Humana Inc. (NYSE: HUM) has fallen sharply over the past year. The stock trades near $229 per share, down about 22%, as rising medical costs and weaker margins continue to pressure earnings. Sentiment remains soft, and expectations have shifted to some of the lowest levels investors have seen in years.

Recently, Humana announced another round of cost reviews aimed at stabilizing medical expense trends, which have been the main driver of the stock’s decline. The company also issued updated guidance pointing to steadier enrollment growth and better visibility heading into 2026. These developments signal that management is taking more active steps to regain control of the areas that matter most to investors.

This article explores where Wall Street analysts think Humana could trade by 2027. We review consensus forecasts and TIKR’s Guided Valuation Model to outline the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

Humana trades near $229 per share today. The latest analyst average price target sits at $288 per share, which implies about 26% upside. The range of targets is fairly wide, showing mixed conviction across Wall Street.

- High estimate: $353 per share

- Low estimate: $231 per share

- Median target: $285 per share

- Ratings: 6 Buys, 3 Outperforms, 17 Holds, 1 Sell

Humana fits the meaningful upside category because the average target is well above the current price. For investors, this suggests analysts expect a steady recovery once medical cost trends normalize. The setup looks more favorable now, although sentiment still depends heavily on visibility around expenses.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Humana: Growth Outlook and Valuation

Humana’s fundamentals show steady growth but ongoing pressure on profitability:

- Revenue is projected to grow 9% through 2027

- Operating margins are expected to remain near 3%

- Shares trade at roughly 17x forward earnings, below historical averages

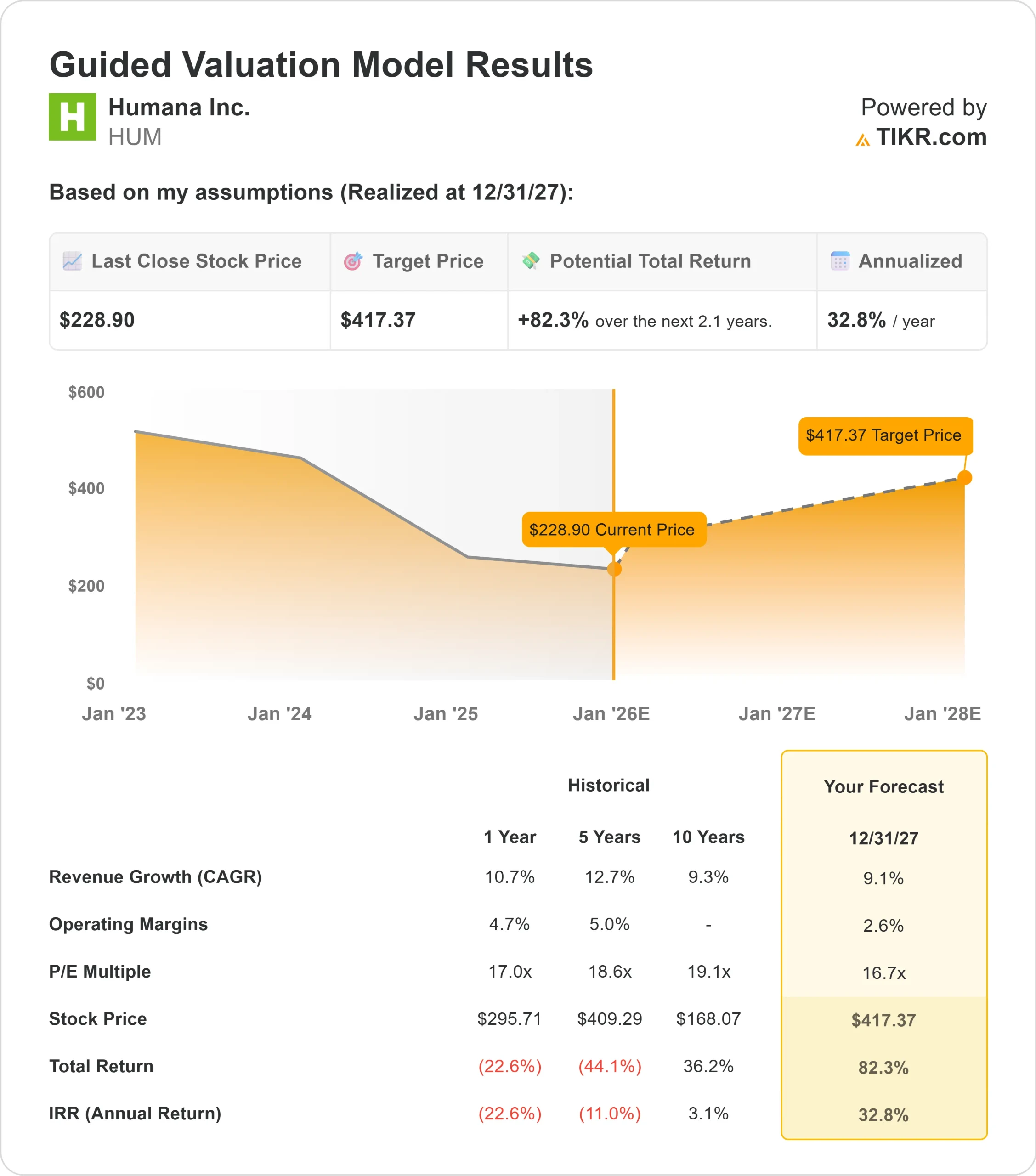

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 17x forward P E suggests about $417 per share by 2027

- That implies roughly 82% upside, or about 33% annualized returns

These numbers highlight how much the stock has reset compared to recent years. The model does not assume aggressive performance. It simply reflects what Humana could be worth if margins stabilize and valuation moves back toward a more typical level.

For investors, Humana looks more like a recovery setup than a high growth story. The stock does not need rapid earnings expansion to deliver gains. It only needs steadier cost trends and consistent execution for shares to re-rate from today’s discounted valuation.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Although Humana has faced a difficult year, several factors support optimism for a recovery. The company continues to see healthy demand across its core healthcare programs, and membership trends remain stable. Revenue growth has held up even as profitability has softened, which indicates that the underlying business remains solid.

Management has begun increasing its focus on cost control. Recent updates suggest a more targeted approach to managing the areas that have caused the most volatility. These signals have helped rebuild some confidence that conditions may become more predictable in the coming year.

For investors, these strengths point to a company that still has the foundation to rebound once cost trends normalize. Humana does not need exceptional performance. It simply needs steady execution and improved visibility around medical expenses.

Bear Case: Margin Pressure and Cost Uncertainty

The biggest risk for Humana is that medical cost trends remain unpredictable. When margins are already thin, even small swings in utilization can significantly impact earnings. This makes the stock more sensitive to quarterly results.

Competition in Medicare Advantage also remains intense. It can be difficult for Humana to raise premiums without risking enrollment softness, especially in an environment where consumers and insurers are both facing cost pressures. Regulatory changes also introduce uncertainty around reimbursement in future periods.

For investors, the bear case is that margins fail to recover meaningfully. If cost volatility persists, the stock may struggle to break out even though valuation appears attractive.

Outlook for 2027: What Could Humana Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 17x forward P E suggests Humana could trade near $417 per share by 2027. This represents about 82% upside, or roughly 33% annualized returns.

This would be a strong rebound from current levels, but it depends on progress toward stabilizing margins. The model does not assume aggressive growth. It reflects a scenario where cost trends improve and valuation returns to a more typical level.

For investors, the key question is whether Humana can deliver steadier cost trends over the next two years. If management provides consistent execution and maintains solid enrollment, the stock could re-rate much faster than expected. If not, returns may align more closely with the midrange analyst targets that imply about 26% upside.

Humana stands as a credible recovery story, but long term performance depends on the company proving that the most volatile period for medical expenses is finally behind it.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>