The Bank of Nova Scotia (BNS) is one of Canada’s largest financial institutions and a key player across retail banking, commercial lending, wealth management, and international banking, particularly in Latin America. The stock has rebounded sharply this year, supported by easing credit concerns, stronger capital levels, and improving sentiment toward Canadian banks.

The bank continues to adjust its portfolio mix, working to build more stable earnings through cost control and targeted growth in wealth and commercial lending. At the same time, management is reshaping risk exposure in its international segment to reduce volatility. The combination of stronger capital, solid deposits, and clearer strategic priorities has helped the stock regain momentum.

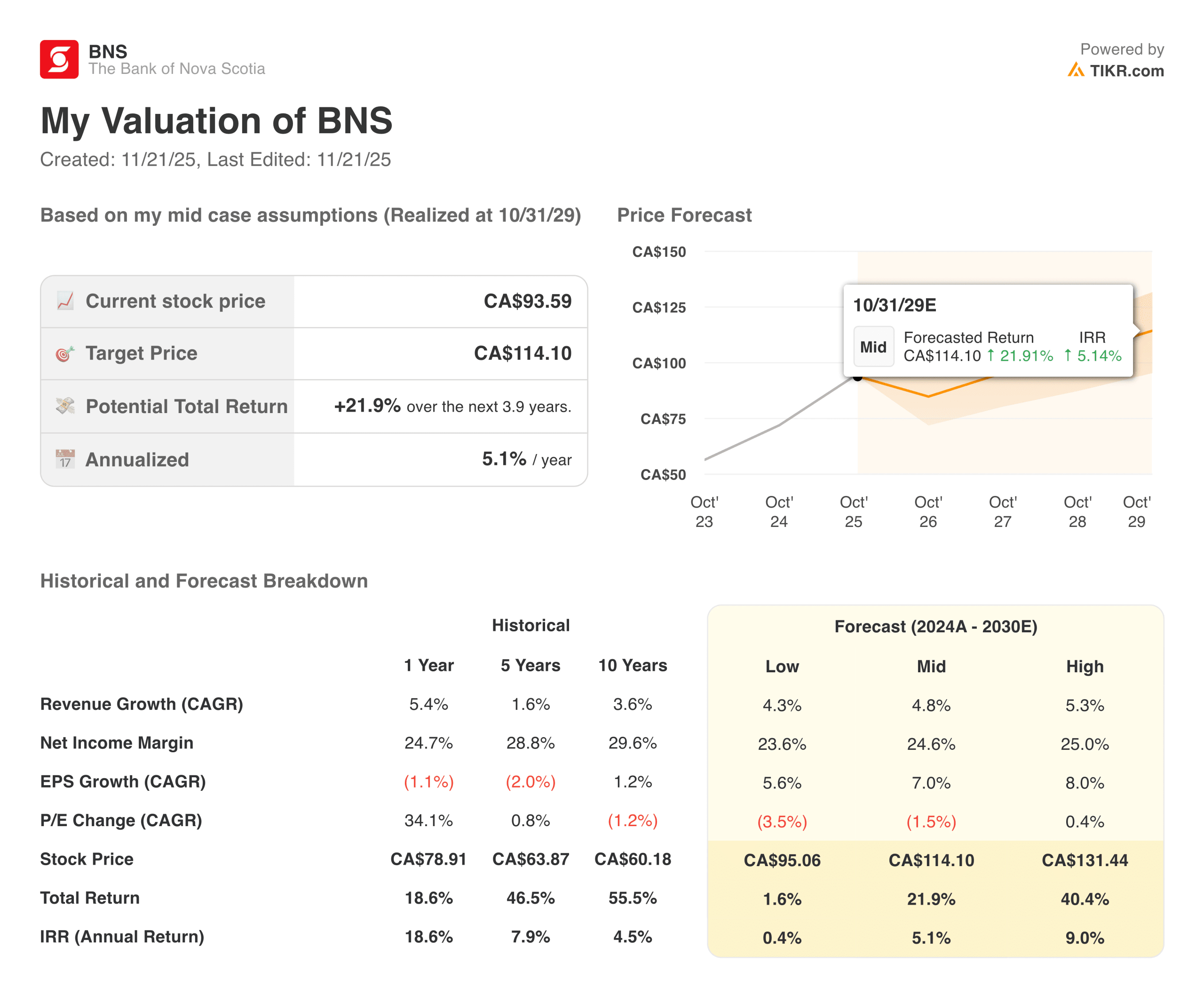

Find out what a stock’s really worth in under 60 seconds with TIKR’s new Valuation Model (It’s free)>>>

BNS remains focused on tightening expenses and improving profitability after several uneven quarters. Credit provisions have been elevated, but trends have begun to move in a more stable direction as consumer and commercial credit conditions normalize.

The bank’s CET1 capital ratio is now comfortably above regulatory levels, providing flexibility for dividends and long-term investment. While revenue growth remains modest, loan growth has picked up in select areas, with international and wealth units showing the most traction. Overall performance reflects a bank in transition, moving toward a more balanced earnings profile.

Quickly value any stock with TIKR’s powerful new Valuation Model (It’s free!) >>>

Financial Story

Bank of Nova Scotia delivered steadier results this past quarter as net interest income held firm and non-interest revenue improved. Expenses remain a key focus, with management continuing to target efficiency improvements after several years of cost pressure.

Provisions for credit losses remained elevated but have started to moderate, helping overall earnings show greater consistency. The capital position remains strong, and the bank maintained its dividend, which continues to be a central part of its investment appeal. Loan growth was supported by stable Canadian retail volumes and recovering international demand.

| Metric | Current Quarter | Sequential Change | Year-over-Year Change |

|---|---|---|---|

| Net Income | $2.2B | +7% | +4% |

| Revenue | $8.4B | +3% | +5% |

| Net Interest Margin | 2.30% | Flat | -5 bps |

| Provisions for Credit Losses | $962M | -4% | +9% |

| CET1 Capital Ratio | 13.5% | +20 bps | +60 bps |

| Expenses | $4.1B | -1% | +2% |

The bank’s balance sheet strength has helped rebuild investor confidence. Deposits grew at a healthy pace, liquidity coverage remained robust, and loan-loss reserves remain well-positioned for a more moderate credit environment. International banking saw sequential improvement, supported by more substantial margins and better cost control. Wealth and capital markets also contributed to quarter-over-quarter gains, improving the earnings mix. The overall picture shows a bank gradually stabilizing after a period of elevated volatility.

Look up Bank of Nova Scotia’s full financial results & estimates (It’s free) >>>

Broader Market Context

Canadian banks have faced several years of margin pressure and slow loan growth due to rate hikes, consumer weakness, and soft housing activity. As conditions normalize, the sector is showing early signs of stabilization, particularly in retail lending and credit performance. Investors are watching closely to see how quickly banks can grow earnings again after years of muted profitability. Cost control and capital strength have become central themes across the sector as management teams work to boost returns. In this environment, a bank with a strong deposit base and diversified revenue streams stands out.

International exposure remains a differentiator for BNS compared to other Canadian banks. South American markets have shown uneven economic conditions, but improving currency stability and recovering demand have supported better results. The bank has worked to reposition its international footprint toward higher-return segments and reduce higher-risk categories. That shift has helped moderate earnings volatility, though the segment remains closely watched by investors. If global credit conditions continue to stabilize, the international business could become a growing contributor again.

1. Retail and Commercial Banking Performance

Retail banking delivered more consistent results, with margins holding steady and deposit volumes improving. Mortgage growth remained subdued, but consumer lending showed modest sequential gains, particularly in credit cards and personal loans. Expense control played a meaningful role in supporting profitability after several quarters of pressure. Customer deposits increased, helping to offset a more competitive rate environment that has weighed on net interest margins. These trends give the retail unit a firmer base heading into the next fiscal year.

Commercial banking saw stable loan demand across most sectors, supported by improved credit performance among business clients. Margins remained resilient despite a competitive lending landscape, and fee income rose due to higher transaction activity. Management continues to focus on risk-adjusted growth rather than broad expansion, emphasizing capital efficiency. As business confidence continues to improve, commercial lending may become a more meaningful tailwind. The division remains a core contributor to earnings stability.

2. International Banking Momentum

International banking delivered better sequential results, with margin expansion and lower expenses helping profitability recover. The bank saw stronger loan growth in key regions, supported by healthier demand trends and early signs of macro stabilization. Management has emphasized improving risk management and operational discipline in international markets, which has helped show better consistency in results. Currency movements remain a swing factor, but revenue and earnings trends point toward improving underlying momentum. This segment remains a long-term growth opportunity for the bank.

At the same time, provisions for credit losses remain higher in international markets compared to Canada, reflecting a more volatile environment. However, the trend has been improving as economic conditions stabilize across several Latin American economies. BNS has also been shifting its international portfolio toward higher-return products and markets, reducing exposure to categories that historically contributed to earnings volatility. If these adjustments continue to take hold, the global business may regain its role as a more dependable earnings driver. The segment remains one of the most important to watch.

Value stocks like Bank of Nova Scotia in less than 60 seconds with TIKR (It’s free) >>>

3. Wealth and Capital Markets

Wealth management delivered solid growth supported by higher client activity and stronger market performance. Fee-based revenue increased, and net sales trends improved in both advisory and asset management. The segment also benefited from operational efficiencies, which helped margins trend higher. With household wealth rising, the platform is positioned to contribute more meaningfully to long-term earnings. This area remains a strategic focus for diversification.

Capital markets turned in a more stable performance this quarter as underwriting and advisory activity improved. Trading revenue was steady, supported by stronger market conditions and healthy client demand. Cost management efforts in the division have helped offset pockets of revenue softness across certain desks. The bank continues to invest in technology and risk systems to support more resilient performance. While results can fluctuate, the division has shown greater consistency in recent quarters.

The TIKR Takeaway

Bank of Nova Scotia looks steadier than it did a year ago, supported by stronger capital, improving credit trends, and more balanced earnings across segments. Retail and commercial banking are stabilizing, the international business is showing better traction, and wealth and capital markets are contributing more consistently.

The bank remains in transition, but the direction is improving. Investors will watch whether management can continue to reduce volatility and strengthen long-term profitability.

Should You Buy, Sell, or Hold Bank of Nova Scotia’s Stock in 2025?

Bank of Nova Scotia remains in a rebuilding phase, but the recent results show a clearer path forward. A stronger capital base, improving credit conditions, and better expense control support a more stable earnings profile. The international business is also moving toward healthier growth, and wealth management continues to gain momentum. At the same time, the bank is still working through uneven revenue growth and elevated provisions. The next few quarters will determine whether the improvements evolve into a sustainable trend.

How Much Upside Does Bank of Nova Scotia Stock Have From Here?

With TIKR’s new Valuation Model tool, you can estimate a stock’s potential share price in under a minute.

All it takes is three simple inputs:

- Revenue Growth

- Operating Margins

- Exit P/E Multiple

If you’re not sure what to enter, TIKR automatically fills in each input using analysts’ consensus estimates, giving you a quick, reliable starting point.

From there, TIKR calculates the potential share price and total returns under Bull, Base, and Bear scenarios so you can quickly see whether a stock looks undervalued or overvalued.

See a stock’s true value in under 60 seconds (Free with TIKR) >>>

Looking for New Opportunities?

- See what stocks billionaire investors are buying so you can follow the smart money.

- Analyze stocks in as little as 5 minutes with TIKR’s all-in-one, easy-to-use platform.

- The more rocks you overturn… the more opportunities you’ll uncover. Search 100K+ global stocks, global top investor holdings, and more with TIKR.

Disclaimer:

Please note that the articles on TIKR are not intended to serve as investment or financial advice from TIKR or our content team, nor are they recommendations to buy or sell any stocks. We create our content based on TIKR Terminal’s investment data and analysts’ estimates. Our analysis might not include recent company news or important updates. TIKR has no position in any stocks mentioned. Thank you for reading, and happy investing!