Ocado Group (OCDO) operates two connected businesses with Ocado Retail, which runs the online grocery partnership with M&S, and Ocado Technology Solutions, which provides automated fulfillment systems to global grocery partners. The two segments share a standard technology base but have distinct economics. Retail captures consumer demand while technology solutions anchor long-term contracted revenue.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

The group’s strategy focuses on three priorities. These are higher retail efficiency, faster deployment of new partner sites, and lower capital spending. The management team believes that scale across modules and support services will improve margin quality over time. The company also expects automation improvements to reduce future delivery and labor costs.

Ocado has made progress this year, with the number of live modules growing. Recurring revenue from Technology Solutions has increased while retail profitability has improved as customer demand stabilized. These gains show that the underlying model has strength. The business still faces cost challenges and significant cash needs, so the task ahead is to achieve consistency across both segments.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

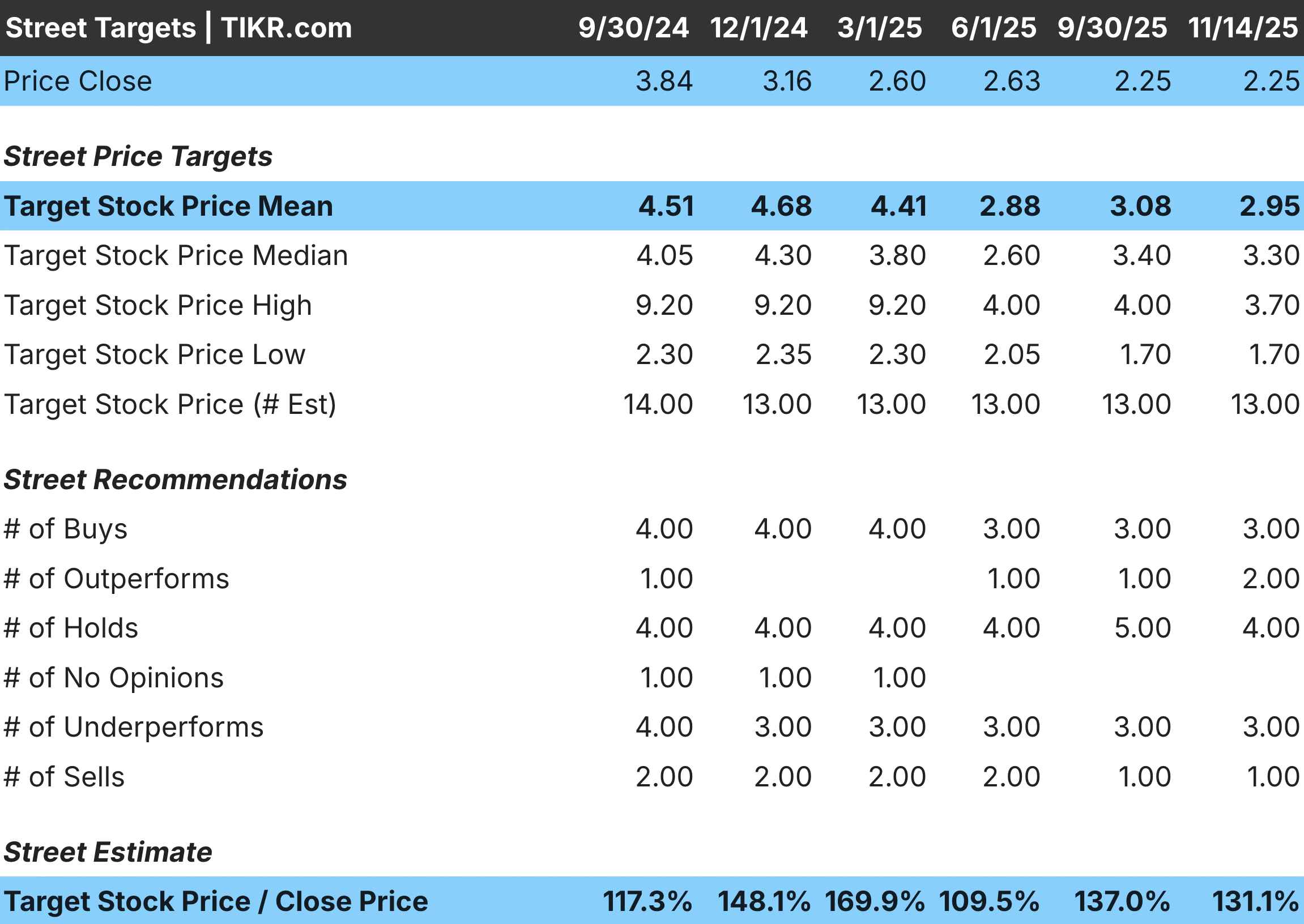

Financial Story

The first half of 2025 indicates mixed but improving trends, with group revenue reaching £1.57 billion, up 7% year on year. Retail grew by 4% due to higher average order sizes and better customer retention. Technology Solutions revenue rose by thirteen percent as more modules entered live service. These gains helped improve EBITDA, but the company still recorded an overall loss.

| Metric | HY2025 | YoY Change | Notes |

|---|---|---|---|

| Group revenue | £1.57B | Up 7 percent | Growth in Retail and Technology Solutions |

| Retail revenue | £1.33B | Up 4 percent | Higher order frequency and basket stability |

| Retail EBITDA | £34M | Up from £16M | Better cost control |

| Technology Solutions revenue | £243M | Up 13 percent | More modules in live service |

| Technology Solutions EBITDA | £35M | Up from £28M | Stronger recurring income |

| Total modules live | 132 | Up from 120 | Expansion across multiple partners |

| Cash outflow | Negative | Improved but still negative | Capex down year on year |

| Target | FY26 cash flow positive | Unchanged | Dependent on execution |

Retail EBITDA reached £34 million, compared with £16 million last year. Better cost control and increased order density drove the improvement. Technology Solutions delivered £35 million of EBITDA, up from £28 million. Partner fee income and higher services revenue supported the gain. The combined segments show that Ocado can generate operating leverage under stable conditions.

Cash flow remains the main challenge. Net cash outflow improved but stayed negative. Capital spending fell as the company reduced investment in new sites and focused on completing committed projects. Management expects a further reduction in spending next year. The company aims for positive cash flow in FY26. Achieving that goal will depend on steady Retail profitability, partner ramp performance, and better control of central costs.

Look up Ocado Group’s full financial results & estimates (It’s free) >>>

Broader Market Context

Online grocery penetration remains steady in the UK. Customer expectations for faster delivery and better pricing continue to shape market competition. Ocado benefits from having the most automated model among UK grocery players, but it still faces cost pressure and rising operational intensity. The model works best with high volume, so order stability is crucial.

Globally, partners are increasing automation investment. Several grocery chains continue to adopt Ocado systems to handle labor shortages and rising fulfillment needs. The pipeline shows interest in both large CFCs and local fulfilment sites. The mix provides long-term revenue visibility, but performance depends on partners reaching volume targets. This creates execution risk across multiple markets.

1. Technology Solutions Drive Long-Term Value

Technology Solutions remains the core of Ocado’s long-term strategy. Recurring revenue from services, software, and support has grown steadily. New modules entering live service lock in fee income for multiple years. This creates stability even when Retail results fluctuate. The segment also benefits from automation upgrades that increase uptime and reduce partner labor costs.

The key risk is partner performance. Ocado depends on large grocery chains scaling their sites to forecast volumes. Ramp delays reduce fee income and slow progress toward margin targets. Management continues to work with partners to improve throughput. If ramp trends stay consistent, recurring revenue can become the primary driver of margin growth.

2. Retail Shows Operational Progress but Needs Consistency

Ocado Retail improved profitability through better cost control. Higher order density and stable demand helped lift EBITDA. The business continues to attract high-value customers who favor convenience and reliability. These factors support long-term revenue stability. Retail remains an integral part of Ocado’s broader ecosystem.

The risk remains cost pressure. Delivery expenses, energy costs, and promotional intensity can increase volatility. The business relies on scale to offset these challenges. Management expects further improvement as automation supports better picking and delivery efficiency. Retail progress is essential for the group’s cash flow targets.

Value stocks like Ocado Group in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Discipline and Cash Flow Targets Shape the Next Phase

Ocado continues to reduce capital spending as major build-outs near completion. Lower capex gives the company more flexibility to manage cash needs. This helps narrow cash outflows and supports the goal of reaching positive cash flow in FY26. The shift from heavy construction to support services also improves the long-term earnings mix.

Central costs remain a focus. The company is targeting lower support costs across the group. These reductions will be necessary to meet the FY26 goal. The path is more straightforward than in past years, but the company needs consistent delivery across Retail and partner sites to reach the target. Execution remains the key theme for the next two years.

The TIKR Takeaway

Ocado is showing progress in both Retail and Technology Solutions. Recurring revenue is rising, live modules are increasing, and Retail EBITDA is improving. These trends support the long-term model and suggest strong demand for the group’s automation platform. Partner activity remains healthy, and capital spending is coming down.

Risks still exist. Cash flow remains negative. Central costs are high. Partner ramp performance varies across markets. Ocado has a clear plan, but the delivery timeline depends on consistency across both segments. The next phase requires discipline. The company is moving in the right direction, but investors should watch for steady progress rather than rapid improvement.

Should You Buy, Sell, or Hold Ocado Group’s Stock in 2025?

Ocado offers long-term potential through automation technology and recurring service revenue. Retail is stabilizing, and Technology Solutions continues to grow. The business also benefits from a clear cost reduction path. The concerns are cash flow, cost pressure, and reliance on partner execution. The shares fit investors who want long-term exposure to automation but who are comfortable with a measured, execution-focused recovery.

How Much Upside Does Ocado Group Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!