BCE Inc. (BCE) is in the middle of a tough transition period. The company is reshaping its cost structure, adjusting its capital spending plan, and trying to stabilize financial performance after a year marked by rising expenses and slow revenue growth. For investors, BCE has always been a steady income name with predictable cash flow. That predictability was tested in 2025 as the company responded to competitive pressure in wireless, changes in consumer habits, and the need to increase operational efficiency.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

This year was defined by a stronger focus on cost reductions and operational streamlining. BCE made workforce adjustments, continued its multi-year network build, and worked to improve margins in a challenging environment. The company also dealt with slower revenue momentum in media and some pressure on wireline. Even with these headwinds, BCE delivered stable wireless results, kept churn in check, and pushed ahead with initiatives designed to strengthen long-term performance. These actions form the base of its strategy heading into next year.

Investors now want to understand whether BCE’s 2025 efforts set the stage for improvement in 2026. The answer depends on how well the company executes its cost plans and how quickly free cash flow stabilizes. The current moves reflect a company taking steps to protect its balance sheet and improve efficiency. That makes 2025 a reset year, and the work done now as 2025 winds down will influence how BCE enters 2026, and whether it can regain some of the consistency it is known for.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

BCE recorded a 4.5 percent price decline over the past year, which reflects the slower pace of revenue growth and ongoing cost pressure. Despite the weak stock performance, the company delivered stable wireless service revenue and continued to add mobile subscribers. Wireless remained one of the most reliable parts of the business. Wireline and media had a softer year, which weighed on consolidated results. Even so, BCE reported steady progress on expense control and held margins better than many expected.

| Metric | Q3 2025 | YoY Change |

|---|---|---|

| Revenue | 6,049M | +1.3% |

| Service Revenue | 5,329M | +0.8% |

| Product Revenue | 720M | +5.1% |

| Adjusted EBITDA | 2,762M | +1.5% |

| Adjusted EBITDA Margin | 45.7% | +10 bps |

| Adjusted Net Earnings | 733M | +6.5% |

| Adjusted EPS | 0.79 | +5.3% |

| Cash Flow From Operating Activities | 1,914M | +3.9% |

| Free Cash Flow | 1,003M | +20.6% |

| Capital Expenditures | 891M | –6.6% |

| Capital Intensity | 14.7% | –1.3 pts |

Free cash flow remained a key focus. Year-to-date 2025 results showed pressure in this area due to elevated capital spending and restructuring charges. BCE highlighted that it expects capital spending to moderate as major network projects peak. Lower capital intensity should help support free cash flow as the company moves through the remainder of the year. The combination of lower costs and more controlled spending will be important for setting up a healthier financial profile heading into 2026.

Look up BCE’s full financial results & estimates (It’s free) >>>

Broader Market Context

Telecommunications companies across Canada faced mixed conditions in 2025. Consumer spending remained cautious, and competitive activity increased in mobile. Companies continued to invest in network upgrades, even as cost pressures created a need for greater efficiency. BCE’s response included streamlining operations, consolidating roles, and removing friction across internal processes. These changes allow the company to slow cost growth in a period where revenue gains are limited.

At the same time, media continues to evolve quickly as advertising markets were uneven and content costs remained high. BCE highlighted these challenges, and the segment continued to face revenue pressure. Despite this, BCE maintained its strategic focus on wireless and high-margin connectivity services. The broader context supports a more disciplined approach to capital allocation, and BCE’s current strategy aligns with that shift.

1. Wireless Remains the Most Reliable Driver

Wireless remained the most consistent part of BCE’s business. Subscriber additions remained healthy, churn stayed low, and service revenue held steady. This stability provides a foundation that helps offset softness in other areas. The company continues to invest in network performance and customer experience, which supports long term retention and pricing power. These efforts help maintain wireless’s importance in BCE’s overall earnings base.

Looking ahead, wireless gives BCE a clear path into 2026, and even with competitive pressure, the company has the scale and network quality needed to protect its share. As cost reductions take hold and spending levels normalize, the wireless segment becomes even more important for cash flow. Investors who watch the company closely tend to focus on this segment first because it reflects both the strength of the brand and the health of the core business.

2. Cost Reductions Are a Central Theme in 2025

BCE committed to an extensive cost-efficiency plan in 2025, reducing headcount, streamlining operational units, and reorganizing parts of the business to improve productivity. These actions create short-term charges but lead to recurring savings. BCE emphasized that its efficiency program is central to restoring margin stability after a period of rising costs.

As 2026 approaches, the success of this cost plan becomes a major part of the story. Lower expenses will help offset slow growth in other areas and give the company more room to protect cash flow. These savings also support BCE’s long-term commitment to the dividend. Investors have been watching this closely, and 2025 marked a transition year aimed at building a healthier operating model for the future.

Value stocks like BCE in less than 60 seconds with TIKR (It’s free) >>>

3. Capital Spending Begins to Find a More Sustainable Level

Capital spending remained elevated through the first three quarters of 2025 due to ongoing investments in fiber and 5G. These projects are necessary, but they put pressure on free cash flow. BCE noted that capital intensity should ease as the network build progresses. This shift is important because lower spending frees up cash for other priorities, including balance sheet strength and continued shareholder distributions.

A more sustainable capital program sets up a clearer runway for 2026. When major projects reach completion, BCE can redirect more cash toward financial stability. The company also highlighted progress in expanding high quality connections, which should support long term customer value. These investments take time to translate into stronger financial results, but the groundwork is being laid now.

The TIKR Takeaway

TIKR makes the shape of BCE’s transition clear, and the multi-year data highlights a company moving through a reset phase, managing cost pressure, and working to stabilize cash flow. Wireless remains solid. Wireline and media face challenges. Cost reductions and steady capital spending improvements form the foundation of the story as the company moves toward 2026. Investors can see this shift clearly by reviewing BCE’s revenue mix, margins, and free cash flow path on TIKR.

Should You Buy, Sell, or Hold BCE Inc’s Stock in 2025?

The stock reflects a tough year, but the company is taking steps to strengthen its financial position. Wireless performance, cost reductions, and a more sustainable capital program support the long-term case. BCE is unlikely to deliver rapid growth, but it remains a durable operator with a clear path to a steadier 2026 if execution improves.

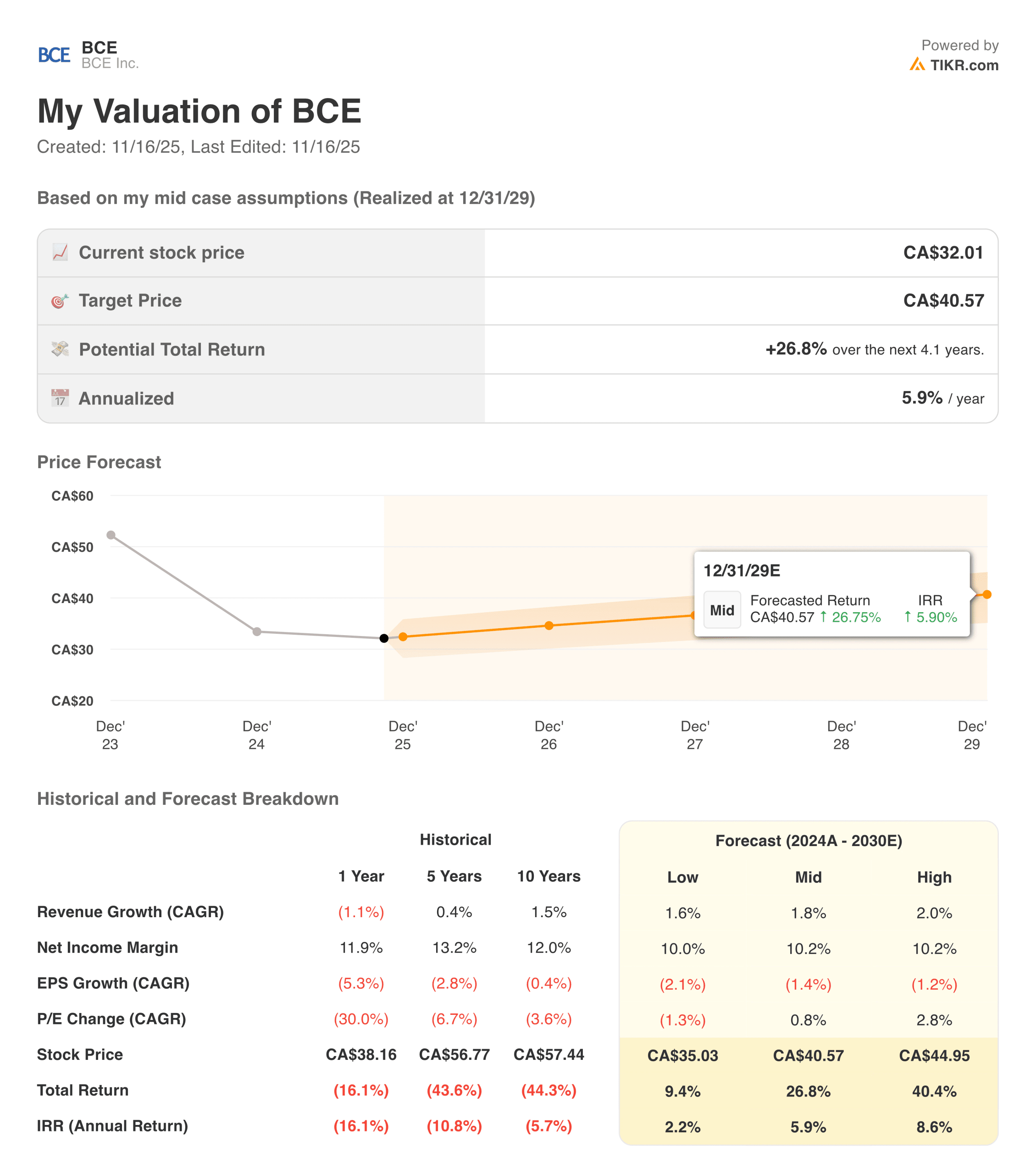

How Much Upside Does BCE Inc. Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!