Warby Parker Inc. (NYSE: WRBY) trades near $17/share after a challenging year, with the stock down nearly 29%. Revenue growth has remained steady, but profitability is still developing, which has kept investor sentiment cautious. Even so, analysts point to healthy gross margins and improving operational efficiency as reasons the stock could recover if execution remains consistent.

Recently, the company posted another quarter of solid revenue growth and highlighted stronger productivity across its expanding retail footprint. Warby Parker is also pushing deeper into eye exams and vision services to drive more repeat visits and strengthen customer lifetime value. These moves suggest the company is building a more durable long term model even in a softer discretionary spending environment.

This article reviews where Wall Street analysts expect Warby Parker to trade by 2027 based on consensus targets and TIKR’s Guided Valuation Model. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

Warby Parker trades around $17/share today. The latest analyst average price target is $22/share, which points to about 30% upside from current levels. Forecasts vary widely, showing that sentiment is still mixed even with a clear path for gains.

- High estimate: $31/share

- Low estimate: $18/share

- Median estimate: $24/share

- Ratings: 7 Buys, 1 Outperform, 6 Holds

Analysts see meaningful upside, but conviction depends on consistent improvement in margins and store level performance. For investors, this means the potential is real, but closely linked to how effectively the company executes over the next several quarters.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Warby Parker: Growth Outlook and Valuation

The company’s fundamentals appear steady, supported by strong unit economics and improving operational efficiency. Analysts expect revenue to grow at a healthy pace over the next few years as Warby Parker continues expanding its retail footprint and strengthening its service offerings.

- Revenue is projected to grow around 13% annually through 2027

- Operating margins are expected to reach about 7%

- Shares trade at roughly 37x forward earnings

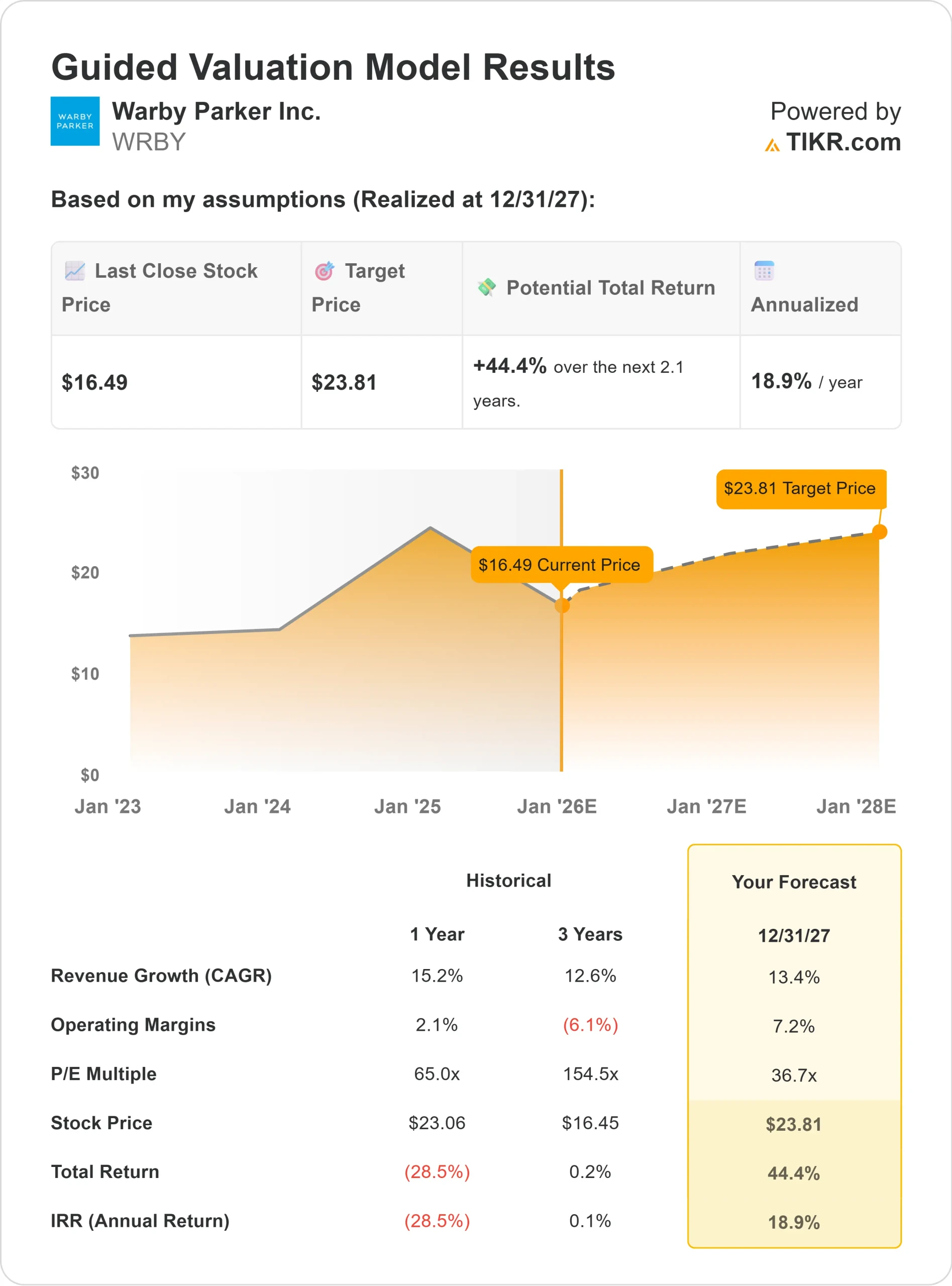

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 37x forward P/E suggests the stock could trade near $24/share by 2027

- That implies about 44% upside, or roughly 19% annualized returns

These numbers point to a business that can compound steadily as efficiency improves. Warby Parker does not need very fast growth for the stock to work, and even modest gains in profitability can meaningfully expand earnings over time.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Warby Parker continues to benefit from a strong brand and a business model that encourages repeat engagement. Its expanding retail network is helping reduce customer acquisition costs and improving in store productivity, which supports more consistent revenue. The company’s growing suite of vision services also strengthens customer relationships and encourages long term loyalty.

Management has also focused on improving operating efficiency, with better cost discipline and more scalable processes beginning to show up in results. For investors, these strengths suggest Warby Parker has the foundation to steadily improve earnings as it gains scale.

Bear Case: Execution and Valuation

Despite these positives, Warby Parker’s valuation remains demanding for a company still early in its profitability journey. Shares trade at a premium multiple, which means the stock has limited room for setbacks. Any slowdown in revenue, margin progress, or store level productivity could pressure the stock.

Competition is another important risk. The eyewear market includes large retail chains, insurance backed providers, and fast growing online players. Pricing pressure and shifting consumer behavior could make consistent margin expansion more difficult. For investors, the concern is that improvements may take longer than expected, making the valuation harder to justify.

Outlook for 2027: What Could Warby Parker Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 37x forward P/E suggests Warby Parker could trade near $24/share by 2027. That represents roughly 44% upside, or about 19% annualized returns.

This outlook already assumes steady revenue growth and improving profitability. To unlock stronger upside, the company would need faster progress in its vision care services, higher store productivity, or more substantial operating leverage. Without that, investors should expect a gradual and measured recovery.

For investors, Warby Parker offers meaningful upside, but the long term payoff depends heavily on consistent execution. The company has the pieces needed to scale earnings, yet the trajectory will be dictated by how effectively it converts strong gross margins into durable profitability.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>