Academy Sports and Outdoors Inc. (ASO) has faced a tougher stretch over the past year. Sales trends have softened, margins have come down from post-pandemic highs, and discretionary spending remains uneven across the sporting goods category. The stock trades near $42/share, down about 9% over the past year as investors reassess the company’s growth prospects. Even so, Academy’s strong profitability metrics and value-oriented positioning continue to give analysts reasons to stay constructive.

Recently, Academy highlighted improving store productivity and stronger inventory discipline in its latest updates. Management also emphasized progress in omnichannel fulfillment and assortment optimization, both of which helped support solid gross margins despite softer demand. These developments suggest the company is still executing well and maintaining a durable long-term model even in a more challenging retail environment.

This article explores where Wall Street analysts think ASO could trade by 2028. We pulled together consensus targets and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

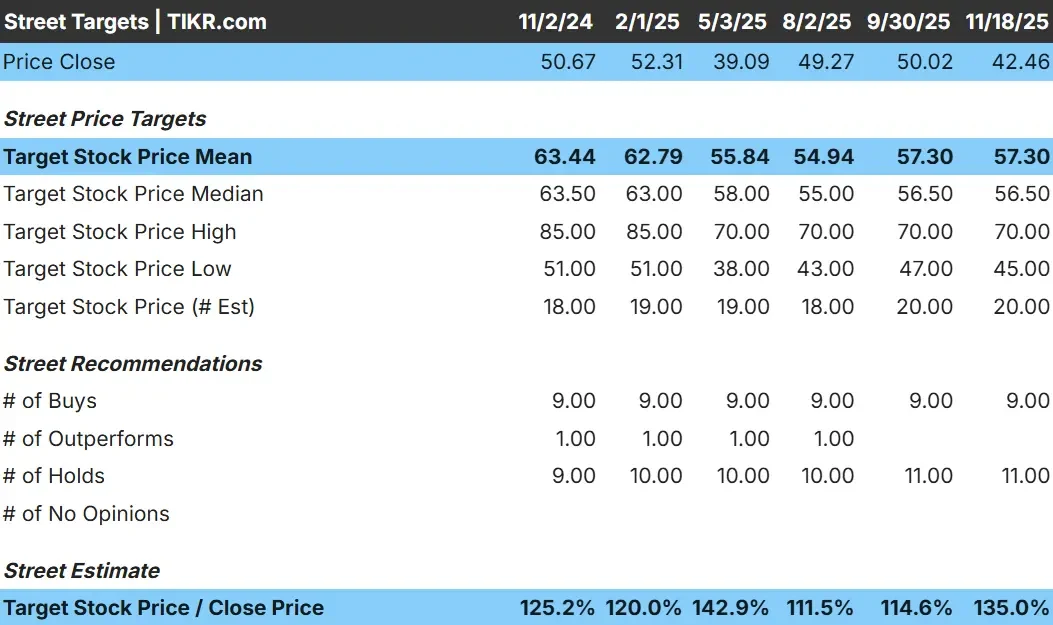

ASO trades near $42/share today. The latest analyst average price target sits at $57/share, which points to about 34% upside. That places ASO in the meaningful upside category.

Key details from the 11/18/25 target grid:

- High estimate: $70/share

- Low estimate: $45/share

- Median estimate: $57/share

- Ratings: 9 Buys, 11 Holds

For investors, this setup suggests analysts expect a solid rebound rather than a small lift. The spread between high and low targets is relatively tight, which shows analysts have a stable view of the company’s performance. ASO’s discounted valuation and consistent profitability are the primary reasons analysts see meaningful room for the stock to move higher.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

ASO: Growth Outlook and Valuation

The company’s outlook appears steady and supported by consistent profitability trends.

- Revenue is projected to grow about 5.9% through early 2028

- Operating margins are expected to move toward about 8.4%

- Shares trade near 6.9x forward earnings, well below most retail peers

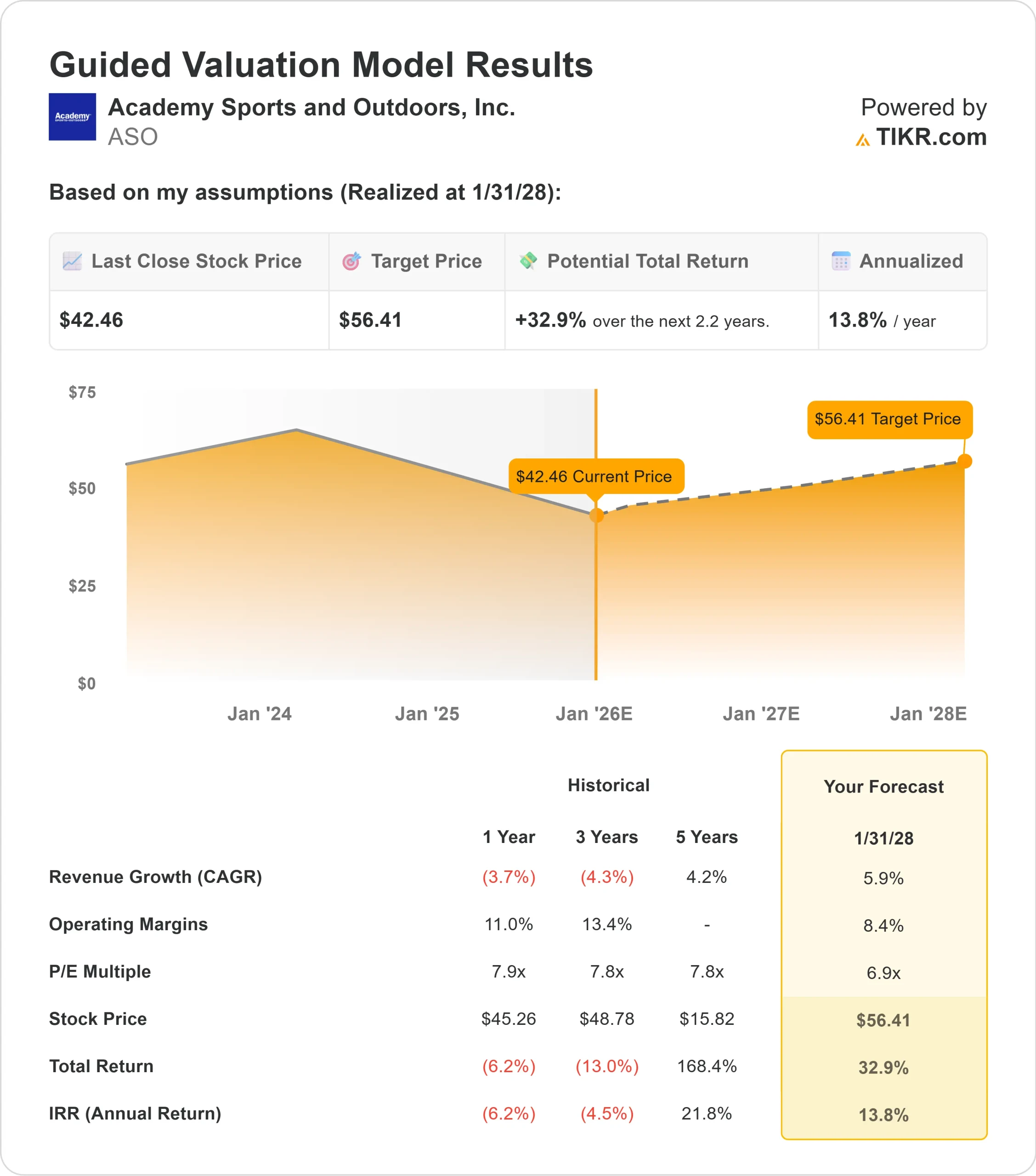

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 6.9x forward P E suggests about $56/share by early 2028

- That implies roughly 33% upside, or about 14% annualized returns

These numbers suggest ASO has enough valuation support to generate attractive returns even without fast revenue growth. The stock looks inexpensive relative to its stability, which means upside depends more on steady execution than a major turnaround.

For investors, ASO screens as a value-driven operator with healthy fundamentals, where modest improvements in performance can still translate into meaningful gains.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Analysts point to several strengths that support ASO’s outlook. The company maintains a resilient operating model focused on value, which resonates with consumers in both strong and weak spending environments. Disciplined inventory management and a balanced merchandising strategy have helped the company protect profitability even as traffic trends soften.

Management’s continued investments in omnichannel capabilities and store efficiency also support long-term stability. These efforts help enhance customer engagement and improve overall productivity. For investors, these factors suggest ASO can maintain steady performance while navigating a more challenging macro backdrop.

Bear Case: Slower Growth and Margin Pressure

The bear case centers on the possibility that ASO’s growth remains muted. The sporting goods category has normalized from its peak surge, and discretionary spending can shift quickly. If demand weakens further or competition intensifies, ASO may find it difficult to accelerate growth at the pace analysts expect.

There is also a risk that profitability could come under pressure if promotions rise or if operating costs grow faster than sales. For investors, the concern is not that ASO collapses, but that it stabilizes rather than grows, which could limit long-term returns even if downside risk appears manageable.

Outlook for 2028: What Could ASO Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests ASO could trade near $56/share by early 2028. That represents about 33% upside from current levels, or roughly 14% annualized returns.

While this forecast points to meaningful upside, it also assumes that margins remain stable and revenue grows at a moderate pace. To outperform these expectations, ASO would likely need stronger sales momentum or improved operating leverage. Without that, investors should expect steady rather than explosive returns.

For investors, ASO stands out as a value-driven retailer with a durable business model and manageable risk profile. The stock does not require aggressive growth to deliver attractive returns, but stronger execution could push performance beyond current estimates.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>