Boston Scientific Corporation (NYSE: BSX) has continued to outperform many large med tech peers. Shares trade near $97/share today, supported by strong procedure volumes, healthy demand across cardiovascular devices, and consistent execution across its major business lines. The stock has remained resilient in a mixed med tech environment, reflecting the strength of its product mix and long-term growth profile.

Recently, Boston Scientific posted results that showed double-digit revenue momentum across several key categories and improving profitability. The company also advanced two major growth drivers. Its Farapulse pulsed-field ablation system continues to gain traction in electrophysiology, and adoption of the WATCHMAN FLX Pro device remains strong in structural heart. These developments signal that BSX is expanding leadership in some of the fastest-growing areas of medical technology.

This article outlines where Wall Street analysts believe BSX could trade by 2027. The forecast combines analyst price targets with TIKR’s Guided Valuation Model to estimate the stock’s potential path. These figures reflect analyst expectations and are not TIKR’s own predictions.

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free) >>>

Analyst Price Targets Suggest Meaningful Upside

BSX trades near $97/share today. The latest analyst average price target is $126/share, which implies about 31% upside. Since upside exceeds 30%, BSX falls into the meaningful upside category.

Key data from the Street target grid:

- High estimate: $140/share

- Low estimate: $99/share

- Median target: $130/share

- Ratings: 25 Buys, 7 Outperforms, 2 Holds

For investors, analysts see BSX as one of the more durable growth stories in med tech. The wide range in targets reflects different assumptions regarding margin expansion and adoption timelines, but the strong leaning toward Buy ratings shows confidence in Boston Scientific’s long-term outlook. Most analysts believe the company can continue delivering steady gains without requiring a significant shift in demand trends.

Discover how much upside your favorite stocks could have using TIKR’s new Valuation Model (It’s free) >>>

BSX: Growth Outlook and Valuation

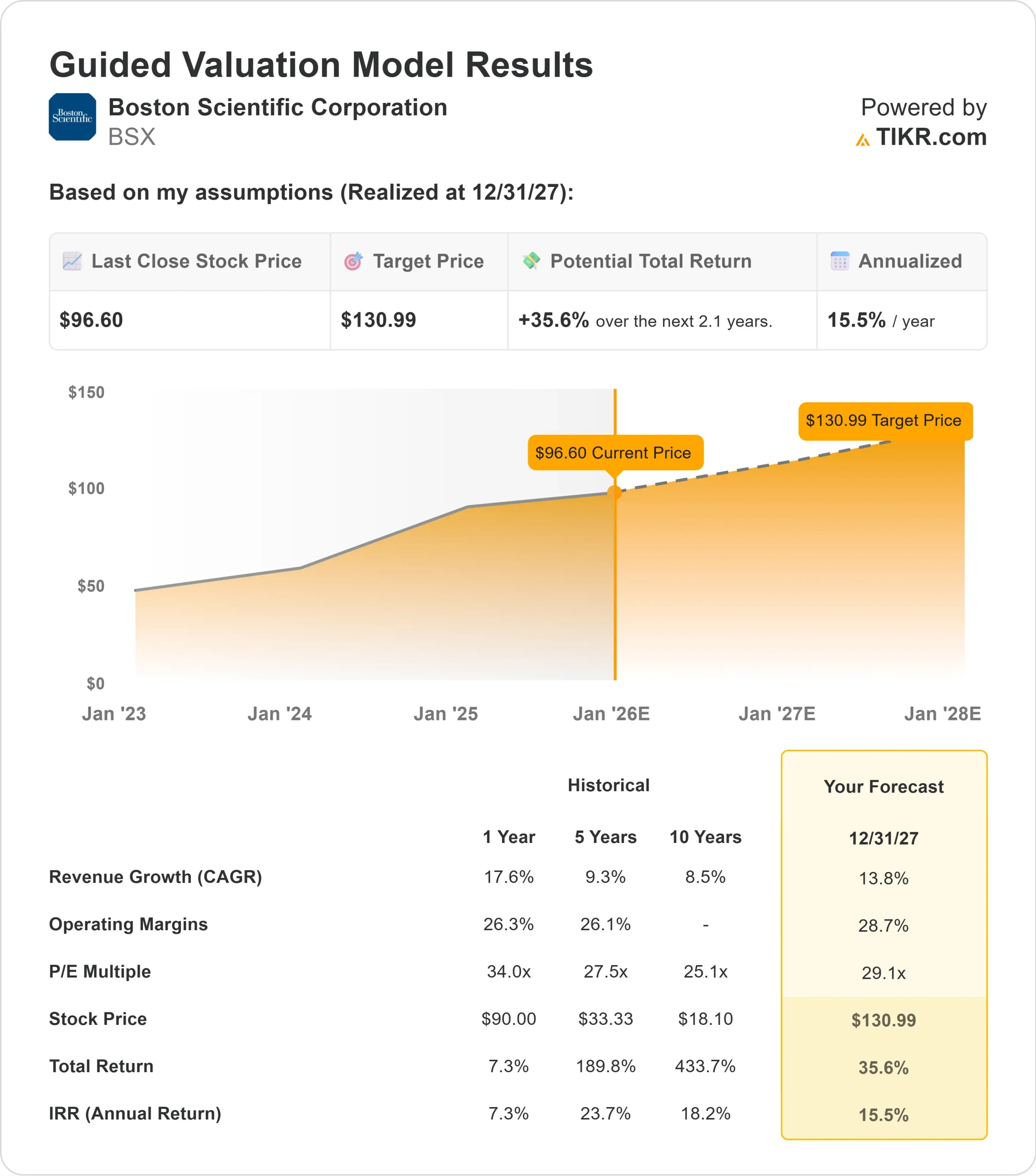

The company’s fundamentals appear strong heading into 2027, supported by healthy revenue momentum and improving profitability across key categories.

- Revenue growth forecast: 13.8%

- Operating margins expected to reach 28.7%

- Shares trade at about 29.1x forward earnings

- Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 29.1x forward P E suggests $131/share by 2027

- That implies roughly 36% upside, or about 16% annualized returns

These numbers point toward steady compounding rather than aggressive acceleration. BSX benefits from reliable demand trends and a portfolio of higher-value devices that support margin expansion. For investors, the company looks positioned to deliver solid long-term returns as long as it maintains its current level of execution.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

What’s Driving the Optimism?

Boston Scientific benefits from a wide range of growth drivers across electrophysiology, structural heart, and interventional cardiology. Products like Farapulse and WATCHMAN FLX Pro continue to gain adoption across global markets, and demand in these categories tends to hold up well even in softer healthcare environments. This gives BSX a strong foundation for sustained long-term growth.

Management has also delivered consistently strong execution. Revenue momentum continues to outpace many large device peers, and margin improvement is becoming more visible as newer product lines scale. For investors, these factors help explain the persistent bullish sentiment. The combination of innovation, reliable demand, and improving profitability supports a long runway for earnings growth.

Bear Case: Valuation and Competitive Pressures

Despite its strengths, BSX trades at a premium valuation. At roughly 29x forward earnings, the company needs to maintain its growth trajectory to justify the multiple. If revenue growth slows or margin expansion underperforms, the valuation could compress and limit returns.

Competition also remains a key consideration. Abbott, Medtronic, and Edwards compete aggressively in overlapping categories, and the pace of innovation across med tech can shift market share quickly. Hospitals remain cost-sensitive, and reimbursement changes can affect profitability across certain device lines. For investors, the risk is that even strong execution may not always be enough to support a premium valuation if broader conditions weaken.

Outlook for 2027: What Could BSX Be Worth?

Based on analysts’ average estimates, TIKR’s Guided Valuation Model using a 29.1x forward P E suggests BSX could trade near $131/share by 2027. This implies about 36% upside, or roughly 16% annualized returns from today’s price.

This outlook reflects a steady and achievable pace of growth. To generate meaningfully stronger upside, BSX would need faster margin expansion, broader international adoption of its key devices, or continued outperformance relative to peers. Without that, returns are likely to follow a stable and predictable path.

For investors, Boston Scientific remains a high-quality long-term compounder. The stock has a clear path to attractive multi-year gains, supported by reliable demand and an expanding portfolio of high-value medical technologies.

AI Compounders With Massive Upside That Wall Street Is Overlooking

Everyone wants to cash in on AI. But while the crowd chases the obvious names benefiting from AI like NVIDIA, AMD, or Taiwan Semiconductor, the real opportunity may lie on the AI application layer where a handful of compounders are quietly embedding AI into products people already use every day.

TIKR just released a new free report on 5 undervalued compounders that analysts believe could deliver years of outperformance as AI adoption accelerates.

Inside the report, you’ll find:

- Businesses already turning AI into revenue and earnings growth

- Stocks trading below fair value despite strong analyst forecasts

- Unique picks most investors haven’t even considered

If you want to catch the next wave of AI winners, this report is a must-read.

Find out what your favorite stocks are really worth (Free with TIKR) >>>