supports that view. As inflation pressures fade and claims stabilization continues, the groundwork laid over the past year should support smoother performance in the quarters ahead.

2. Strong Capital Base Supports Consistency

Balance sheet strength is one of Intact’s defining characteristics. The company maintains strong regulatory capital ratios that give it flexibility during periods of volatility. That flexibility allows Intact to navigate higher claims, pursue technology investments, and remain active in acquisition opportunities when the right fit appears. The result is a capital structure that strengthens the business rather than constraining it.

For investors, this stability has two important effects. First, it supports dividend growth and provides confidence that the company can maintain payouts even in challenging environments. Second, it gives Intact the ability to lean into growth when competitors may be more constrained. Over long horizons, insurers with strong capital positions tend to outperform those that approach the cycle with less resilience. Intact’s ability to maintain that strength throughout the past year reinforces its long-term appeal.

Value stocks like Intact Financial in less than 60 seconds with TIKR (It’s free) >>>

3. Investment Income Helps Smooth the Cycle

Higher interest rates shaped much of the insurance industry’s earnings profile this year, and Intact was no exception. The company benefited from better yields on its investment portfolio, which helped offset margin pressure in underwriting. Float is one of the most valuable tools an insurer has, and rising yields enhance the return on that float without requiring additional risk.

Even if rates begin easing in the coming year, the portfolio’s income base is still higher than during the low-rate era. That gives Intact a helpful earnings tailwind as underwriting margins normalize.

When investment income pairs with disciplined pricing and a stable balance sheet, the result is a business that can deliver consistent performance even when individual segments face temporary headwinds. That combination is one of the main reasons the company continues to hold its place among Canada’s most reliable financial stocks.

The TIKR Takeaway

TIKR’s multi-year lens makes it easier to appreciate what sets Intact apart. When you view underwriting ratios, investment income trends, and capital strength across several cycles, the consistency becomes clear. Intact rarely delivers dramatic surprises, but it consistently protects its earnings base and compounds value over time.

The combination of steady underwriting, a strong balance sheet, and improved investment income keeps the company in the category of long-term compounders that reward patience. For investors looking for reliability in the Canadian financial sector, IFC still checks the right boxes.

Should You Buy, Sell, or Hold Intact Financial’s Stock in 2025?

Intact’s valuation does not look stretched, but it is not deeply discounted either. The company’s long-term strengths remain intact. As claims trends normalize and pricing resets flow through, the business is positioned for steadier performance. For investors seeking a reliable compounder with a strong track record of consistency, IFC remains a compelling long-term option.

How Much Upside Does Intact Financial Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!