Stryker Corporation (NYSE: SYK) continues to navigate a steady but slower growth environment. The stock trades near $369/share, holding up better than many medical device peers, although still below its recent high of $406/share. Revenue trends remain healthy, margins are stable, and Stryker’s diversified mix across MedSurg, orthopedics, and surgical technologies supports confidence in long term consistency.

Recently, Stryker reported stronger than expected procedure volumes and highlighted accelerating adoption of its Mako robotics platform as hospitals continue to expand joint replacement capacity. The company also noted improving demand across MedSurg equipment, suggesting that hospital capital spending may be stabilizing. These developments show that Stryker can continue driving steady performance even in a mixed healthcare environment.

This article outlines where Wall Street analysts expect the stock to trade by 2028. We combined the latest price targets with TIKR’s Guided Valuation Model to map out Stryker’s potential path. These figures reflect current analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Modest Upside

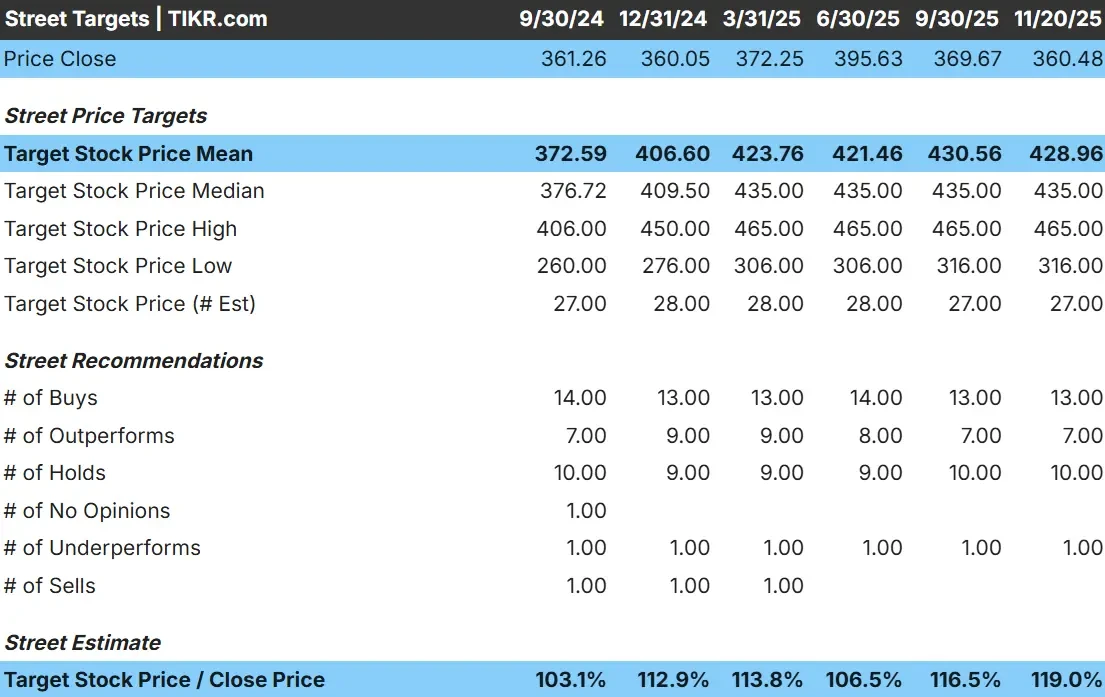

Stryker trades around $369/share today, and analysts see a steady path higher. The latest average analyst price target is $429/share, which implies about 16% upside, placing the stock in the modest upside category. Forecasts across the analyst group remain fairly consistent:

- High estimate: $465/share

- Low estimate: $316/share

- Median target: $435/share

- Ratings: 13 Buys, 7 Outperforms, 10 Holds, 1 Underperform

The forecast range is reasonably tight, which shows stable conviction among analysts. For investors, this suggests Stryker can continue compounding through dependable procedure trends, steady MedSurg demand, and expanding robotics adoption. The stock is positioned more as a reliable long term operator than a high volatility name.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

Stryker: Growth Outlook and Valuation

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 25x forward P E suggests Stryker could reach about $453/share by 2027. The company’s fundamentals point to steady performance supported by consistent revenue and margin trends:

- Revenue is projected to grow about 9.3%

- Operating margins are expected to hold near 27.0%

- Shares trade near 25x forward earnings, in line with Stryker’s long term premium

- Based on analysts’ average estimates, the valuation model points to about $453/share

- That implies roughly 26% upside, or about 11% annualized returns

These figures show that Stryker can compound steadily without relying on dramatic growth acceleration. The outlook is shaped by high single digit revenue gains, firm margins, and continued leadership across MedSurg and orthopedics.

For investors, Stryker is positioned as a consistent long term compounder. Stable execution, predictable demand from hospitals, and a durable product ecosystem create a foundation that can support reliable returns over time.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Stryker benefits from steady procedure growth and consistent demand across its orthopedic and surgical categories. Hospitals continue to rely on Stryker equipment in operating rooms, and the company remains a core partner for systems modernizing their surgical workflows. The Mako robotics platform is gaining traction, which strengthens Stryker’s position in joint replacement.

Management’s continued focus on innovation, improved manufacturing, and stronger supply chain execution adds further support. For investors, these strengths provide confidence that Stryker can maintain stable earnings and reduce volatility across economic cycles.

Bear Case: Valuation and Competition

The primary risk for Stryker is valuation. The stock trades at a premium earnings multiple, and the market expects steady growth to continue. If hospital spending slows or procedure volumes weaken, the stock could face pressure.

Competition also remains active in key categories like orthopedics, robotics, and digital surgery. Several players are investing heavily to capture share. For investors, the main concern is not operational deterioration but the possibility of the market reducing Stryker’s premium valuation if industry conditions soften.

Outlook for 2028: What Could Stryker Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model suggests Stryker could trade near $453/share by 2027. That represents roughly 26% upside, or about 11% annualized returns over the next few years.

This outcome would mark a strong period of compounding, but it already assumes stable margins and consistent growth. For Stryker to deliver more meaningful upside, the company would likely need faster robotics adoption or a stronger rebound in hospital capital spending.

For investors, Stryker looks like a high quality long term compounder. The outlook depends on steady execution and maintaining its leadership across orthopedics and surgical technologies.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>