Elevance Health (NYSE: ELV) has had a challenging year. The stock trades near $319/share, down about 19% as rising medical cost trends and soft profitability pressured investor sentiment. Even with these challenges, analysts still view Elevance as a stable operator with dependable premium revenue and a strong long term track record.

Recently, Elevance highlighted progress in cost management and continued momentum in Carelon, its growing health services platform. Carelon has become a key driver of Elevance’s strategy, offering higher margin opportunities and helping reduce earnings volatility tied to insurance cycles. These updates show that Elevance is actively positioning itself for steadier performance even as cost pressures remain elevated across the healthcare system.

This article reviews where analysts expect ELV to trade by 2027 based on TIKR’s valuation model and the latest Street targets. These figures reflect analyst expectations and are not TIKR’s predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

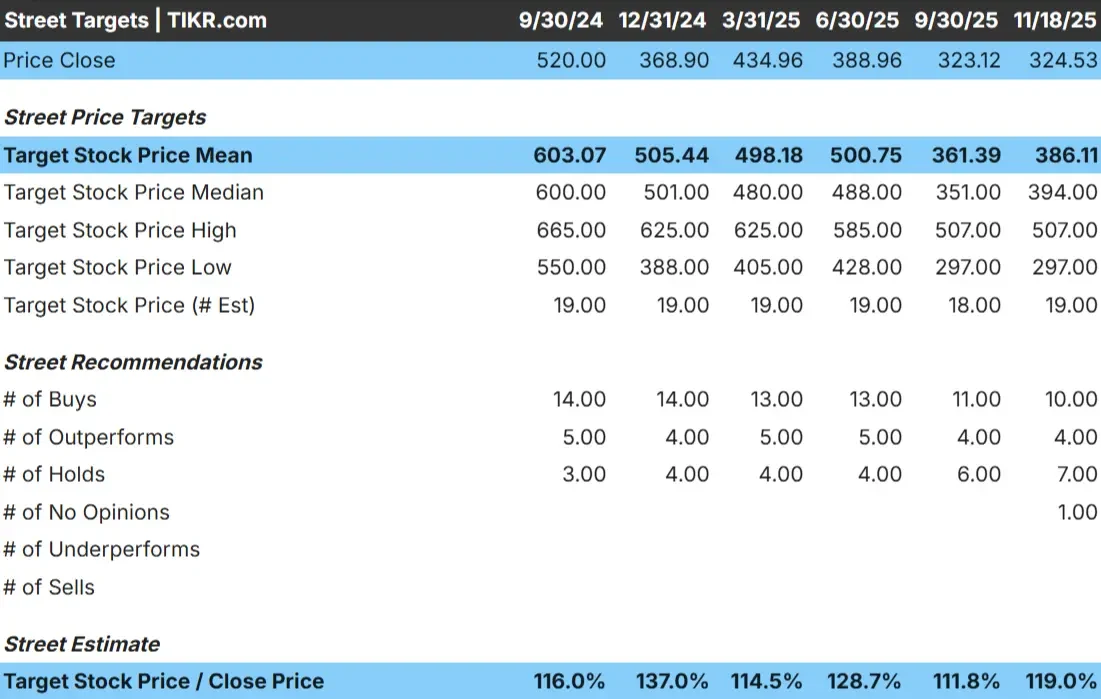

Elevance trades near $319/share today. The latest analyst average price target is $386/share, which implies about 21% upside. This places Elevance in the modest upside category, since expectations do not call for a major rerating.

Key numbers from the latest analyst grid:

- High estimate: $507/share

- Low estimate: $297/share

- Median target: $394/share

- Ratings: 10 Buys, 4 Outperforms, 7 Holds

Analysts see some room for a rebound, but the wide spread between the high and low estimates shows conviction is mixed. For investors, Elevance could still outperform if medical cost trends normalize, yet the path upward depends on steadier margins and better visibility into future profitability.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Elevance Health: Growth Outlook and Valuation

The company’s long term outlook appears steady and is supported by conservative assumptions across revenue growth and profitability:

- Revenue is projected to grow about 7%

- Operating margins are expected to hold near 5%

- Shares trade at an implied 11x forward earnings in the valuation model

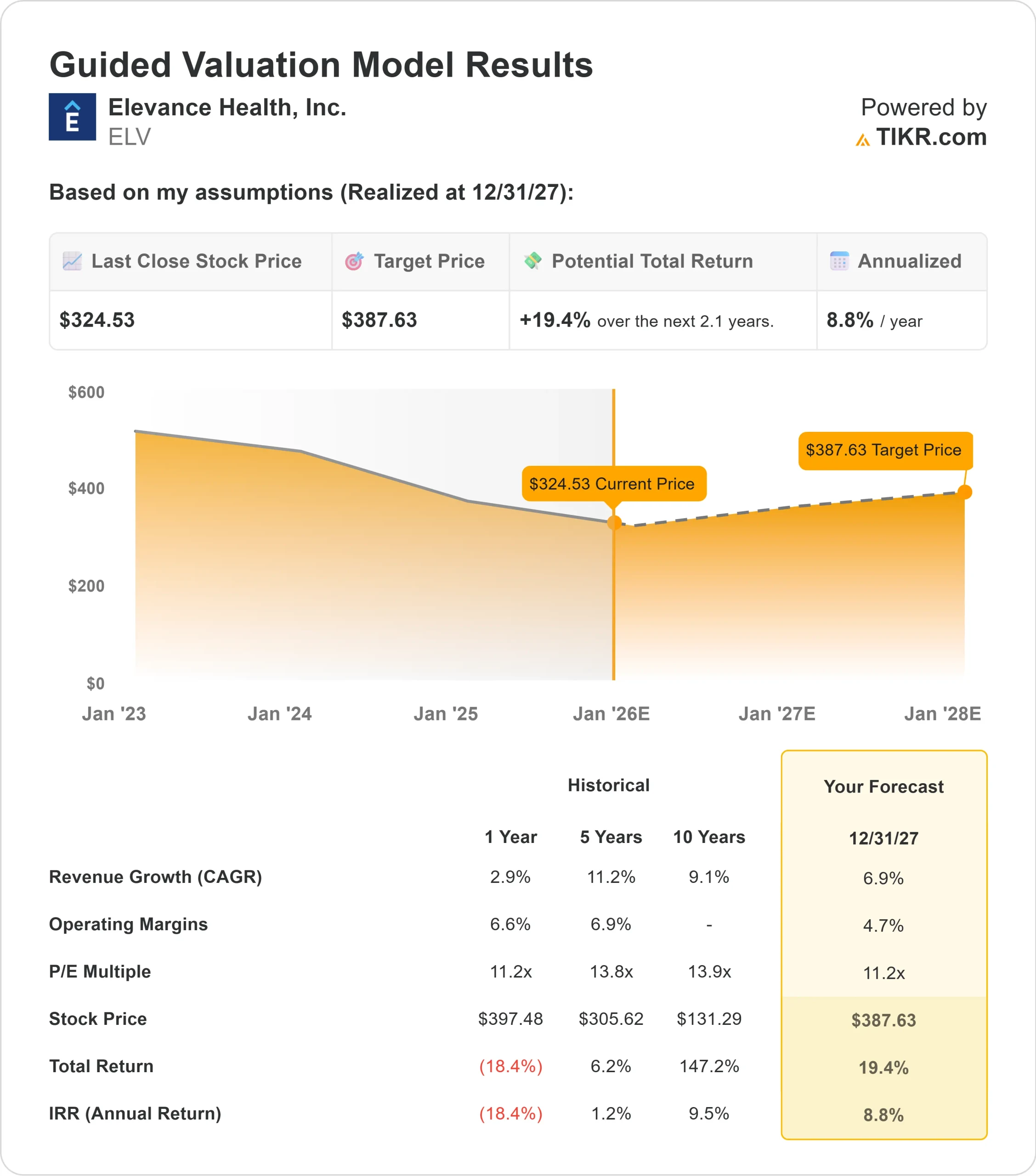

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests about $388/share by 2027

- That implies roughly 19% upside, or about 9% annualized returns

These inputs point to a stable growth profile rather than an aggressive rebound. For investors, Elevance looks more like a steady compounder supported by consistent premium revenue and disciplined cost control. The upside case depends less on rapid expansion and more on maintaining solid execution across its core insurance and services business.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Elevance benefits from a large membership base that produces reliable premium revenue and helps smooth performance even during volatile periods. Carelon, the company’s health services arm, is gaining traction and provides diversification that reduces Elevance’s dependence on traditional insurance-driven profit cycles.

Management has been investing in technology and care management programs aimed at improving efficiency across the business. For investors, these initiatives show that Elevance is working deliberately to strengthen its operational foundation and support more predictable earnings over time.

Bear Case: Margins and Medical Costs

The biggest risks for Elevance come from unpredictable medical cost trends and rising competitive pressure. Elevated utilization in certain categories can quickly weigh on profitability, and periods of higher costs often lead to weaker sentiment around the stock.

Competitive dynamics in the healthcare sector are also intensifying as regional plans and vertically integrated peers expand their offerings. For investors, the main concern is that Elevance may struggle to lift margins if cost dynamics do not stabilize.

Outlook for 2027: What Could Elevance Health Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using an 11x forward P E suggests Elevance could trade near $388/share by 2027. This represents about 19% upside, or roughly 9% annualized returns.

This outlook reflects a steady recovery rather than a major valuation shift. Elevance does not need a dramatic improvement in margins to reach the high $380s, but it does require consistent cost control and ongoing momentum within Carelon. For investors, Elevance offers a path to moderate and dependable returns, with the possibility of stronger upside if medical cost trends improve faster than expected.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>