eBay Inc. (NASDAQ: EBAY) has rebounded toward the mid 80s after a volatile year. The company continues to generate strong margins, reliable cash flow, and steady improvements across its focus categories. While the business is stable, revenue growth remains modest, which limits how much upside analysts expect over the next few years.

Recently, eBay gained renewed interest from investors after rolling out AI powered listing tools that help sellers create optimized descriptions and images. The company also expanded authentication services across luxury goods and collectibles, which supports trust and strengthens its positioning in higher value categories. These moves show that eBay is actively modernizing the platform to improve both user quality and long term engagement.

This article explores where Wall Street analysts believe eBay could trade by 2027. We reviewed consensus price targets and valuation models to outline the stock’s potential path. These figures reflect analyst expectations and not TIKR predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

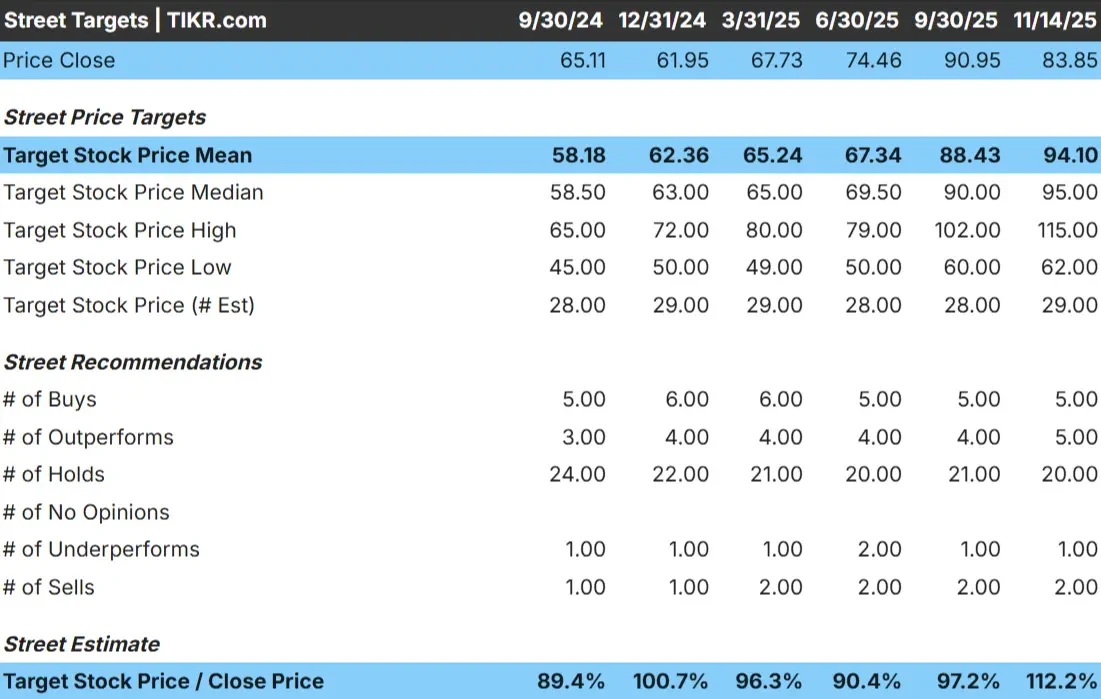

eBay trades around $84/share today. The latest analyst average price target is $94/share, which suggests about 12% upside if expectations hold. Forecasts still vary widely:

- High estimate: ~$115/share

- Low estimate: ~$62/share

- Median target: ~$95/share

- Ratings: 5 Buys, 5 Outperforms, 20 Holds, 1 Underperforms, 2 Sell

Analysts see some room for gains, but the large number of Hold ratings shows that conviction remains limited. For investors, the stock is viewed as a steady performer rather than a high growth opportunity. Upside is possible if the company delivers cleaner execution, stronger buyer activity, or better category performance, but expectations remain modest.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

eBay: Growth Outlook and Valuation

The company’s fundamentals appear stable based on the valuation inputs shown in the model:

- Revenue is projected to grow about 5.4% through 2027

- Operating margins are expected to reach roughly 28.1%

- Shares trade at an implied 11.8x forward P E in the model

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11.8x forward P E suggests eBay could trade near $84/share by 2027

- That implies roughly 1% total return and 0% annualized gains

These numbers suggest eBay can continue to compound steadily, but not at a pace that will drive significant valuation expansion. The stock already reflects its current growth profile, which means upside depends on the company delivering better than expected GMV trends or stronger adoption of higher margin services.

For investors, eBay looks more like a dependable cash flow story than a high growth opportunity. Returns will likely come from dividends and buybacks unless management can unlock stronger top line momentum.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

eBay continues to benefit from a business model that produces consistent and healthy profitability. The company remains focused on categories where it can stand out, such as refurbished goods, collectibles, and luxury items. Authentication programs and AI powered listing tools improve trust and efficiency, which helps attract more serious buyers and sellers.

These initiatives support a higher quality marketplace and deepen engagement within core verticals. For investors, this indicates that even without rapid growth, eBay has several levers that can stabilize the business and sustain long term cash generation.

Bear Case: Slow Growth and Competitive Pressure

Despite these strengths, eBay’s growth outlook remains modest. Buyer activity has not seen a meaningful rebound, and GMV trends continue to fluctuate. This makes it difficult for the company to expand beyond a mid single digit growth profile, which limits the potential for valuation expansion.

Competition also remains intense across ecommerce and social commerce channels. If eBay cannot show consistent progress in attracting buyers or increasing transaction activity, the stock may remain range bound. For investors, the risk is not that eBay breaks down, but that it delivers steady yet uninspiring returns.

Outlook for 2027: What Could eBay Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11.8x forward P E suggests eBay could trade near $84/share by 2027. From today’s price near $84/share, that implies roughly 1% total return over the next few years.

While this outlook reflects stability, it also shows that expectations are already low. eBay will need clearer signs of GMV growth, improved buyer activity, or higher adoption of its new platform features to generate more substantial upside. Without a meaningful catalyst, returns will likely be steady but limited.

For investors, eBay remains a dependable cash generating marketplace, but stronger performance will require the company to outperform today’s conservative assumptions. Execution and product improvements will matter most.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>